Palantir Technologies (PLTR) is once again at the center of a Wall Street debate. After a blistering rally in 2025 that cemented its status as one of the market’s top AI winners, PLTR stock has pulled back sharply this year, caught in a broader software selloff and renewed scrutiny over lofty valuations. Yet just as sentiment began to cool, Mizuho Securities stepped in with a fresh vote of confidence, upgrading the stock to “Outperform.” Mizuho’s Gregg Moskowitz described Palantir as being “in a category of one,” pointing to a rare combination of explosive revenue growth and expanding margins that he argues is unmatched in the software space.

Still, PLTR remains one of the market’s most richly valued stocks, even after its recent pullback. That premium valuation continues to divide investors: bulls see a uniquely positioned AI software standout with a long runway, while skeptics question whether expectations are already too high. So is Mizuho right that Palantir stands in a “category of one”—and that now is the time to buy? Let’s take a closer look at what’s driving the upgrade and what it means for PLTR stock today.

About Palantir Technologies Stock

Palantir Technologies develops and deploys software platforms for the intelligence community, commercial enterprises, and government entities around the globe. It offers a range of platforms, such as Palantir Gotham, Foundry, Apollo, and the Artificial Intelligence Platform. It currently has a market cap of $323.5 billion.

Palantir’s key platforms include Gotham, designed for detecting patterns in large datasets for defense and intelligence agencies, and Foundry, which functions as a central operating system for data across multiple industries. Apollo is the company’s cloud-agnostic platform that enables seamless software updates, while the Artificial Intelligence Platform (AIP) leverages generative AI models to improve decision-making across commercial and government sectors.

After a blockbuster performance in 2025, shares of the analytics software provider have slumped 27% so far this year. PLTR stock has been caught up in the recent software-sector selloff and the broader deterioration in sentiment toward AI. Concerns that the company’s valuation had outpaced its fundamentals also weighed on the stock.

Despite the recent pullback from its record highs, Palantir remains one of the most expensive names in the market, trading at a forward non-GAAP P/E of 102.56x, though still below Tesla’s (TSLA) 200x multiple.

Palantir Wins Upgrade as Mizuho Says It’s “In a Category of One”

Last week, Palantir Technologies’ stock earned a new vote of confidence on Wall Street. Mizuho Securities analyst Gregg Moskowitz upgraded the stock to “Outperform” from “Neutral” and reiterated his $195 price target. The analyst argued that Palantir is “in a category of one,” given its revenue growth and margin expansion, calling it “unlike anything else in software.” PLTR stock gained 1.8% last Wednesday following the upgrade.

Mizuho had previously taken a cautious stance on PLTR stock amid concerns about a potential sharp valuation pullback. “We had for months stated a concern that PLTR shares could suddenly be subject to meaningful multiple reversion at some point,” Moskowitz wrote. He noted that a de-rating now appears to have taken place, highlighting a 46% decline in the company’s 2026 estimated EV/FCF multiple during the first six weeks of the year. Mizuho believes “the risk/reward is now attractive.”

Moskowitz remains optimistic about the company’s outlook. “While PLTR is surely not immune to macro risk, rapid expansion into production environments suggests many customers are seeing clear [ROI], undercutting the view that growth is driven by short-term AI hype,” he said. The analyst pointed to continued strength in Palantir’s U.S. commercial division (which we’ll examine in more detail shortly), adding that upside to the company’s guidance of at least 115% growth in 2026 for the business “is very likely.” He also highlighted Palantir’s overseas performance, noting especially strong growth in the UK “despite some broader European spending caution.” In December, Palantir won its largest-ever UK defense contract, a roughly $328 million award from the Ministry of Defence to support Britain’s military operational decision-making over a three-year period.

Mizuho believes Palantir can sustain government revenue growth of over 40% for the next two years, supported by rising geopolitical tensions and continued contract wins. “More broadly, we remain steadfast in our view that PLTR is increasingly well-positioned to benefit from long-term trends in AI, government digital transformation, and industrial modernization,” Moskowitz wrote.

Interestingly, William Blair’s Louie DiPalma also upgraded PLTR stock to “Outperform” in early February, just before the company’s Q4 earnings report, after maintaining a negative stance on the shares for several years. The analyst pointed to valuation as the key reason for the upgrade after the stock’s selloff since the start of the year.

Palantir Delivers Blowout Q4 Results

In early February, Palantir once again delivered blowout quarterly results, reinforcing its position as a standout player in AI software. The company’s fourth-quarter revenue stood at a record $1.41 billion, up 70% year-over-year (YoY) and 19% quarter-over-quarter (QoQ). That figure came in well above analysts’ expectations of $1.34 billion. Moreover, the company reported net income of $609 million, marking another quarterly record. Its adjusted earnings per share (EPS) were 25 cents, beating expectations by 2 cents and up from 14 cents a year earlier.

CEO Alex Karp noted that Palantir’s results “have again exceeded even our most ambitious expectations.” “Such a massive acceleration in growth, for a company of this scale and size, is a remarkable achievement—a cosmic reward of sorts to those who were interested in advancing our admittedly idiosyncratic project and embraced, or at least did not wholly reject, our mode of working,” Karp said.

As in prior quarters, revenue growth was largely fueled by Palantir’s core U.S. business, where sales surged 93% YoY. Both Palantir’s U.S. commercial and U.S. government segments delivered strong performance. Commercial revenue was the clear standout, jumping 137% YoY to $507 million, while revenue from U.S. government contracts stood at $570 million, up 66% YoY. Both figures exceeded analyst expectations. Swissquote analyst Ipek Ozkardeskaya said the surge in the company’s U.S. revenue is “a sign that AI hype is now turning into hard budgets—exactly what investors have been waiting to see.” Notably, U.S. quarterly revenue surpassed the $1 billion mark for the first time.

While Palantir’s revenue growth was already impressive, its total contract value (TCV) was even more remarkable. TCV represents the total potential lifetime value of contracts signed with or awarded by the company’s customers at the time they are executed. With that, the company signed contracts worth $4.26 billion during the fourth quarter, up 138% YoY, including 61 deals each valued at over $10 million.

Looking ahead, Palantir said it expects 2026 revenue to range between $7.182 billion and $7.198 billion. That implies a very solid 61% YoY growth at the midpoint, supported by projected 115% YoY growth in the U.S. commercial segment.

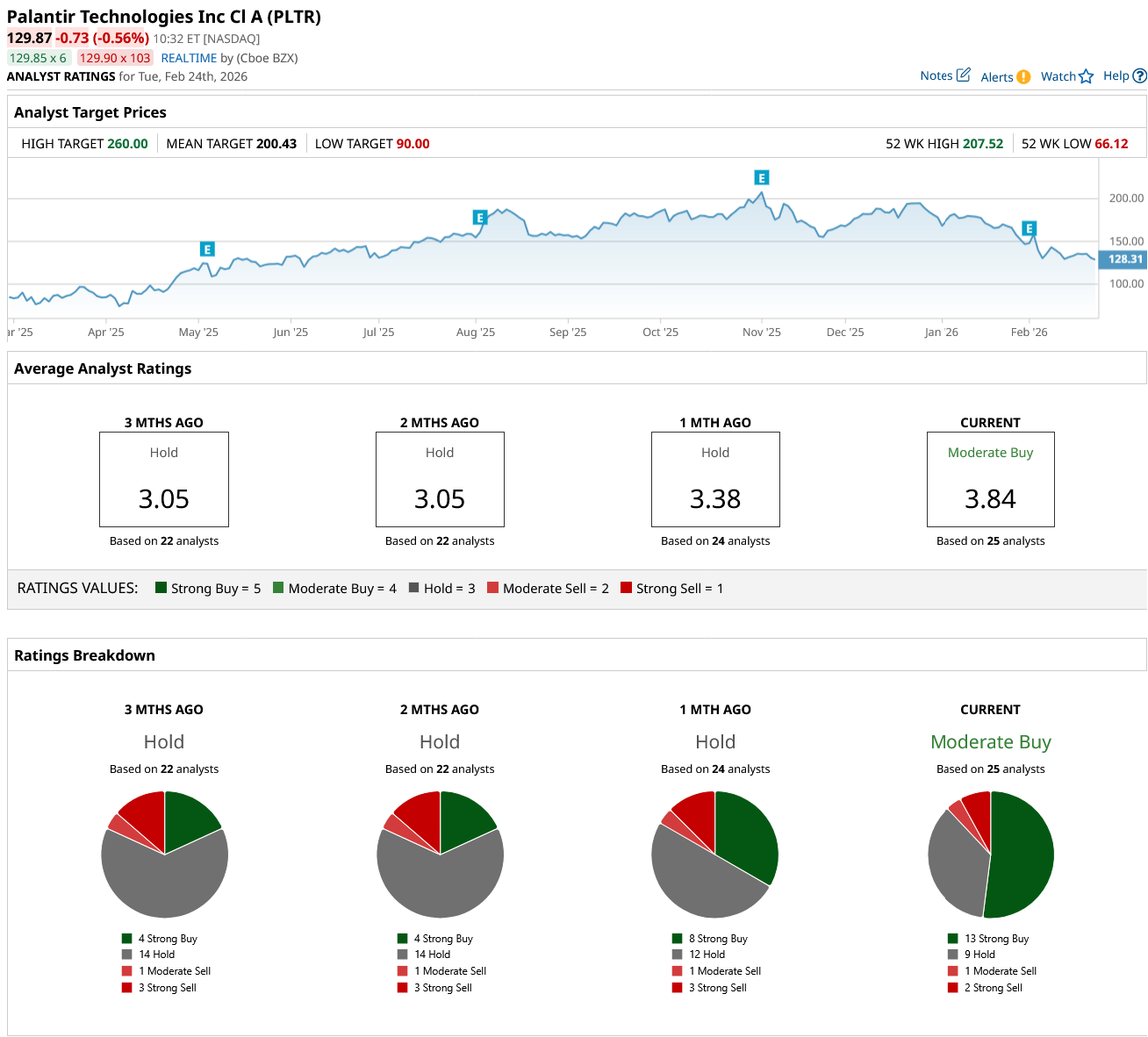

What Do Analysts Expect for PLTR Stock?

The broader Wall Street community seems to share Mizuho’s Moskowitz’s view, as reflected in the stock’s “Moderate Buy” consensus rating. Interestingly, PLTR stock had a “Hold” consensus rating just a month ago, suggesting that the recent pullback, combined with strong growth prospects, is prompting more analysts to turn bullish. Among the 25 analysts covering the stock, 13 assign a “Strong Buy” rating, nine recommend holding it, one rates it a “Moderate Sell,” and two have issued a “Strong Sell” rating. The mean price target for PLTR stock stands at $200.43, implying 48.2% upside potential from Friday’s closing price.

On the date of publication, Oleksandr Pylypenko did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart