CoreWeave (CRWV) had a solid 2025. Then, it told investors what to expect in the first quarter of 2026, and the stock dropped hard.

Shares of the artificial intelligence (AI) cloud infrastructure provider fell more than 18% on Friday after the company issued Q1 guidance that came in well below analysts' expectations. That's a painful single-day move for any stock. But does it change the longer-term picture? That's the more important question.

Let's break down the numbers and what management actually said.

What Did CoreWeave Report in Q4?

On the surface, the fourth quarter was strong.

- CoreWeave posted revenue of $1.57 billion, up 110% year-over-year and slightly above the consensus of $1.55 billion.

- Its contracted revenue backlog grew to $66.8 billion, up more than $11 billion from the prior quarter and more than 4x higher than a year ago.

- Active power capacity hit 850 megawatts across 43 data centers, ahead of the roughly 827 megawatts analysts had projected.

- Adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) came in at $898 million, just below the $929 million consensus.

- The adjusted loss per share was $0.56 per share, worse than the $0.49 per share loss analysts had expected.

So the quarter itself was mixed, but mostly solid. The issue was what came next.

Why CoreWeave Stock Tanked 18% on Friday

CoreWeave guided for Q1 revenue of $1.9 billion to $2 billion, significantly missing estimates of $2.29 billion.

CoreWeave also flagged that Q1 will be the trough for margins this year. CFO Nitin Agrawal said that adjusted operating income for Q1 would come in between $0 and $40 million, with margins expected to ramp through the rest of the year and return to low-double-digits by Q4.

Why the squeeze? CoreWeave is spending aggressively to build out capacity. The company brought on 260 megawatts of active power in Q4, roughly one-third of its entire installed base at the start of the quarter. That kind of rapid expansion means data-center costs and depreciation hit the income statement before the associated revenue fully ramps.

CEO Mike Intrator was direct about the tradeoff on the earnings call. "Our margins reflect the cost of building tomorrow's revenues," he said.

For 2026 overall, CoreWeave expects $12 billion to $13 billion in revenue. That's roughly in line with the $12.09 billion consensus. It's also planning to spend $30 billion to $35 billion in capital expenditures, more than double its 2025 capex, with management saying substantially all of it is tied to already signed customer contracts.

The Bull Case: $66.8 Billion in Backlog Doesn't Lie

Here's what matters for anyone trying to assess whether the selloff is an overreaction.

CoreWeave's revenue backlog grew to $66.8 billion — a figure representing hard, contracted customer commitments, not projections. Every contract in that backlog is expected to begin generating revenue by year-end 2026, according to management.

The weighted average contract length has also expanded from four years to five years, meaning customers are locking in for longer. New customers in Q4 included names like Midjourney, Cursor, Cognition, and Mercado Libre (MELI), alongside expanded relationships with existing hyperscale partners, including both of its current major cloud customers.

Management also guided for an annualized revenue run rate of $17 billion to $19 billion at exit in 2026, and more than $30 billion at exit in 2027.

Demand signals remain strong across the board. Nvidia's (NVDA) H100 GPUs, the backbone of CoreWeave's platform, stayed roughly flat year-over-year in Q4, while older A100 pricing increased, a sign that supply remains tight and demand isn't slowing.

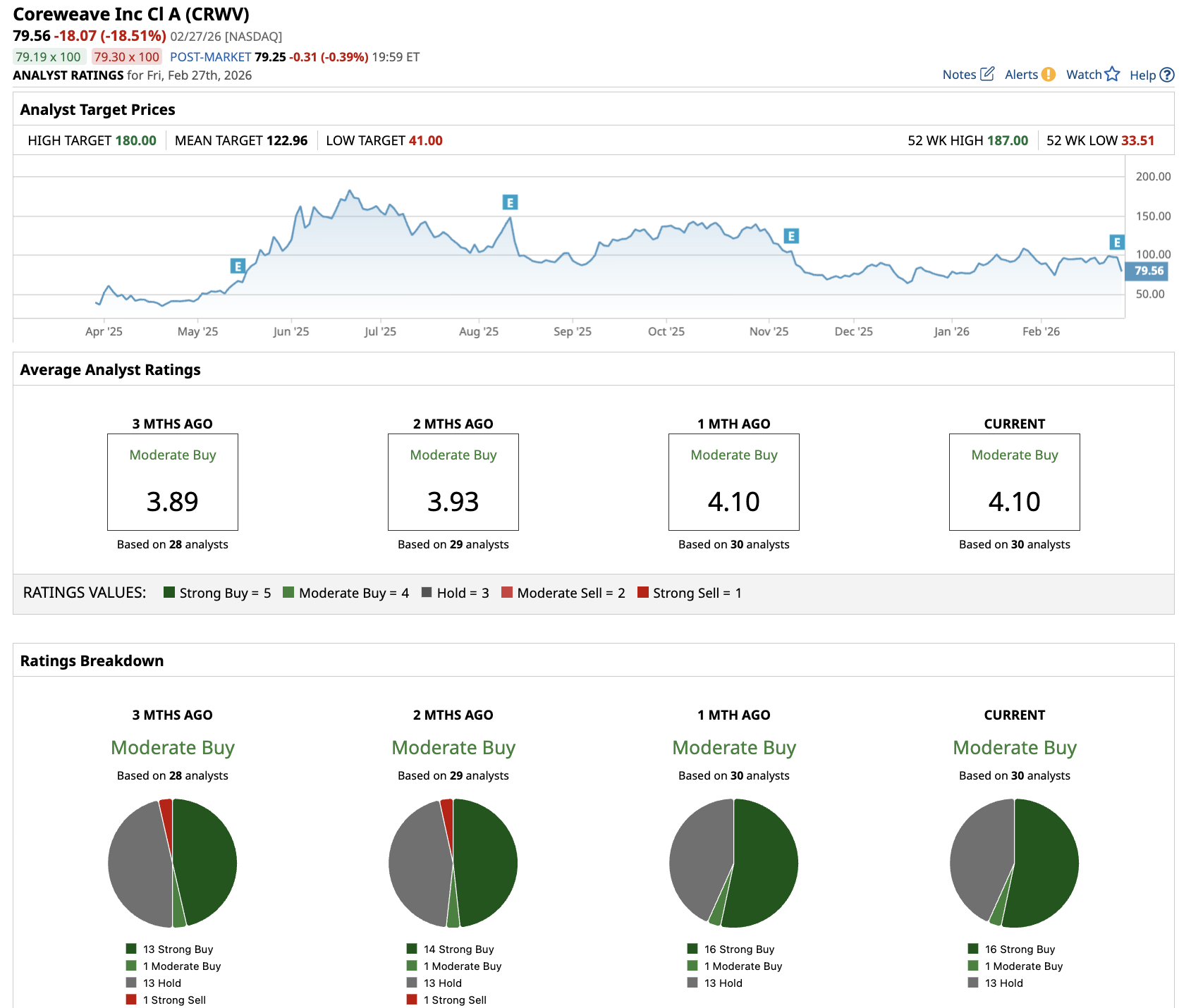

What Is the CRWV Stock Price Target?

The 18% pullback in CoreWeave stock offers investors an opportunity to buy the dip. Moreover, the AI infrastructure stock is also down more than 50% from all-time highs.

A $66.8 billion backlog, 110% revenue growth, and a customer list that includes Alphabet's (GOOG) (GOOGL) Google and OpenAI are not the hallmarks of a business in trouble. It indicates that the business is spending heavily to capture a window of opportunity that may not stay open forever.

The key risk is execution. CoreWeave is betting that it can keep deploying infrastructure at breakneck speed while costs eventually normalize and margins recover. If the demand holds and the build-out stays on schedule, the numbers management is projecting for 2027 and beyond could look very conservative.

Out of the 30 analysts covering CoreWeave stock, 16 recommend “Strong Buy,” four recommend “Moderate Buy,” and 13 recommend “Hold.” The average CRWV stock price target is $123, well above the current price of $80.

CoreWeave is not a stock for the faint-hearted. But for investors with a multi-year horizon, the selloff may be worth a closer look.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart