The artificial intelligence (AI) boom has unleashed an insatiable appetite for data centers, the very backbone powering this technological revolution. And the scale of expansion is nothing short of extraordinary. Across North America, data center construction is accelerating so rapidly that growth is now spilling far beyond traditional strongholds. For years, Virginia has held the crown as the world’s largest data center market. But that dominance may soon shift.

According to a new report from JLL, Texas is on track to unseat Virginia, a moment the firm describes as a true “inflection point” for the industry. The numbers tell the story. Roughly 64% of the massive 35-gigawatt construction pipeline is now rising outside so-called mature markets like Virginia. Meanwhile, vacancy rates remain extraordinarily tight. At the end of 2025, data center vacancies stood at just 1%, marking the second consecutive year at this historic low.

“The data center sector has officially entered hyperdrive,” said Andy Cvengros, executive managing director and co-lead of U.S. data center markets at JLL. He emphasized that record-low vacancy sustained over two consecutive years pushes back firmly against bubble fears, especially considering that nearly the entire construction pipeline is already spoken for by investment-grade tenants. In fact, about 92% of the capacity currently under construction is pre-committed.

Additionally, JLL highlights another eye-catching figure. The top five hyperscalers are planning a staggering $710 billion in capital expenditures in 2026 alone to build out the infrastructure needed to support this next wave of digital growth. Against this powerful backdrop, here’s a closer look at two top-rated stocks that appear perfectly positioned to benefit from this accelerating data center expansion story.

Stock #1: Amazon

Seattle-based Amazon.com (AMZN) may be best known for reinventing online shopping, but its evolution into a full-scale technology powerhouse has been nothing short of remarkable. What began as an e-commerce disruptor has transformed into a company deeply embedded in cloud computing, artificial intelligence, data centers, and digital entertainment. Today, Amazon shapes how people shop, stream, work, and even build the next generation of technology.

The company’s footprint in entertainment alone is massive. From Prime Video and Amazon Music to gaming and Twitch, Amazon has secured a meaningful share of the global streaming and digital content market. At the same time, Amazon Web Services (AWS) sits squarely at the center of the cloud and AI boom, providing the backbone infrastructure that powers startups, enterprises, and global corporations alike. And Amazon is doubling down on AI in a big way.

In late February, the company announced a multi-year strategic partnership with OpenAI designed to accelerate AI innovation for businesses, startups, and consumers around the world. As part of the agreement, Amazon will invest a substantial $50 billion in OpenAI, beginning with an initial $15 billion investment, followed by an additional $35 billion in the coming months once certain conditions are satisfied. But despite Amazon’s sweeping AI ambitions, its stock has yet to fully reflect that bold vision.

Valued at roughly $2.3 trillion by market capitalization, Amazon shares are down 9.8% so far in 2026 and -1.92% over the past year. The main culprit behind the muted performance is the investor reaction to the company’s eye-popping $200 billion capital expenditure forecast for the year, a clear signal that Amazon is aggressively investing in AI, data centers, and robotics. By comparison, the broader S&P 500 Index ($SPX) is up marginally in 2026 and delivered a solid 15% gain in 2025.

Amazon’s fiscal 2025 fourth-quarter earnings report, released on Feb. 5, delivered blockbuster scale but also sparked cautious investor reaction. The company posted a staggering $213.4 billion in revenue, up 14% year-over-year (YOY) and comfortably ahead of Wall Street’s $211.5 billion estimate. A major driver of that growth was AWS, where revenue surged 24% annually to $35.6 billion, underscoring the continued strength of cloud and AI-related demand.

Also, other business segments turned in solid performances. North America sales climbed 10% YOY to $127.1 billion, while the international segment grew even faster, rising 17% to $50.7 billion. On the surface, it was a quarter that showcased Amazon’s sheer operating scale across multiple geographies and divisions.

Yet despite the top line strength, the stock came under immediate pressure, falling more than 5% in the sessions that followed. Investors were weighing a slight earnings-per-share miss alongside the company’s sizable capital spending plans. Quarterly EPS rose 4.8% YOY to $1.95 but came in just below analyst expectations of $1.98.

More importantly, CEO Andy Jassy signaled an aggressive acceleration in AI infrastructure investment. Amazon guided for an eye-catching $200 billion in capital expenditures for 2026. While some of that spending will support core retail operations and non-AI workloads, Jassy emphasized that the majority is aimed at expanding the generative AI stack, including new data centers and custom silicon such as Trainium and Graviton.

In fact, Trainium and Graviton have surpassed a combined $10 billion annual revenue run rate, growing at a triple-digit YOY pace as demand for Amazon’s custom chips accelerates. Looking ahead, Amazon projected first-quarter 2026 revenue in the range of $173.5 billion to $178.5 billion, representing 11% to 15% growth. Operating income is expected to fall between $16.5 billion and $21.5 billion, compared with $18.4 billion in the first quarter of 2025.

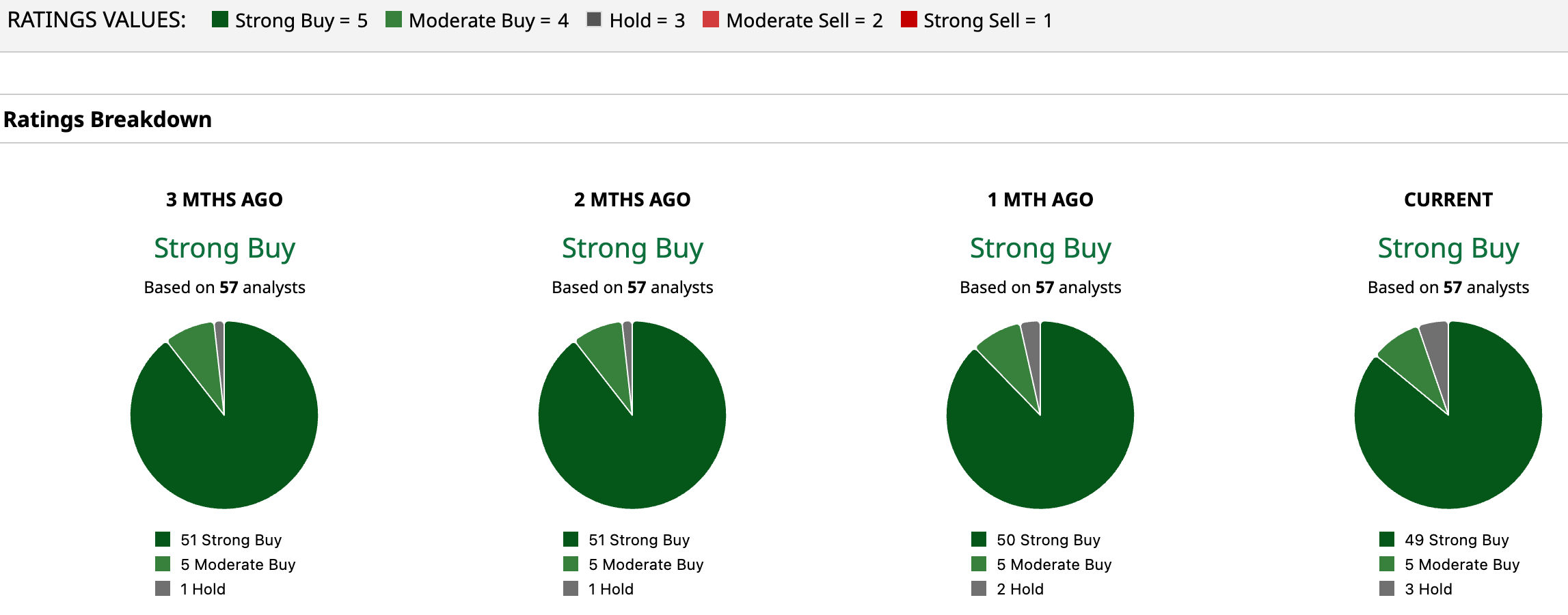

Even with recent share price volatility, Wall Street’s conviction hasn’t wavered. Amazon holds a consensus “Strong Buy” rating overall, with 49 of 57 analysts calling it a “Strong Buy,” five issuing “Moderate Buy,” and just three sitting at “Hold.” The average price target of $285.65 points to roughly 37.5% upside, while the Street-high target of $360 suggests shares could soar as much as 73% from current levels.

Stock #2: Broadcom

California-based Broadcom (AVGO) is a major player in the global technology landscape, developing semiconductors and infrastructure software that underpin many of today’s most demanding digital systems. Its products are widely used in data centers, networking equipment, broadband services, wireless communications, storage platforms, and enterprise software environments, areas that form the backbone of modern connectivity and cloud computing.

Broadcom is increasingly becoming a central player in the AI infrastructure buildout. In 2026, a substantial portion of its growth is being fueled by custom AI chips and high-speed networking components that connect thousands of GPUs inside large-scale AI clusters. With a market capitalization of roughly $1.5 trillion, Broadcom remains one of the largest players in the semiconductor space.

Nevertheless, the stock has not been immune to broader technology sector volatility, declining about 8.86% so far in 2026 as macro and tech headwinds weigh on sentiment. Taking a step back, however, the longer-term trajectory remains notable. Over the past year, Broadcom shares have surged approximately 58.16%, comfortably outpacing the broader market’s more modest double-digit gains during the same stretch.

Broadcom lifted the curtain on its impressive fiscal 2025 fourth-quarter earnings report on Dec. 11, and the results sailed past Wall Street’s expectations on both the top and bottom lines. During the quarter, the chip giant delivered record quarterly revenue of $18.02 billion, marking a 28% YOY increase and comfortably beating the $17.5 billion consensus estimate.

A major driver of that strength was a remarkable 74% surge in AI-related semiconductor revenue, underscoring Broadcom’s position as a key beneficiary of the massive capital spending underway by hyperscale cloud providers. Looking deeper into the numbers, semiconductor solutions revenue climbed 35% YOY to $11.1 billion, while infrastructure software revenue rose 19% annually to nearly $7 billion.

Profitability was equally impressive, highlighting the company’s high-margin operating model. Broadcom reported non-GAAP earnings per share of $1.95, up 37% YOY and ahead of the $1.87 consensus estimate. Adjusted EBITDA for the quarter jumped 34% annually to $12.2 billion. Looking ahead to the first quarter, with results expected to be announced on Wednesday, March 4 after market close, the momentum appears set to continue.

For the upcoming quarter, AI semiconductor revenue is expected to double YOY to $8.2 billion, driven by continued demand for custom AI accelerators and Ethernet AI switches. In addition, the chipmaker is projecting total revenue of approximately $19.1 billion, with adjusted EBITDA reaching 67% of revenue.

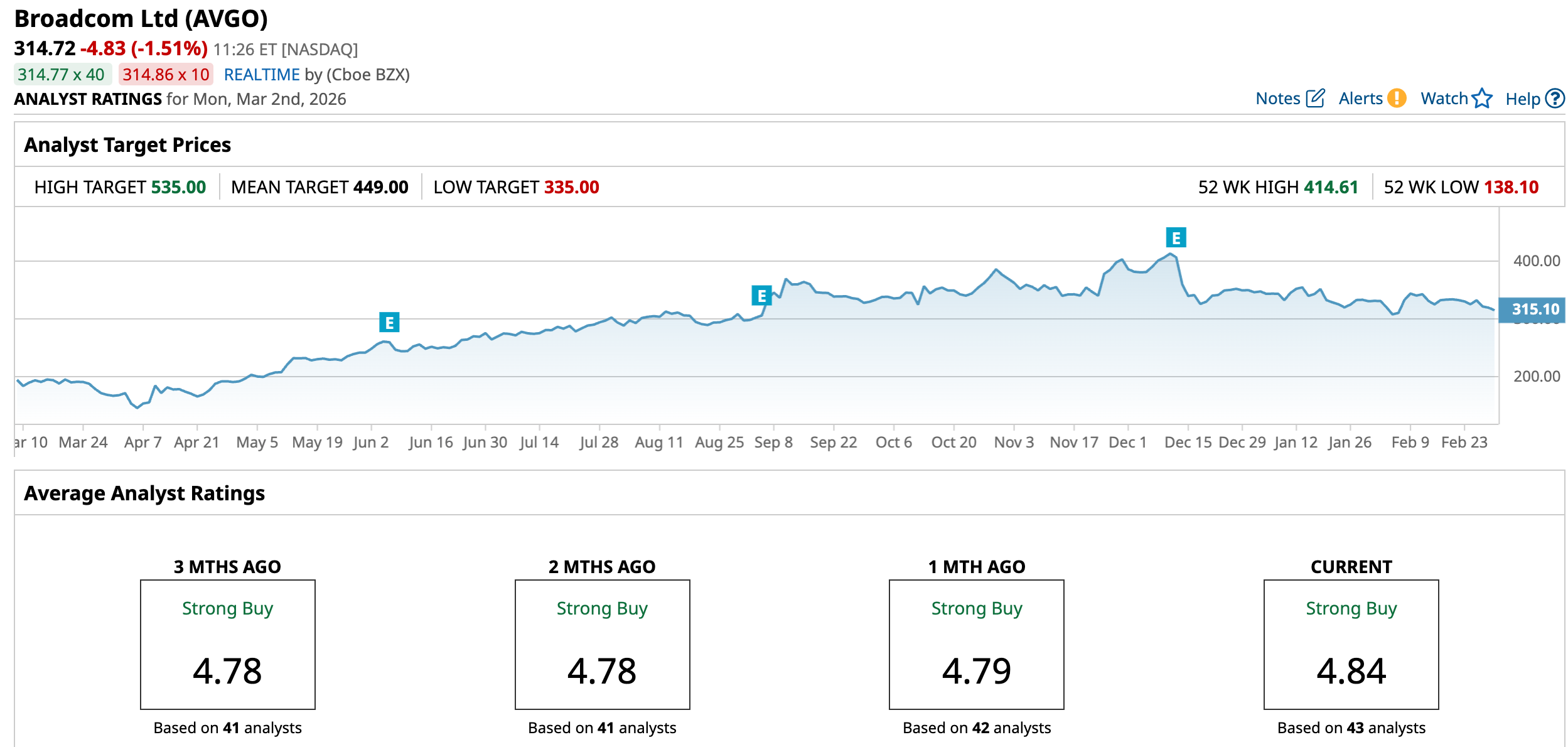

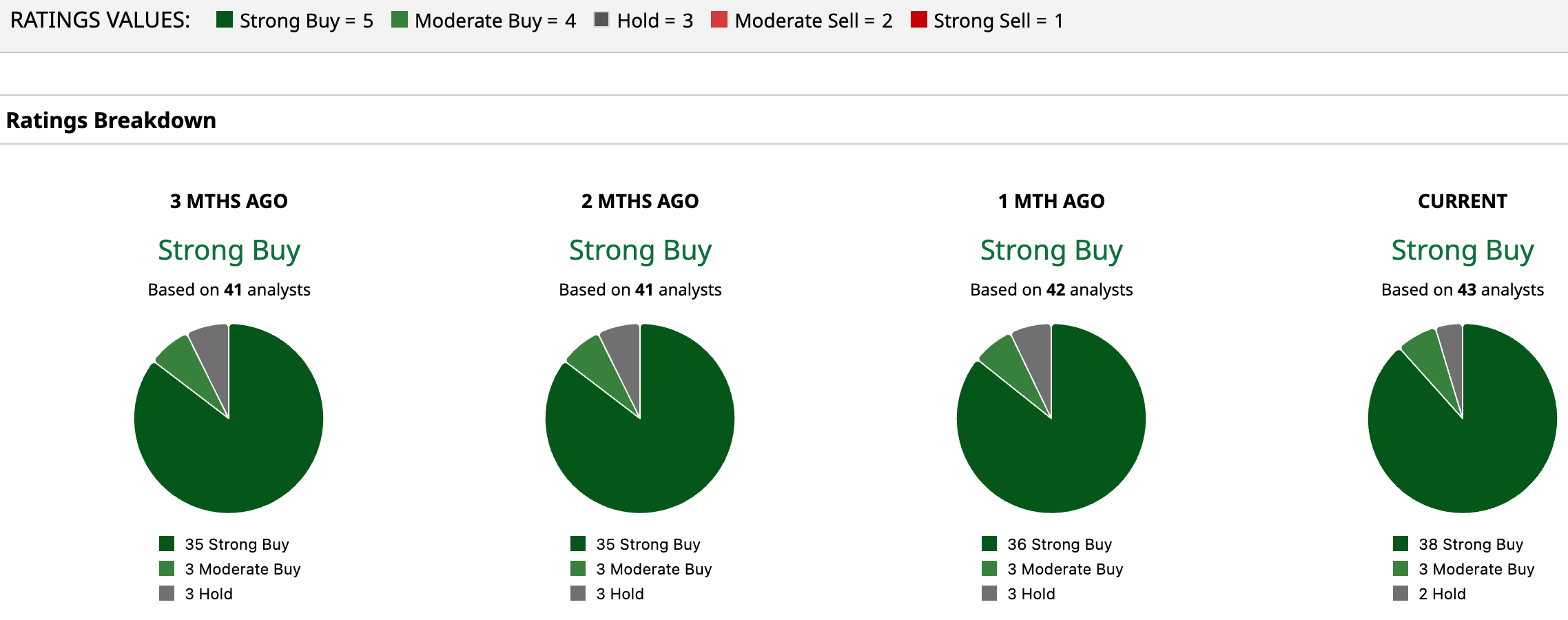

Overall, Wall Street’s confidence in Broadcom remains firmly intact. The stock carries a consensus “Strong Buy” rating, reflecting solid conviction in its long-term prospects. Out of 43 analysts covering the company, 38 rate it a “Strong Buy,” three recommend a “Moderate Buy,” and only two suggest to “Hold” the shares. The upside implied by price targets is also notable.

The average target of $449 points to potential gains of about 42.7%, while the Street-high estimate of $535 suggests shares could climb as much as 70% from current levels.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart