Those looking to capitalize on the artificial intelligence revolution have plenty of avenues to go down. Of course, there are the hardware makers focused on chips, memory, and the other associated components of building high-performance computing networks and AI applications. Then, there are the application developers and those who run back-end cloud services, which really power everything to begin with.

I've been finding myself spending more time on the cloud piece of the AI puzzle, and it appears a number of other analysts from J.P. Morgan and others are doing the same. In a recent note from Morgan Stanley this past week, the investment bank noted that Alibaba (BABA) exemplifies the sort of business model that separates itself from the competition in a good way.

Here's why Alibaba is one of Morgan Stanley's top ideas as ways to play the AI revolution and what to make of this call right now.

A Chinese Tech Giant Worth Owning

J.P. Morgan analysts upgraded Alibaba to their top pick on their list of AI ideas, calling the company a “global AI winner” due to the company's vertically integrated business model that spans both the large cloud infrastructure needed to bolster the Asian AI trade and also the company's in-house semiconductor production and the expansion of homegrown AI models in China as key to this investing thesis.

Of course, there are plenty of risks to investing in Chinese companies. For American investors looking to own a piece of BABA stock via the American Depository Receipt (ADR) structure, American investors (and global investors for that matter) don't actually own a piece of the company or a say in its future cash flows. Rather, they own a receipt to a Cayman Islands company that owns a piece of the company—and that agreement between Alibaba and said Cayman Islands entity can be revoked at any time.

I think that's an integral piece to the investment puzzle that's worth pointing out, considering all the fireworks around Alibaba's former CEO Jack Ma and his ouster from power a few years back. But the reality for many investors looking for the absolute best places to put their capital to work in this space is that there are few top-tier blue-chip winners like Alibaba with the fundamentals and growth story to more than support a very juicy valuation multiple (relative to U.S. stocks, at least).

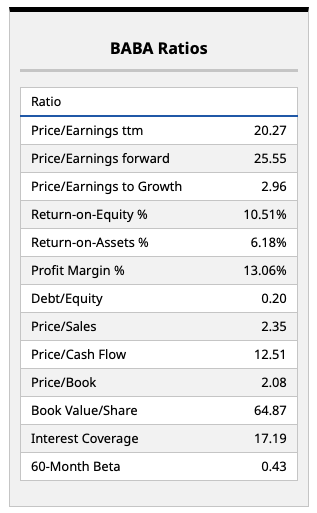

Speaking of Fundamentals

Looking at Alibaba's fundamentals below, it's clear that investors have a lot to like about this mega-cap Chinese tech giant relative to global peers. Trading around 20 times trailing earnings and around 25 times forward earnings with a double-digit profit margin, there's a lot to like about Alibaba and its ability to provide investors with sustainable capital appreciation over the long term.

Indeed, there does appear to be plenty of growth ahead to support these relatively attractive multiples, with J.P. Morgan analysts citing a combination of excess capacity to produce AI chips internally as well as the company's robust cloud infrastructure as the key pillars of the bullish thesis around this name. Now, Alibaba's growth rate has slowed in recent years, and some of that has to do with the company's sheer size. But if the underlying catalysts around internal chip production and an integrated business model provide the boost many in the market think is coming, this is a stock trading at around an 8% free cash flow yield that will start to look very attractive to many.

What Do Analysts Think?

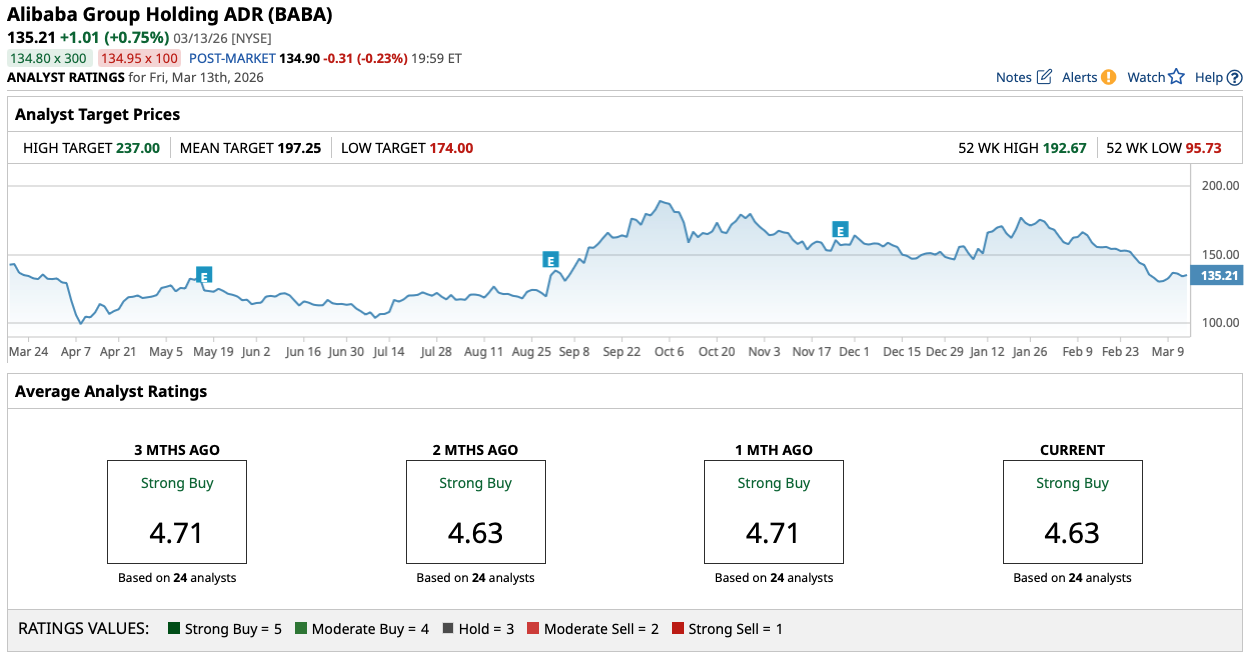

Overall, it appears most Wall Street analysts concur with J.P. Morgan, given the fact that the average $197.25 price target on BABA stock implies around 45% upside from current levels.

The reality that Alibaba has been among the biggest mega-cap losers in this tech and software selloff we've seen materialize of late is notable, considering Alibaba's rather attractive underlying fundamentals. Few U.S. stocks can come close to delivering an 8% free cash flow yield, let alone have revenue and earnings growth visibility for years to come due to spare internal capacity to produce more chips. That's a key differentiating factor investors should indeed be honing in on right now.

I remain of the view that the Chinese market is one of the most attractive for investors to consider from a fundamentals perspective. Unfortunately, the state of geopolitical risk is as high as it's been in a long time, and that's keeping me on the sidelines. For those who find themselves on the more risk-aggressive end of the spectrum, maybe that's a different story.

On the date of publication, Chris MacDonald did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart