As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the general industrial machinery industry, including JBT Marel (NYSE: JBTM) and its peers.

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand for general industrial machinery companies. Those who innovate and create digitized solutions can spur sales and speed up replacement cycles, but all general industrial machinery companies are still at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 14 general industrial machinery stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 3.3% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 6.4% since the latest earnings results.

JBT Marel (NYSE: JBTM)

Tracing back to its invention of the mechanical milk bottle filler in 1884, JBT Marel (NYSE: JBTM) designs, manufactures, and sells equipment used for food processing and aviation.

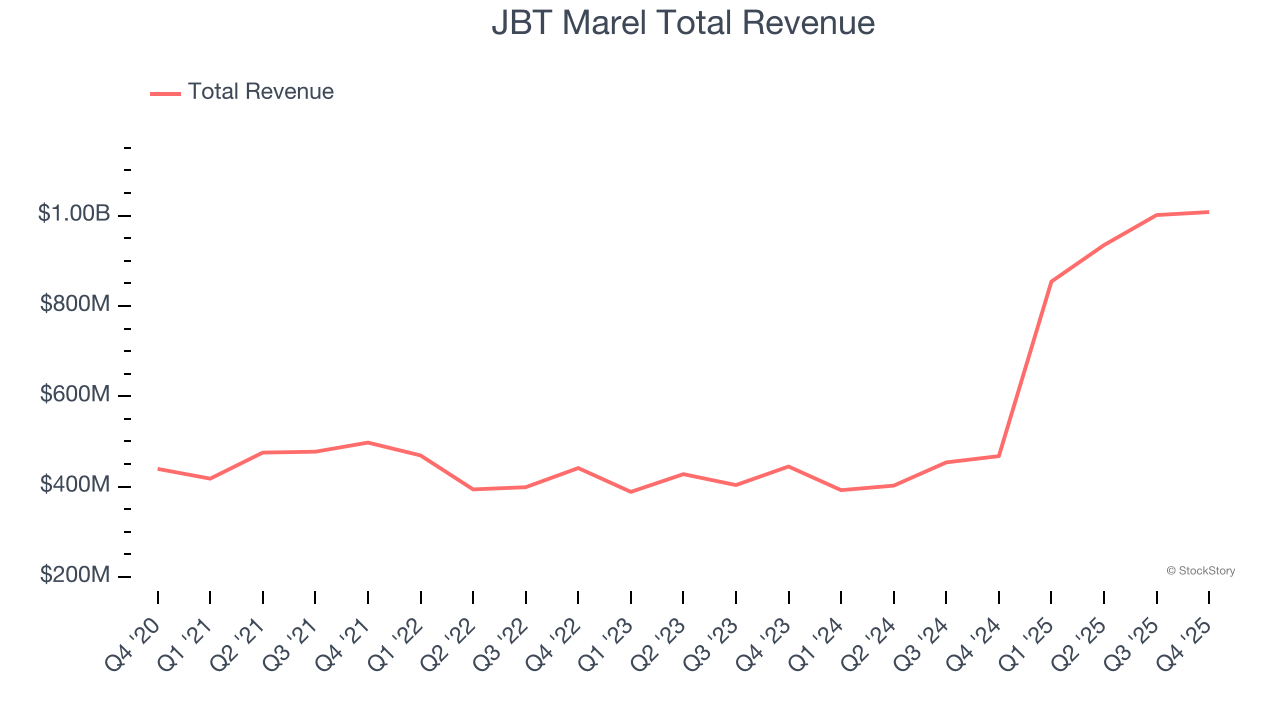

JBT Marel reported revenues of $1.01 billion, up 116% year on year. This print exceeded analysts’ expectations by 1.1%. Overall, it was a satisfactory quarter for the company with full-year EBITDA guidance exceeding analysts’ expectations but a miss of analysts’ adjusted operating income estimates.

“We delivered on our ambitious expectations for our first year operating as JBT Marel and demonstrated that we are truly better together," said Brian Deck, Chief Executive Officer.

JBT Marel pulled off the fastest revenue growth of the whole group. Even though it had a relatively good quarter, the market seems discontent with the results. The stock is down 28.9% since reporting and currently trades at $142.04.

Is now the time to buy JBT Marel? Access our full analysis of the earnings results here, it’s free.

Best Q4: Columbus McKinnon (NASDAQ: CMCO)

With 19 different brands across the globe, Columbus McKinnon (NASDAQ: CMCO) offers material handling equipment for the construction, manufacturing, and transportation industries.

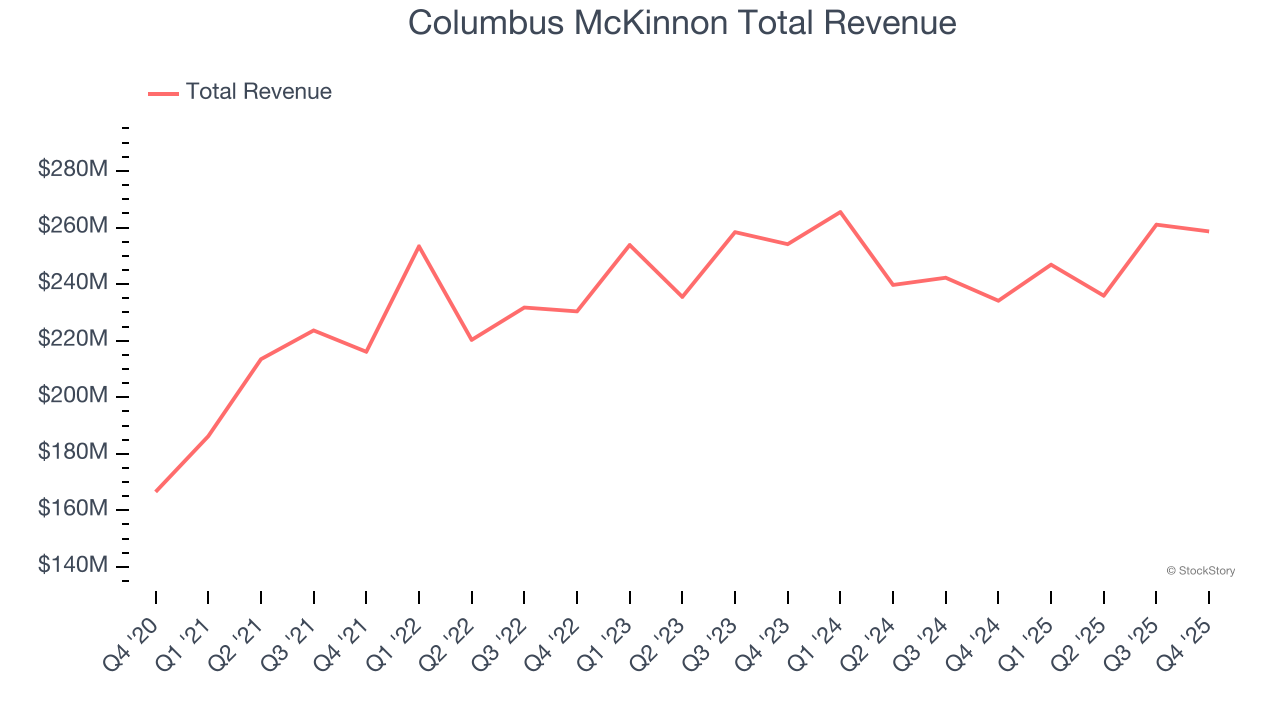

Columbus McKinnon reported revenues of $258.7 million, up 10.5% year on year, outperforming analysts’ expectations by 5.3%. The business had an exceptional quarter with an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ revenue estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 28.9% since reporting. It currently trades at $16.29.

Is now the time to buy Columbus McKinnon? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Albany (NYSE: AIN)

Founded in 1895, Albany (NYSE: AIN) is a global textiles and materials processing company, specializing in machine clothing for paper mills and engineered composite structures for aerospace and other industries.

Albany reported revenues of $321.2 million, up 12% year on year, exceeding analysts’ expectations by 16%. Still, it was a softer quarter as it posted a significant miss of analysts’ adjusted operating income estimates and a significant miss of analysts’ EBITDA estimates.

As expected, the stock is down 3.3% since the results and currently trades at $56.03.

Read our full analysis of Albany’s results here.

3M (NYSE: MMM)

Producers of the first asthma inhaler, 3M Company (NYSE: MMM) is a global conglomerate known for products in industries like healthcare, safety, electronics, and consumer goods.

3M reported revenues of $6.02 billion, up 3.7% year on year. This print beat analysts’ expectations by 1.5%. More broadly, it was a mixed quarter as it also produced a solid beat of analysts’ revenue estimates but a slight miss of analysts’ adjusted operating income estimates.

The stock is down 8.8% since reporting and currently trades at $153.10.

Read our full, actionable report on 3M here, it’s free.

L.B. Foster (NASDAQ: FSTR)

Founded with a $2,500 loan, L.B. Foster (NASDAQ: FSTR) is a provider of products and services for the transportation and energy infrastructure sectors, including rail products, construction materials, and coating solutions.

L.B. Foster reported revenues of $160.4 million, up 25.1% year on year. This result surpassed analysts’ expectations by 1%. Taking a step back, it was a slower quarter as it logged a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ EPS estimates.

L.B. Foster scored the highest full-year guidance raise among its peers. The stock is down 12.8% since reporting and currently trades at $28.06.

Read our full, actionable report on L.B. Foster here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.