CoreWeave (CRWV) unveiled its fiscal first-quarter results last week, showcasing what appeared to be robust operational momentum in the competitive AI cloud computing space. Yet, the market's reaction was devastating: shares plunged nearly 19% on Friday, erasing billions in market value. Shares are down over 57% from their 52-week high.

Investors—already jittery about the company's trajectory amid intensifying competition and economic headwinds—found little reassurance in the report. The primary culprits were CoreWeave's underwhelming guidance that fell short of lofty expectations and a ballooning debt load that overshadowed any positives.

For a stock grappling with pre-existing concerns over profitability and capital intensity, these earnings served only to amplify anxieties rather than dispel them.

Strong Growth Signals Amid AI Demand Surge

The results painted a mixed picture with undeniable strengths on the surface. Revenue growth remained impressive, reflecting the surging demand for AI infrastructure, and the company's contracted backlog swelled dramatically to $66.8 billion, with an average contract duration of five years. Yet CoreWeave missed analyst EPS estimates of a $0.61 loss with wider losses of $0.84.

This backlog—fueled by commitments from hyperscalers, AI startups, and enterprises—signals strong future visibility and positions CoreWeave as a key player in the AI boom. Adjusted EBITDA margins also held firm in the quarter, underscoring its operational efficiency in core activities.

Hoisting Red Flags

However, these highlights were quickly eclipsed by red flags that fueled the selloff.

- Debt levels tripled year-over-year (YoY) as the company ramped up investments in data centers and GPU acquisitions to meet demand.

- Share count more than doubled through dilutive financing, eroding per-share value.

- Losses expanded significantly, with net deficits widening due to spiking expenses in sales, marketing, and infrastructure buildouts—costs essential for scaling but painful in the short term.

- Guidance for the upcoming quarter projected revenue below consensus estimates, suggesting a potential slowdown that clashed with the narrative of unchecked growth.

This earnings release has ignited a heated debate among market observers on the sustainability of CoreWeave's model. On one side, noted short-seller Jim Chanos questioned the company's accounting practices, particularly the use of an extended 10-year depreciation schedule for GPUs, which is longer than the typical six-year industry norm. He argues this inflates reported profitability by deferring costs, and when factoring in full economic expenses, the firm remains deeply unprofitable.

He also expressed concern about CoreWeave's growing debt burden, with high interest payments potentially overwhelming operational gains, leading to persistent negative pre-tax income in coming quarters. His doubts extended to the backlog's quality—whether these long-term contracts are as ironclad as portrayed or vulnerable to cancellations amid shifting AI priorities.

Rittenhouse Research countered that such criticism overlooks the transformative growth potential in AI, where upfront investments pave the way for outsized returns. It emphasized that margin compression is temporary, with management forecasting a rebound, and that the backlog's scale validates the strategy despite near-term pain.

Wall Street Ignores the Turmoil, Remains Bullish

Wall Street, for its part, appears largely unfazed by the turmoil. Deutsche Bank upgraded CRWV from “Hold” to “Buy,” lifting its price target from $100 to $140, citing confidence in the company's AI leadership. Similarly, DA Davidson raised its target from $110 to $125, highlighting resilient demand.

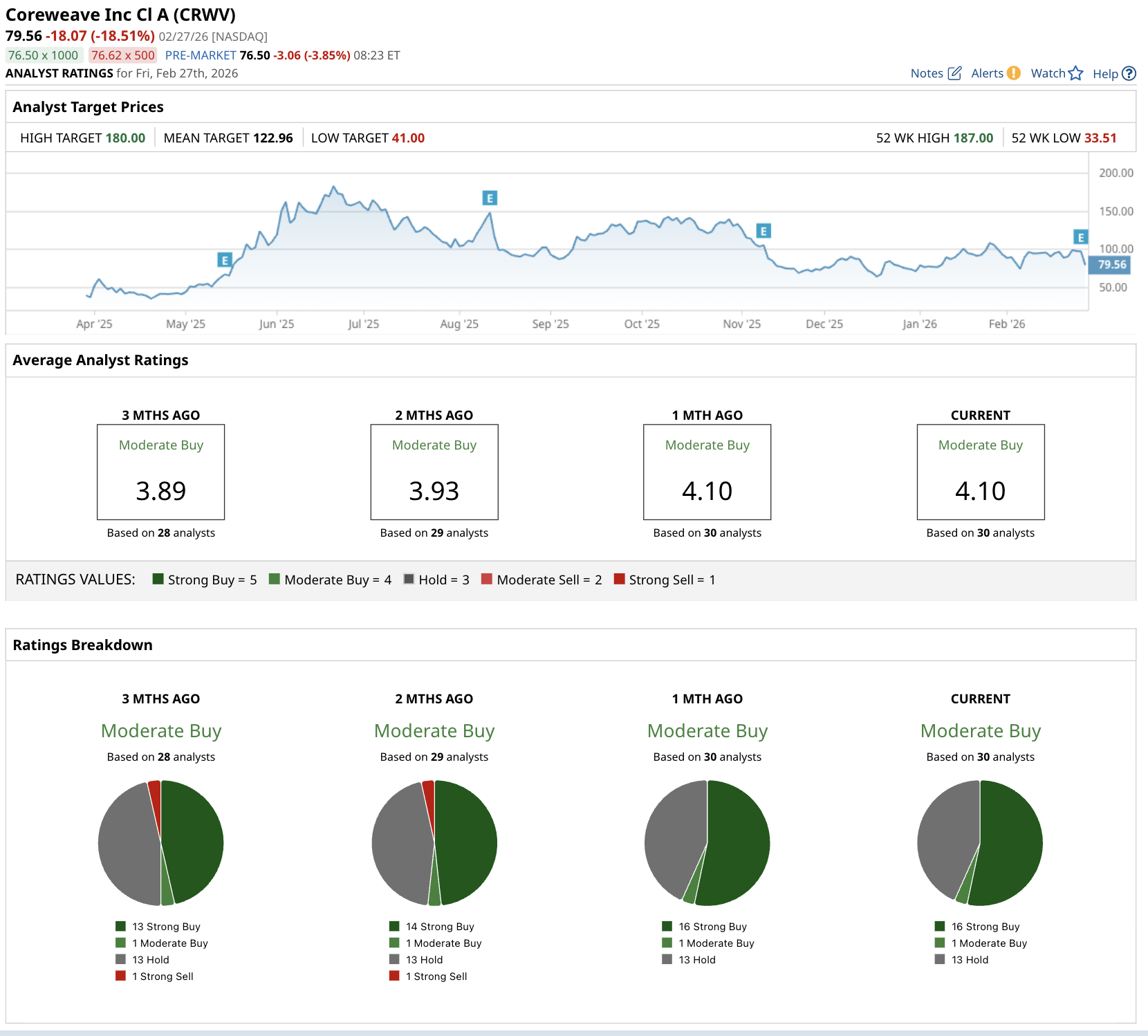

Overall, among the 30 analysts covering the stock, the consensus rating is a "Moderate Buy," with a mean price target of $122.96, implying about 54.5% upside potential from current levels.

Key Takeaway

The market's sharp rebuke contrasts starkly with analysts' optimism, as the Q1 results failed to ease longstanding worries over mounting debt, dilution, and profitability hurdles in a capital-intensive industry.

Until CoreWeave demonstrates that this quarter marks the trough—as management asserts—and delivers on its promises of margin recovery and growth acceleration through the year, CRWV stock seems to be at best a hold stance for cautious investors.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart