Shares of Advanced Micro Devices (AMD) closed 8.8% up on Feb. 24 after the company announced an expansion of its partnership with Meta Platforms (META). Under the new multi-year agreement, Meta will use AMD’s Instinct graphics processing units (GPUs) to power up to 6 gigawatts of artificial intelligence (AI) infrastructure. AMD’s expanding partnership network and large planned deployments strengthen its competitive position in the global AI buildouts.

This deal also strengthens AMD’s position as the leading alternative to Nvidia (NVDA) in high-performance AI chips. Nvidia currently dominates the AI GPU market, but AMD has been steadily building relationships across the industry. In addition to Meta, the company counts OpenAI and Oracle (ORCL) among its AI-focused partners. As more major players adopt AMD hardware, investor confidence in AMD’s long-term AI strategy, including an ambitious earnings target, is likely to improve and support its share price.

Coming back to the Meta deal, the partnership goes beyond GPUs. Meta has already deployed millions of AMD EPYC server processors across its data centers, and the two companies are deepening that relationship. Meta will be a lead customer for AMD’s upcoming sixth-generation EPYC chips, code-named “Venice,” as well as a new processor, “Verano,” designed to deliver strong performance while minimizing power consumption and cost.

Part of the agreement is the performance-based warrant that AMD issued to Meta for up to 160 million shares of stock. These shares will vest in stages as Meta purchases increasing volumes of AMD’s Instinct GPUs, starting with the first gigawatt of shipments and scaling up to six gigawatts. Additional conditions tie vesting to certain stock price levels and technical milestones.

Although issuing new shares may raise concerns about dilution, this partnership is expected to generate significant revenue growth over the next several years and increase AMD’s adjusted earnings per share. Further, the deal could support AMD’s long-term financial targets and boost the market’s confidence in its broader AI strategy.

Is AMD Stock a Buy?

AMD is a compelling stock to buy now. The company’s growing share in the fast-growing AI chip market and expanding partner network suggest that the momentum in its business could continue, supporting its share price.

A major catalyst for AMD is its data center business. This segment has been expanding rapidly, driven by rising demand for its server processors and AI accelerators. In particular, the rollout of the Instinct MI350 series GPUs has significantly boosted revenue. At the same time, AMD continues to gain market share in servers, taking business from competitors as customers seek high-performance alternatives.

Demand from large cloud providers remains strong. Hyperscalers are investing heavily to expand their infrastructure to handle growing cloud usage and AI workloads. These investments are translating into higher demand for AMD’s server chips. Beyond cloud companies, enterprises are also upgrading aging data centers, further supporting sales of AMD’s EPYC processors.

Looking ahead, AMD’s product pipeline adds to the growth story. The upcoming Venice CPU is already attracting strong customer interest, especially from large cloud operators planning major deployments. Broad support from original equipment manufacturers is expected when the chip launches later this year, which could accelerate adoption.

Given the strength of its EPYC and Instinct product roadmaps, AMD appears well-positioned to deliver rapid growth in its data center business over the next several years. Revenue from this segment is projected to rise at a CAGR of more than 60% over the next three to five years. Moreover, the data center AI business’s revenue is expected to grow at a CAGR of more than 80%, driven by increasing customer demand and its next-generation Instinct products and systems.

Valuation is another factor that makes AMD stock compelling. AMD currently trades at a forward price-to-earnings (P/E) ratio of 35.5, which looks attractive given analysts' expectations of 72.5% earnings growth in 2026 and another 60% in 2027. With strong growth prospects and an attractive valuation, AMD stock appears to be a buy.

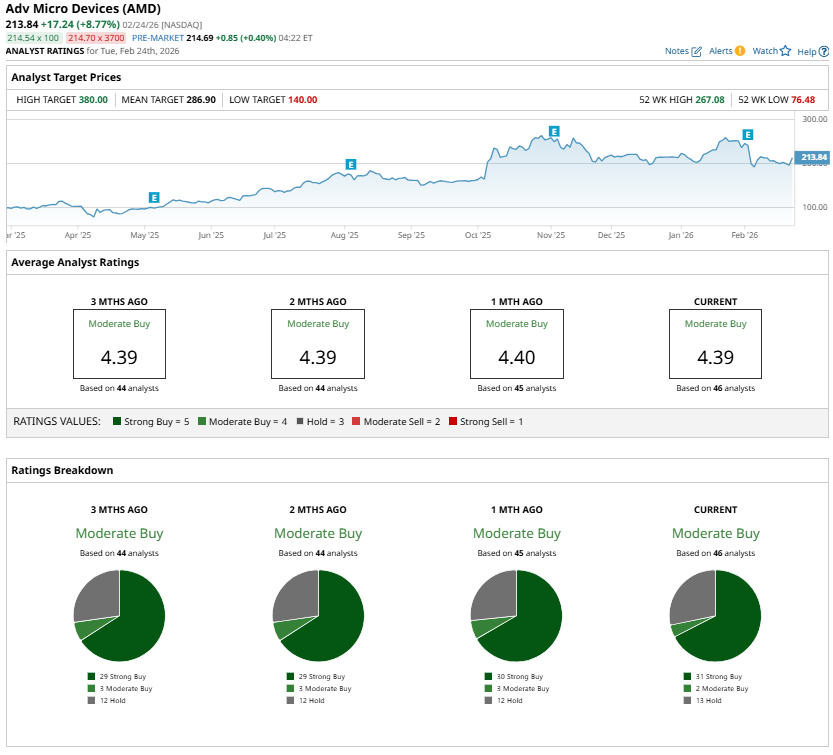

Analysts are cautiously optimistic about AMD stock and maintain a “Moderate Buy” consensus rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Ken Griffin, Ray Dalio, and Warren Buffett All Sold More Apple Stock. Should You?

- As Circle Stock Breaks Through Key Resistance Levels, Should You Chase the CRCL Rally?

- RIVN Stock 2026 Forecast: What to Expect as Rivian Sees ‘Inflection Year’

- Huge Volume in Netflix Call Options Today Shows Investors are Bullish on NFLX Stock