Over the past six months, IBM has been a great trade. While the S&P 500 was flat, the stock price has climbed by 11.9% to $247.60 per share. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in IBM, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

We’re happy investors have made money, but we're cautious about IBM. Here are three reasons why there are better opportunities than IBM and a stock we'd rather own.

Why Do We Think IBM Will Underperform?

With a corporate history spanning over a century and once known for its iconic mainframe computers, IBM (NYSE: IBM) provides hybrid cloud computing platforms, AI solutions, consulting services, and enterprise infrastructure to help businesses modernize their operations.

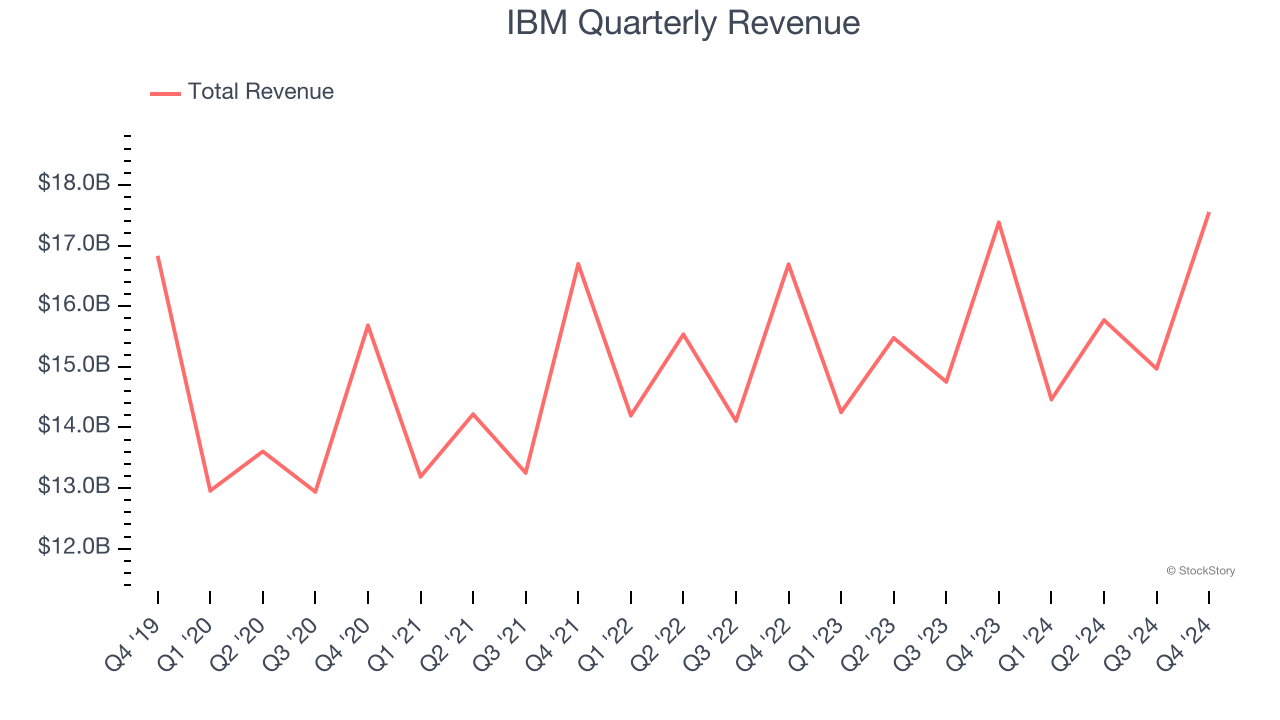

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, IBM’s sales grew at a sluggish 1.7% compounded annual growth rate over the last five years. This was below our standards.

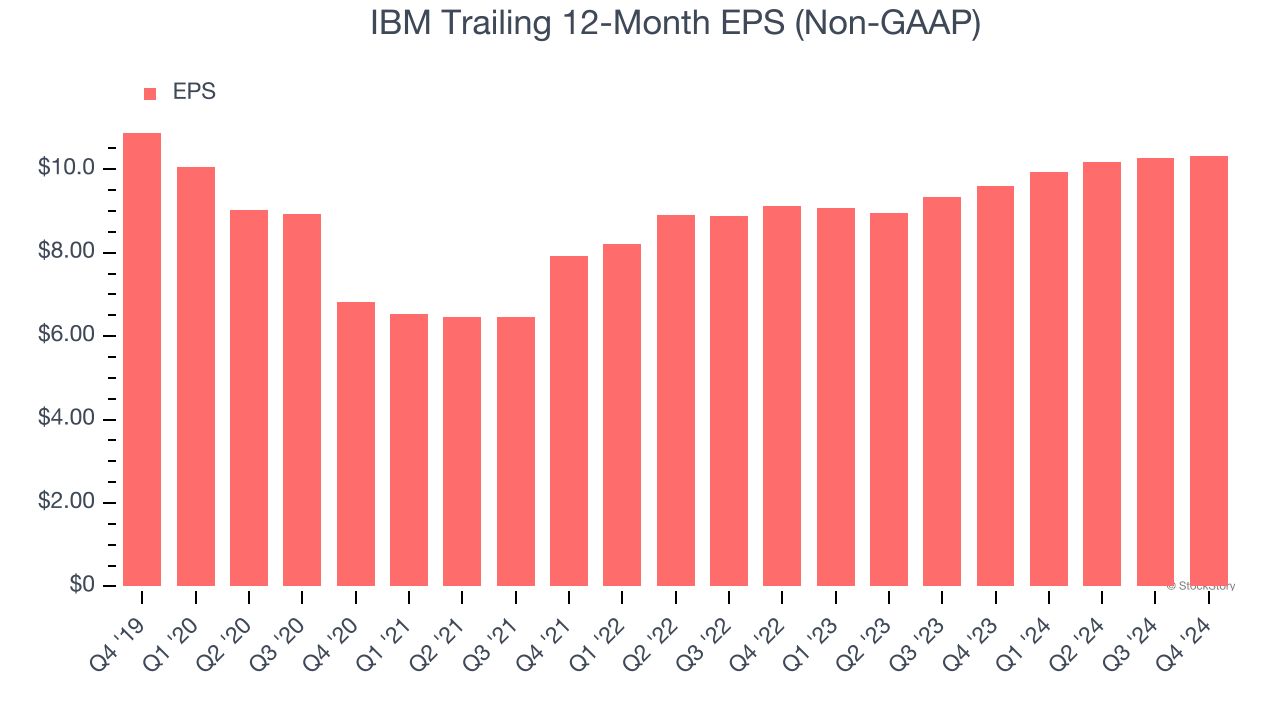

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for IBM, its EPS declined by 1% annually over the last five years while its revenue grew by 1.7%. This tells us the company became less profitable on a per-share basis as it expanded.

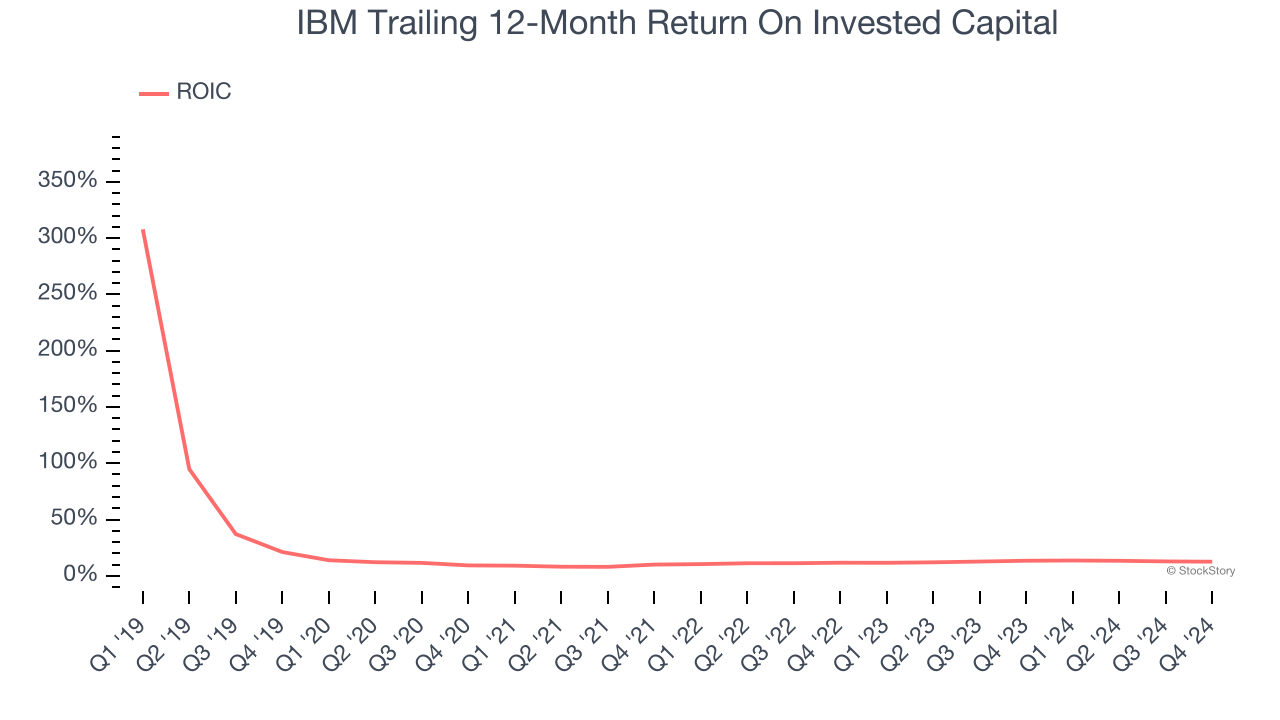

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

IBM historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 11.4%, somewhat low compared to the best business services companies that consistently pump out 25%+.

Final Judgment

IBM doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 23.3× forward price-to-earnings (or $247.60 per share). This valuation tells us a lot of optimism is priced in - you can find better investment opportunities elsewhere. We’d suggest looking at the most dominant software business in the world.

Stocks We Like More Than IBM

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.