Western Digital (WDC) has quietly staged a strong comeback over the past few months as investor enthusiasm around AI infrastructure and cloud storage continues to build. The data-storage specialist has benefited from rising demand for high-capacity drives, with Wall Street warming up to the idea that AI-driven data growth could fuel a multi-year upgrade cycle for hard disk technology.

Now the stock has another catalyst. On the heels of these announcements, Morgan Stanley lifted its price target to a Street-high $369, reaffirming WDC as a Top Pick, citing AI as a “sustainable tailwind” for data storage. The firm pointed to a robust technology roadmap, expanding margins, and long-term financial targets that suggest meaningful earnings power ahead.

So does this bullish reset change the outlook for WDC stock, and is WDC worth buying right now?

Western Digital Doubles Down on AI and Cloud Storage

Based in California, Western Digital is a prominent provider of data storage devices and solutions. The company's core business is designing hard disk and flash storage for everything from personal computers to massive cloud data centers. What makes WD unique is its AI focus: it recently rebranded as simply “WD” and says roughly 90% of revenue is driven by AI/cloud customers.

WD has also been busy expanding its AI focus lately. The company reported record shipments of 215 exabytes of storage in Q2, a 22% rise year-over-year (YoY), including millions of its newest 32TB UltraSMR HDDs. These high-density drives have found eager buyers at hyperscale data centers, helping push WD’s “Nearline” cloud revenue up 28%.

Additionally, at Innovation Day, WD introduced a new “intelligent” storage platform, a set of open-API software tools designed to speed deployment of its HDDs in large AI clusters. The goal is to let cloud providers plug WD storage directly into their AI infrastructure more easily.

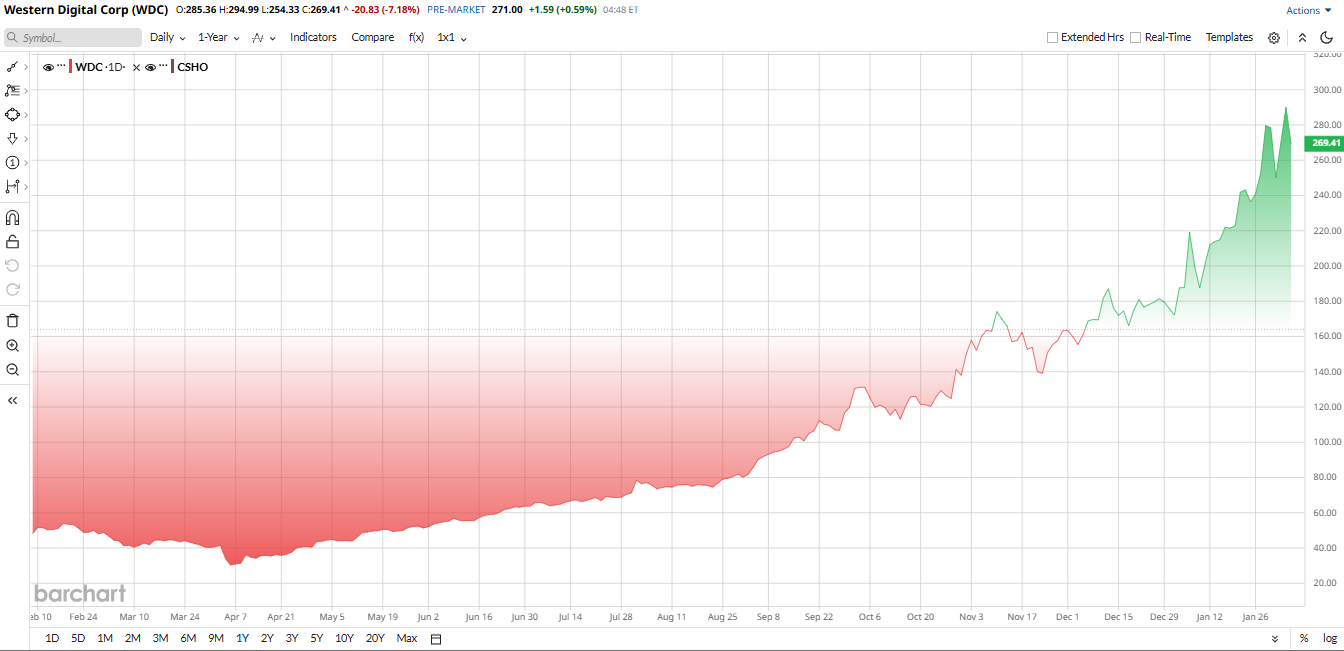

That positioning has translated directly into stock performance. WDC stock has been on a tear lately. It roughly quadrupled in 2025, soaring from the low $40s to around $172 by year-end. That gain of roughly 433% in the past 12 months came as WD repeatedly beat forecasts and hiked guidance. Investors fueled the rally on optimism that exploding AI datasets will drive HDD demand. In fact, management says hyperscale customers are already “pretty much sold out” of capacity into 2026.

Following the bull run, WDC is now trading at elevated levels. For example, the price-to-sales ratio is 8.07, compared to the sector median of 3.41, and the price-to-book ratio is 11.99, well above the sector median of 3.74. These metrics suggest WDC is significantly overpriced relative to its peers.

Morgan Stanley’s Bullish Case

The Innovation Day news has analysts gushing. Morgan Stanley specifically cited the event in raising its WDC target to $369. The firm noted that WD’s new long-term model—20% annual revenue growth, 50% gross margins, and a target of $20 in EPS—looks achievable if AI data keeps expanding. Morgan sees AI as a “sustainable tailwind” that will support HDD pricing, margins, and profits.

In effect, MS is betting that WD’s high-capacity drives and new performance technologies will let it capture a big slice of the booming AI/data economy.

WD Q2 Earnings Show Strong Growth

WDC reported its second-quarter earnings on Jan. 29, which blew past expectations. Revenue was $3.017 billion, up 25% YoY, driven by cloud and AI-heavy data center orders. EPS came in at $2.13, a 78% jump from a year ago. Gross profit margins expanded into the mid-40% range thanks to a richer mix of high-capacity drives like the new UltraSMR tech. In short, sales and profits both surged on strong demand.

The quarter also delivered robust cash flow. WD generated $745 million of operating cash and $653 million of free cash flow. Management immediately returned cash to shareholders: $615 million was spent on buybacks, 3.8 million shares, and full dividends. In fact, the company said it returned 100% of FCF in Q2 to shareholders. Moreover, WD ended Q2 with $1.975 billion in cash and a total liquidity cushion of $3.2 billion.

CEO Tan touted multi-year purchase commitments from all major cloud customers, with orders booked through 2026-28. WD also announced an additional $4 billion share repurchase authorization on top of $484 million left in the prior plan, underscoring management confidence.

Looking ahead, the company guided Q3 revenue at $3.2 billion, which would be a 40% increase YoY, and gross margins at 47.5%, again reflecting sustained big-data demand. Management also reiterated that hyperscaler clients are accelerating adoption of WD’s latest drives, e.g., UltraSMR JBOD platforms, to pack more AI data on disk.

What Do Analysts Say About WD Stock?

Wall Street analysts have generally rallied behind WD’s momentum. Morgan Stanley stands with an “Overweight” rating and now leads the Street at a $369 target, citing the AI “tailwinds” and new long-term guidance as validation.

Similarly, Citigroup also just raised its target to $335 from $325 after the event, noting WD’s new $20 EPS guide.

Even cautious shops have bumped their numbers, like Goldman Sachs, which, with a "Hold" rating, lifted its target to $250 post-Innovation Day, pointing out new product roadmaps and the on-track HAMR ramp.

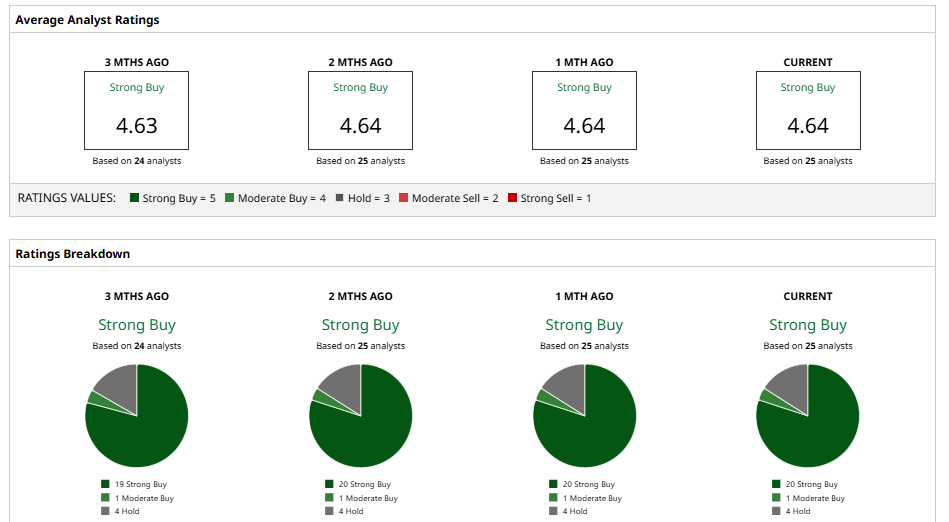

The consensus now stands at a “Strong Buy” rating, with an average price target of $288, which implies a decent 11% upside potential over current levels. In short, analysts agree that Western Digital’s fundamental reset and AI-tailored roadmaps justify the higher targets, as long as execution lives up to the hype.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart