Adeia's (ADEA) licensing deal with major chipmaker AMD (AMD) appears to leave Adeia poised to obtain a large amount of revenue from chipmakers, while ADEA reported superb fourth-quarter financial results. Moreover, Wall Street analysts are very bullish on the company's outlook, and the valuation of its stock is quite attractive. Yet all these positive points are tinged with a significant amount of revenue fluctuation.

In light of all of these points, I view ADEA as a buy for only some investors.

About ADEA Stock

Adeia develops technologies through R&D and then licenses them to other firms. Its hybrid bonding offerings allow chips “to be bonded with ultra-fine pitch 3D electrical interconnects at room temperature without pressure or adhesives.” According to the company, hybrid bonding "delivers high reliability and enhanced thermal performance." The company has also developed new cooling solutions for chips. Additionally, Adeia provides technology that enables consumers to more easily find, watch, and interact with video content on multiple devices.

In Q4, the firm's revenue soared to $182.6 million versus $119.17 million during the same period a year earlier, while its operating income jumped to $108.75 million compared with $57.48 million in Q4 of 2024.

ADEA stock has a low forward price-earnings ratio of 18.8 times and a market capitalization of $2.17 billion.

The AMD Deal and Its Implications

On March 9, Adeia reported that AMD had agreed to sign a multi-year deal that will provide the chip maker with “access to Adeia’s…semiconductor intellectual property (IP) portfolio.” Further, under the deal, all outstanding litigation between the firms will be settled.

In a note to investors, investment bank Rosenblatt indicated that the agreement bodes well for Adeia's ability to sign similar deals and reach $100 million of annual revenue from semiconductor firms, up from $26 million in 2025. Also noteworthy is that Rosenblatt raised its price target on ADEA stock to $40 from $30 and kept a “Buy” rating on the name.

Moreover, research firm Trefis stated that the AMD agreement “validates the strength and necessity of Adeia's semiconductor (intellectual property) portfolio, while the simultaneous litigation settlement removes a significant risk and cost overhang, allowing management to focus on growth and future collaboration.”

Optimistic Analysts and an Attractive Valuation

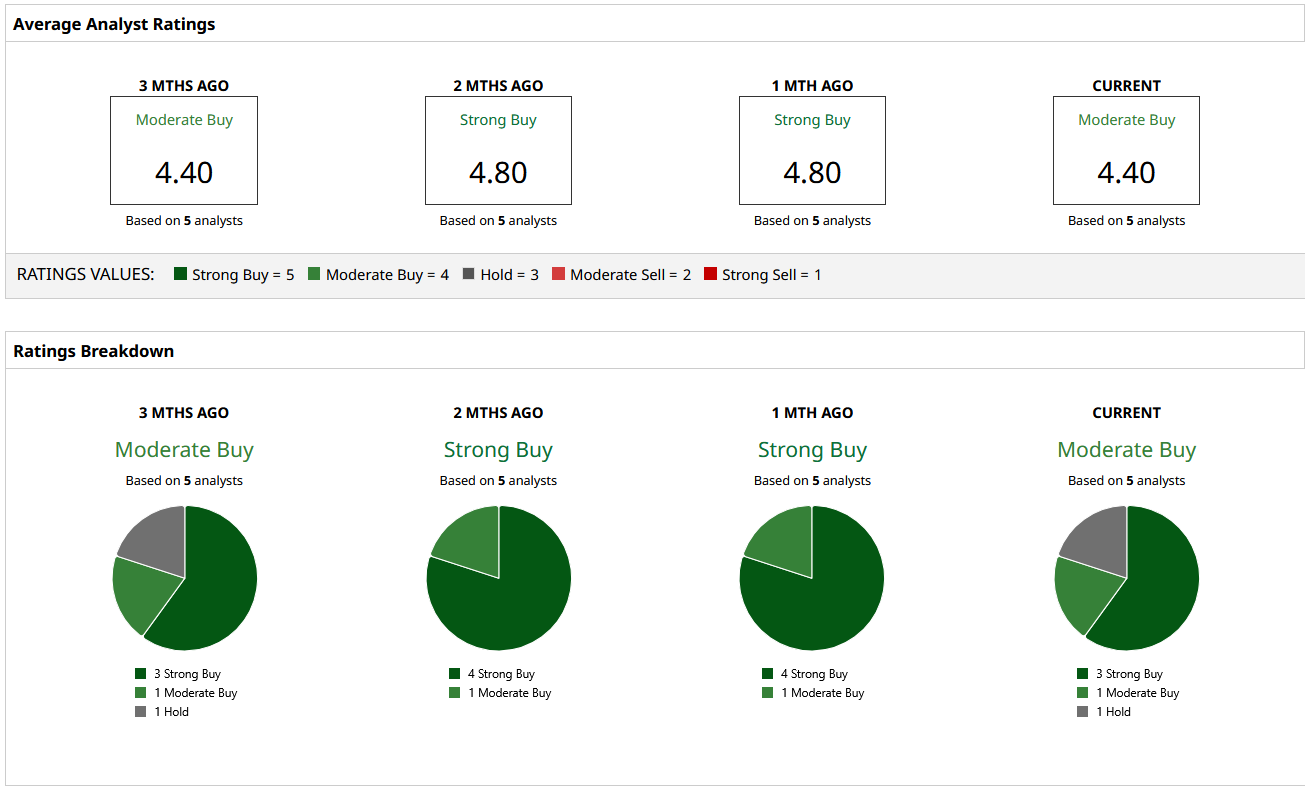

Out of the five analysts covering ADEA stock, three have a “Strong Buy” rating on it, one has a “Moderate Buy” rating, and one has a “Hold” rating. That is a rather bullish combined outlook. Meanwhile, given the company's strong growth and upbeat prognosis, its forward price-earnings ratio of 18.8 times is quite low.

The Bottom Line

With Adeia's semiconductor revenue looking poised to keep expanding rapidly in the wake of the AMD deal and the firm changing hands at a low valuation, ADEA stock appears to be a good choice for growth investors. However, historically, Adeia's revenue has fluctuated a great deal, as it generated revenue of $516 million in 2020, $391 million in 2021, $439 million in 2022, and $389 million in 2023.

Therefore, although I think the proliferation of semiconductors due to AI has enabled the firm to reach a positive turning point, I view the name as somewhat risky, and I recommend that only risk-tolerant growth investors buy ADEA stock.

On the date of publication, Larry Ramer did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart