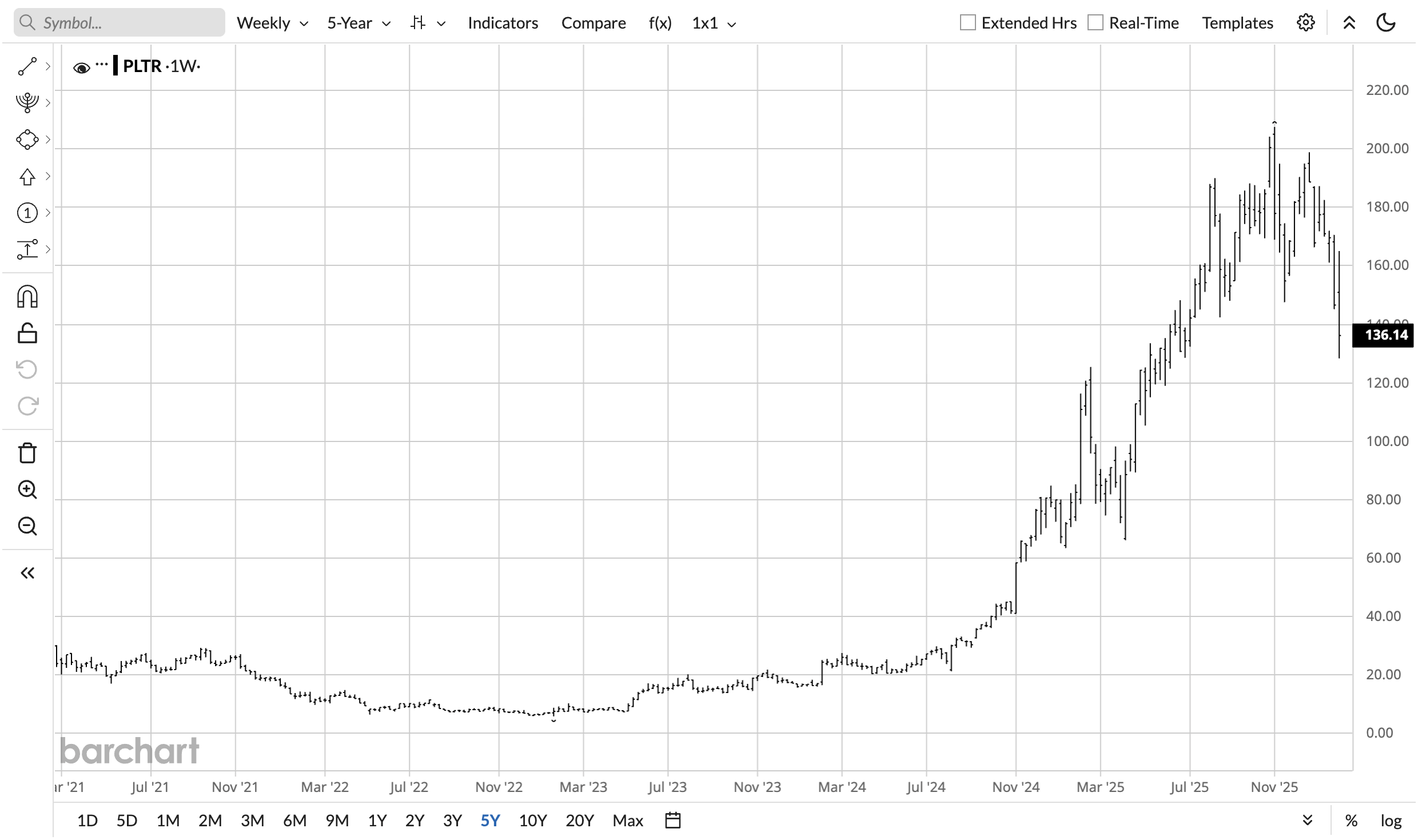

Palantir (PLTR) recently posted fourth-quarter 2025 results that trounced analyst estimates. Revenue grew 70% to $1.41 billion, while adjusted EPS came in at $0.25 against expectations of $0.23. Full-year revenue came in at $4.48 billion, with management expecting 2026 revenue at $7.19 billion, up 61% year-over-year (YOY). That's almost $1 billion more than what the consensus penciled in earlier.

As one would expect, PLTR stock surged on the report, but this didn't last for long. Shares are down 3% over the past five days and the reaction tells you everything about where Palantir sits in the market's imagination. The stock is loved for its fundamentals and feared for its valuation.

Should you chase the execution and buy the stock at a discount, or is PLTR going even lower? Let's take a look at what has been happening.

Palantir Shatters Analyst Expectations

U.S. commercial revenue exploded 137% YOY in Q4, reaching $507 million, while total U.S. revenue grew 93% YOY to $1.08 billion. For the full year, U.S. commercial revenue more than doubled, rising 109% to $1.47 billion. What makes these figures genuinely remarkable is the customer behavior underneath them. Palantir's customer count climbed 34% YOY to 954.

Not only that, the company closed $4.26 billion in contracts during Q4 alone, up 138% YOY. Existing clients are quadrupling and quintupling their commitments. This proves that once Palantir gets its foot in the door, it can start taking over operations at both businesses and government institutions very rapidly. It's a win-win for both Palantir and its clients, with one shipbuilder slashing their planning time from 160 hours to 10 minutes. A boost like that makes up for very sticky customer relationships and opens the door for further deals.

Moreover, adjusted free cash flow for Q4 hit $791 million at a 56% margin. For the full year, the metric reached $2.27 billion at a 51% margin. These figures are truly unbelievable, even for a software company.

Why the Market Is Still Saying No to PLTR Stock

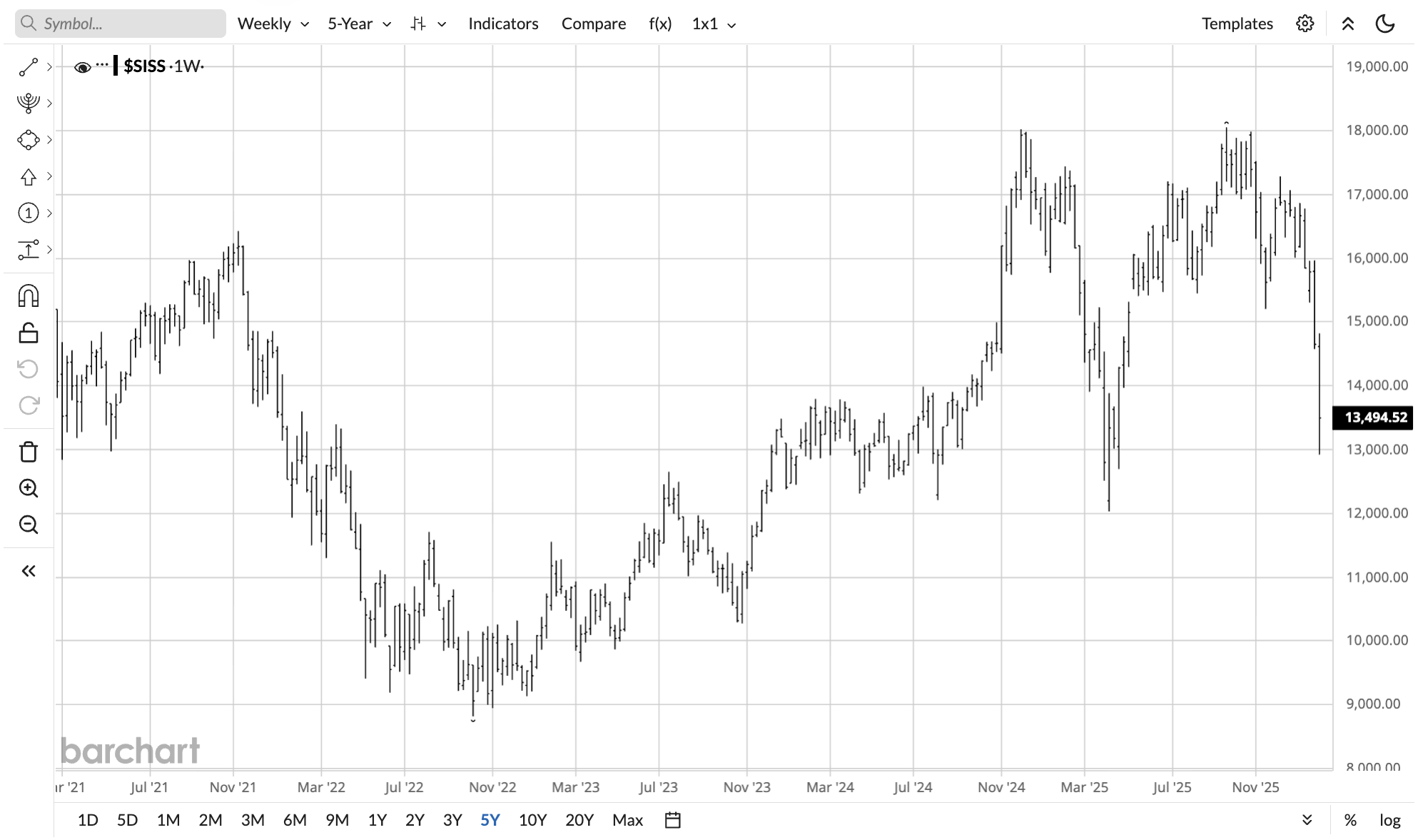

Palantir's valuation is mostly where things start going awry. The company has a spotless track record, but Wall Street is no longer willing to pay a massive premium for it. That may have a lot to do with the broader market entering a "risk-off" mode by dumping speculative assets and piling into safer ones.

Take a look at the S&P 500 Software & Services Select Industry Index (XSW), for example.

A business like Palantir won't buck the trend this time because the stock was already overdue for a correction. If anything, the selloff in Palantir is a healthy reset that will allow the fundamentals to catch up to the sky-high valuation.

Is PLTR Stock a Buy Now?

Even though PLTR stock is down 31% from its 52-week high, it remains uncomfortably expensive. PLTR stock trades at 123 times forward earnings and roughly 90 times next year's earnings. Palantir's management tends to lowball estimates, so you can assume that you're realistically paying a little less than that, but those figures remain above the norm.

Remember, the rest of the software sector is taking a dive, and investors are paying just 24 times earnings for a stock like Nvidia (NVDA). Comparing Palantir's valuation to last year looks cheap, but it's still exceptionally high against its historical valuation and peers. Forward-looking investors will realize that investors are getting pickier as AI novelty wears off. You should no longer expect Palantir to trade at 2025 premiums.

Analyst sentiment remains genuinely divided. And for the first time, Wall Street has done the exact opposite of what it would have done after such an earnings beat.

In my opinion, investors should take some time to digest these ominous signs and only accumulate software stocks that are trading at a bargain. If the sector keeps bleeding, the floor is a lot lower for PLTR stock.

Compare that to something like Microsoft (MSFT), and you'll notice that the herd will ramp up the buying pressure the moment it drops below 20 times forward earnings. PLTR stock will need to drop further before anyone calls it a bargain.

On the date of publication, Omor Ibne Ehsan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Palantir Bets on 61% Revenue Growth in 2026, Should You Buy Palantir Stock?

- Amid Capex Concerns, Should You Buy, Sell, or Hold Alphabet Stock?

- QuantumScape Just Broke Through Its 200-Day Moving Average. Should You Buy QS Stock Before Earnings?

- Oracle Heads Toward Key Resistance Levels After Analyst Upgrade. Should You Buy ORCL Stock Here?