Let’s dig into the relative performance of Capital One (NYSE: COF) and its peers as we unravel the now-completed Q4 credit card earnings season.

Credit card companies facilitate electronic payments and extend revolving credit to consumers. Growth comes from increasing digital payment adoption, cross-border transaction growth, and value-added services for cardholders and merchants. Challenges include regulatory scrutiny of fees and practices, competition from alternative payment methods, and potential credit losses during economic downturns.

The 6 credit card stocks we track reported a mixed Q4. As a group, revenues missed analysts’ consensus estimates by 0.5%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 7.2% since the latest earnings results.

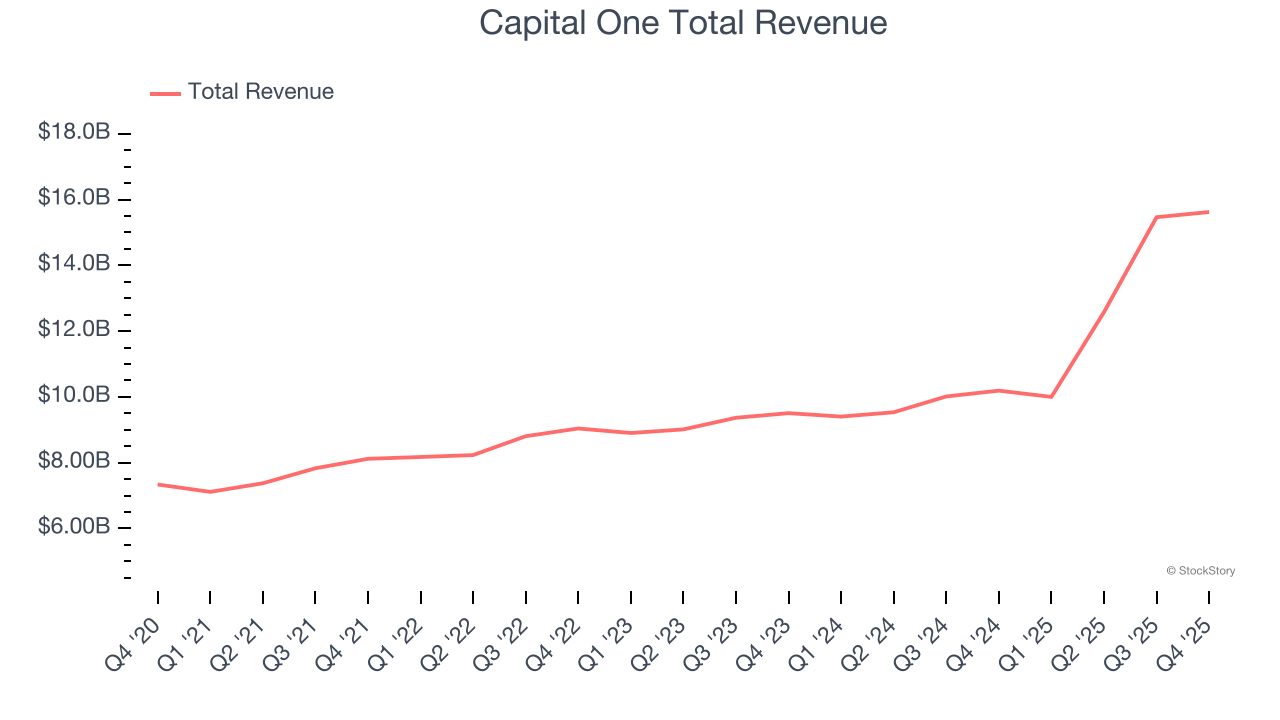

Capital One (NYSE: COF)

Starting as a credit card company in 1988 before expanding into a full-service bank, Capital One (NYSE: COF) is a financial services company that offers credit cards, auto loans, banking services, and commercial lending to consumers and businesses.

Capital One reported revenues of $15.62 billion, up 53.3% year on year. This print exceeded analysts’ expectations by 0.9%. Despite the top-line beat, it was still a slower quarter for the company with a significant miss of analysts’ EPS estimates and a miss of analysts’ net interest margin estimates.

Capital One achieved the fastest revenue growth of the whole group. Still, the market seems discontent with the results. The stock is down 5.5% since reporting and currently trades at $193.52.

Is now the time to buy Capital One? Access our full analysis of the earnings results here, it’s free.

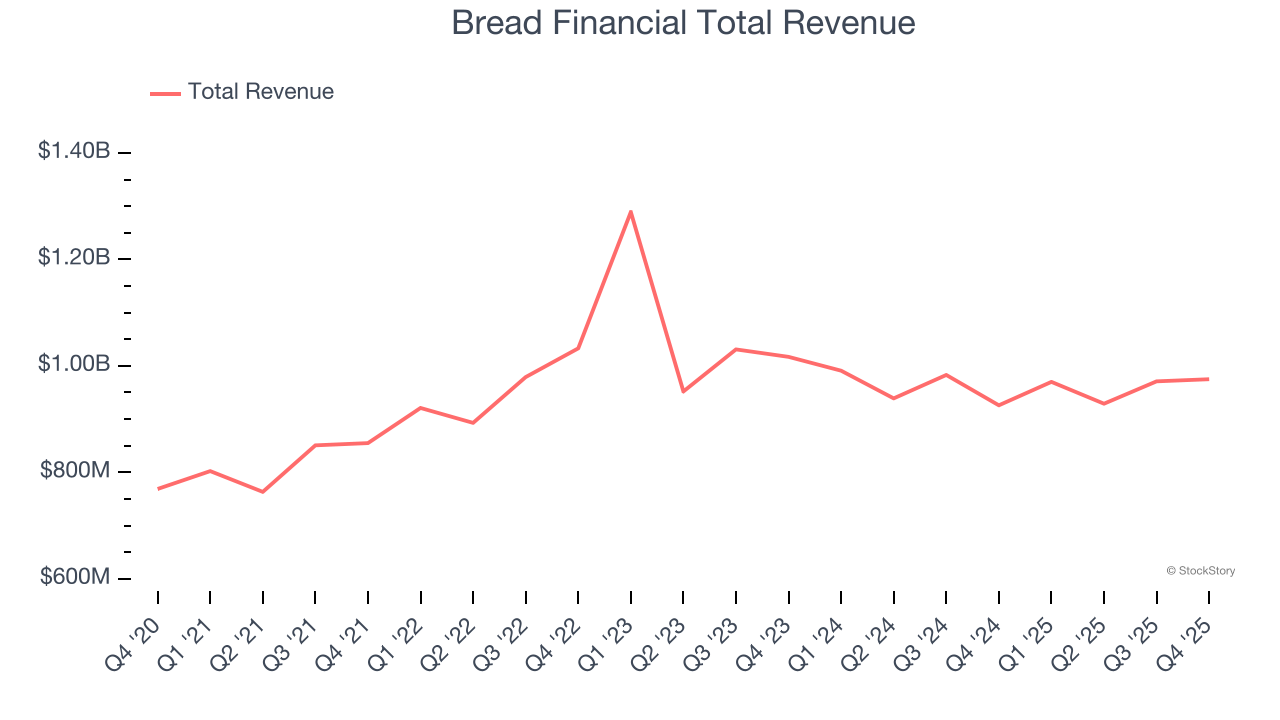

Best Q4: Bread Financial (NYSE: BFH)

Formerly known as Alliance Data Systems until its 2022 rebranding, Bread Financial (NYSE: BFH) provides credit cards, installment loans, and savings products to consumers while powering branded payment solutions for retailers and merchants.

Bread Financial reported revenues of $975 million, up 5.3% year on year, outperforming analysts’ expectations by 2.2%. The business had an exceptional quarter with a beat of analysts’ EPS estimates and a solid beat of analysts’ net interest margin estimates.

Bread Financial pulled off the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 5.5% since reporting. It currently trades at $71.98.

Is now the time to buy Bread Financial? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: American Express (NYSE: AXP)

Recognizable by its iconic green logo and the slogan "Don't leave home without it," American Express (NYSE: AXP) is a global payments company that issues credit and charge cards, processes merchant transactions, and offers travel and lifestyle benefits to consumers and businesses.

American Express reported revenues of $17.57 billion, up 10.6% year on year, falling short of analysts’ expectations by 7.2%. It was a softer quarter as it posted a significant miss of analysts’ revenue estimates and a miss of analysts’ EPS estimates.

American Express delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 14.4% since the results and currently trades at $306.95.

Read our full analysis of American Express’s results here.

Mastercard (NYSE: MA)

Recognizable by its iconic "Priceless" advertising campaign that has run in over 120 countries, Mastercard (NYSE: MA) operates a global payments network that connects consumers, financial institutions, merchants, and businesses, enabling electronic transactions and providing payment solutions.

Mastercard reported revenues of $8.81 billion, up 17.6% year on year. This print met analysts’ expectations. It was a strong quarter as it also logged a beat of analysts’ EPS estimates and a decent beat of analysts’ EBITDA estimates.

The stock is flat since reporting and currently trades at $517.

Read our full, actionable report on Mastercard here, it’s free.

Visa (NYSE: V)

Processing over 829 million transactions daily and connecting billions of cards to 150 million merchant locations worldwide, Visa (NYSE: V) operates one of the world's largest electronic payments networks, facilitating secure money movement across more than 200 countries through its VisaNet processing platform.

Visa reported revenues of $10.9 billion, up 14.6% year on year. This result beat analysts’ expectations by 2%. Overall, it was a satisfactory quarter as it also recorded a decent beat of analysts’ revenue estimates.

The stock is down 4.2% since reporting and currently trades at $317.82.

Read our full, actionable report on Visa here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.