Global defense spending is rising as the Middle East tension escalates, along with the ongoing Russia-Ukraine war and the U.S.–China tensions in the Indo-Pacific. When conflicts rise, governments worldwide are forced to boost military budgets, which is why defense stocks are surging now. In 2025 global military expenditure reached an estimated $2.63 trillion, up from $2.48 trillion the year before. As geopolitical tensions continue rising, defense contractors with large backlogs, combat-proven systems, and strong government ties could benefit.

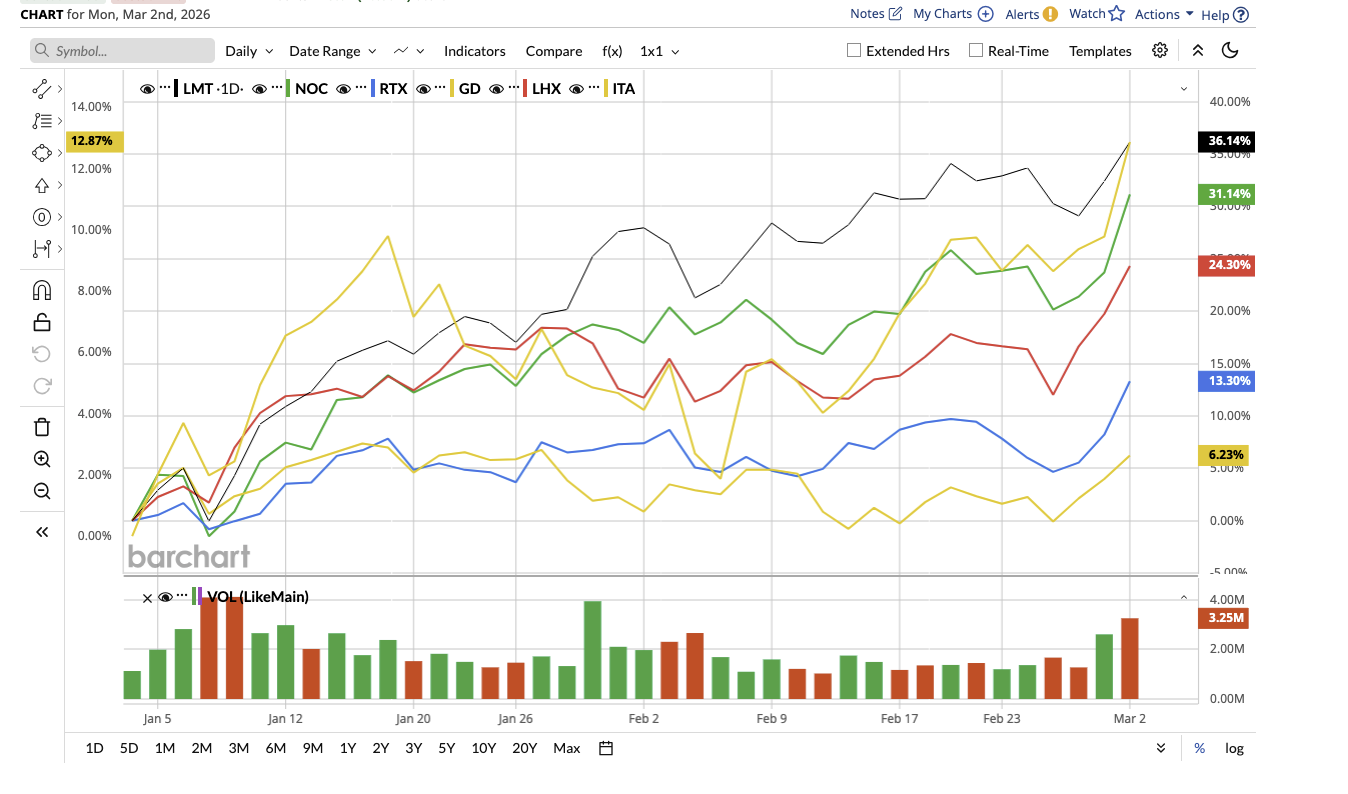

Let's explore five such defense stocks, most of which have outperformed the overall market and the iShares U.S. Aerospace & Defense ETF (ITA) gain of 12% so far this year.

Defense Stock #1: Lockheed Martin (Strategic Jet & Missile Defense Exposure)

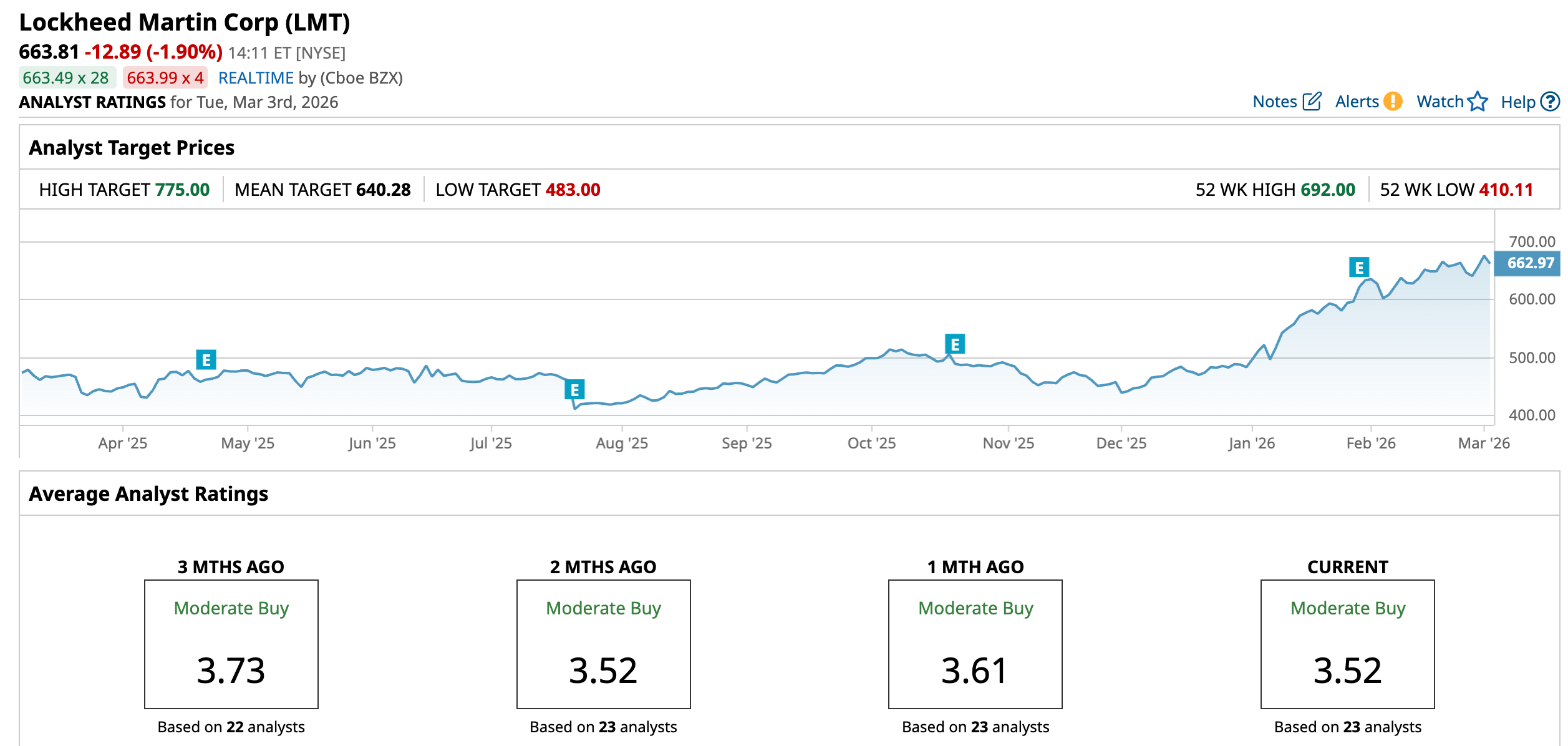

Valued at $155.7 billion, Lockheed Martin (LMT) is a prime U.S. aerospace and defense contractor that manufactures fighter jets (F-35), missiles, ISR systems, and space systems. Lockheed reported solid 2025 results, including a 6% year-over-year (YOY) sales increase, a high free-cash-flow balance of $6.9 billion, and a record backlog of $194 billion, which reflects multi-year contracted work. That backlog improves revenue visibility, cash generation, and shareholder returns.

Management expects continued momentum in 2026, guiding for sales between $77.5 billion and $80 billion, diluted earnings per share of $29.35 to $30.25, and free cash flow of $6.5 billion to $6.8 billion. Lockheed’s portfolio sees near-term demand increases in wartime procurement and allied modernization.

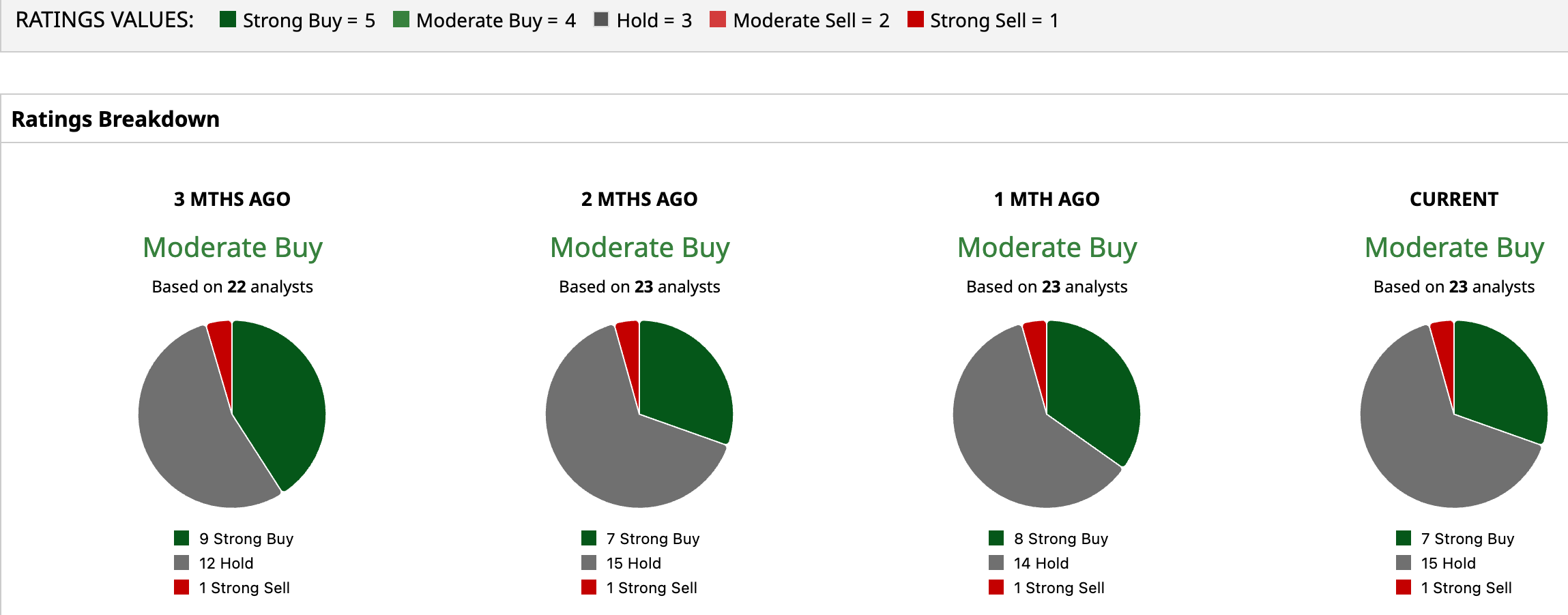

Overall, LMT stock remains a “Moderate Buy” on Wall Street. Of the 23 analysts that cover the stock, seven rate it a “Strong Buy,” 15 rate it a “Hold,” and one says it is a “Strong Sell.” Given its rally of 37% so far this year, LMT has surpassed its average analyst target price of $640.28. However, the Street-high estimate of $775 implies the stock can rally as much as 16.8% over the next 12 months.

Defense Stock #2: Northrop Grumman (Stealth, Space & Strategic Systems)

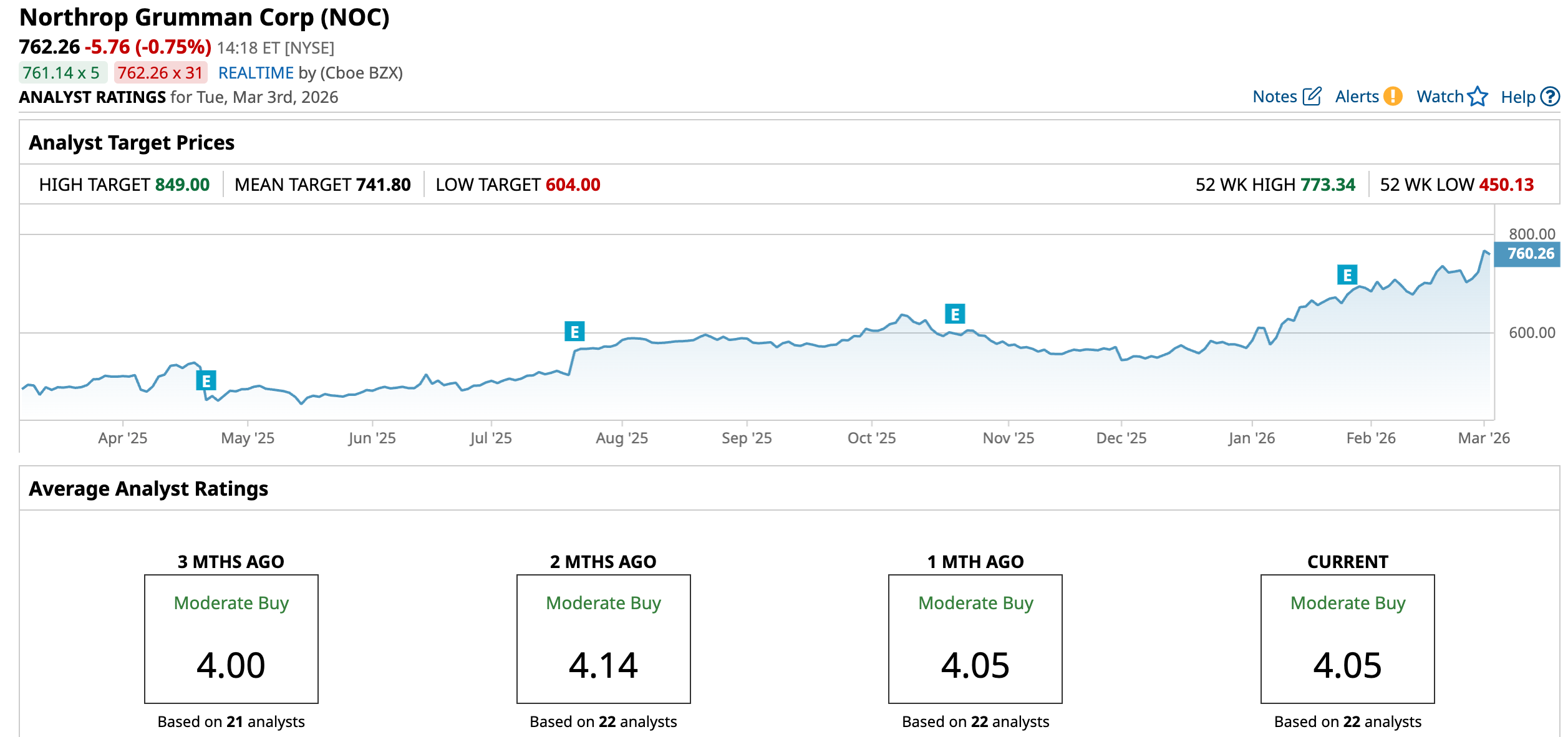

Valued at $109 billion, Northrop Grumman (NOC) is a major U.S. aerospace and defense contractor that builds stealth aircraft, missile defense systems, and space technologies for the U.S. government and its allies.

In 2025, Northrop reported a massive backlog of nearly $96 billion supported by a full-year book-to-bill ratio of 1.10, meaning it received 10% more in new orders than it recognized as revenue (billed) during the year. Major awards during the year included restricted programs, F-35 contracts, missile systems, and submarine-related work, indicating that long-term demand is intact. Full year revenue reached $42 billion with adjusted earnings per share of $29.08. It also generated $3.3 billion in free cash flow. Northrop’s B-21/stealth programs, missile-defense work, and space architecture efforts are all heavily reliant on increasing defense spending and alliance upgrades, which could dramatically boost revenues and margins if procurement accelerates.

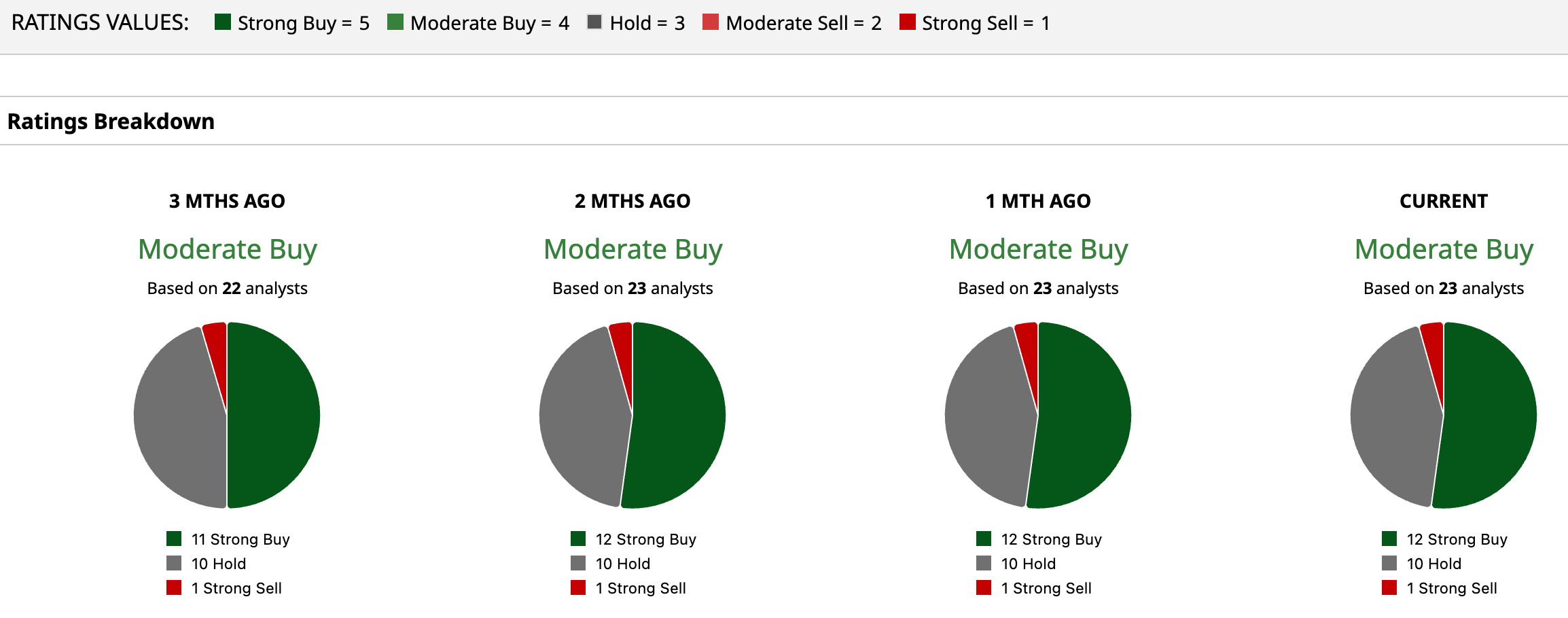

Overall, NOC stock remains a “Moderate Buy” on Wall Street. Of the 22 analysts that cover the stock, 11 rate it a “Strong Buy,” one rates it a “Moderate Buy,” and 10 rate it a “Hold.” Given the NOC stock rally of 33.3% so far this year, the stock has surpassed its average analyst target price of $741.8. However, the Street-high estimate of $849 implies the stock can rally as much as 11.4% over the next 12 months.

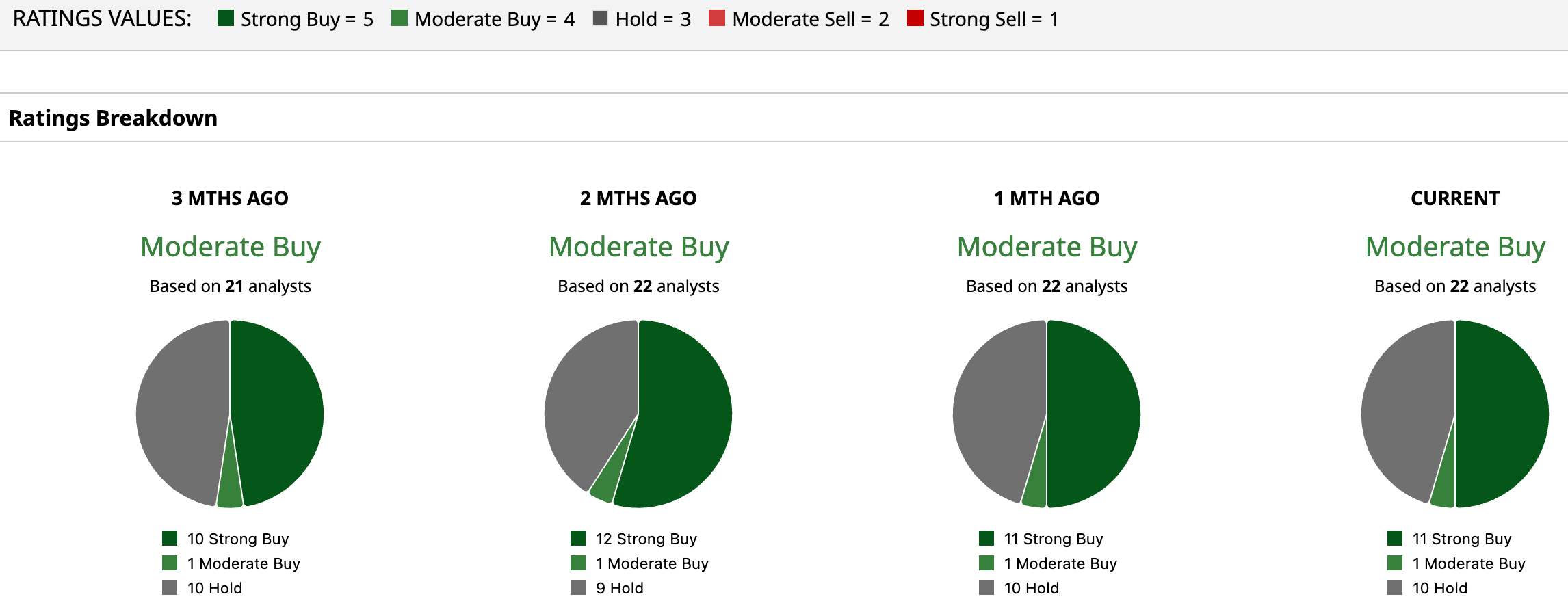

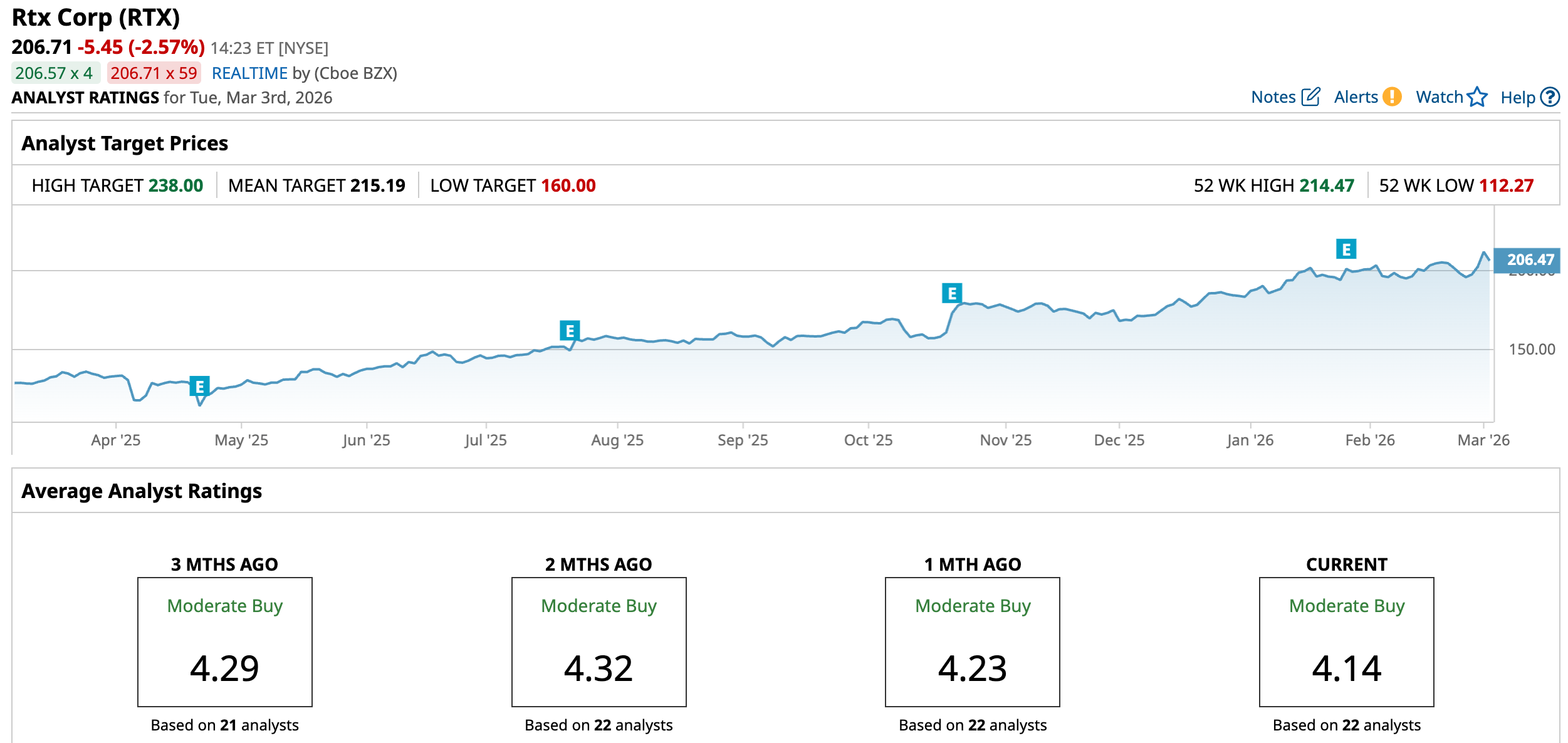

Defense Stock #3: RTX Corporation (Missiles, Engines & Integrated Defense Systems)

Valued at $284.8 billion, RTX Corporation (RTX) is a major U.S. aerospace and defense company.

- Through Pratt & Whitney, it manufactures jet engines for commercial and military aircraft.

- Through Raytheon, it produces missile systems, air defense systems (like Patriot), radars, and other advanced military technologies.

- Through Collins Aerospace, it makes avionics, flight controls, landing systems, interiors, and other aircraft components.

In 2025, RTX saw strong demand in both its commercial aerospace and defense businesses. Total sales increased 10% YOY to $88.6 billion, while adjusted earnings per share rose 10% to $6.29. It generated $7.9 billion in free cash flow and ended the year with a massive $268 billion backlog, including $107 billion tied to defense programs, providing strong revenue visibility. Management anticipates sustained growth in 2026, with sales ranging from $92 billion to $93 billion, adjusted EPS of $6.60 to $6.80, and free cash flow of $8.25 billion to $8.75 billion. Its exposure to both defense modernization and aerospace demand provides diverse revenue streams in growing war situations, lowering single-program risk.

Overall, RTX stock remains a “Moderate Buy” on Wall Street. Of the 22 analysts that cover the stock, 13 rate it a “Strong Buy,” one rates it a “Moderate Buy,” seven rate it a “Hold,” and one says it is a “Strong Sell.” RTX stock has gained 12.38% so far this year. The average analyst target price of $215.19 suggests the stock can climb by 4.1% from current levels. Plus, the Street-high estimate of $238 implies the stock can rally as much as 15.14% over the next 12 months.

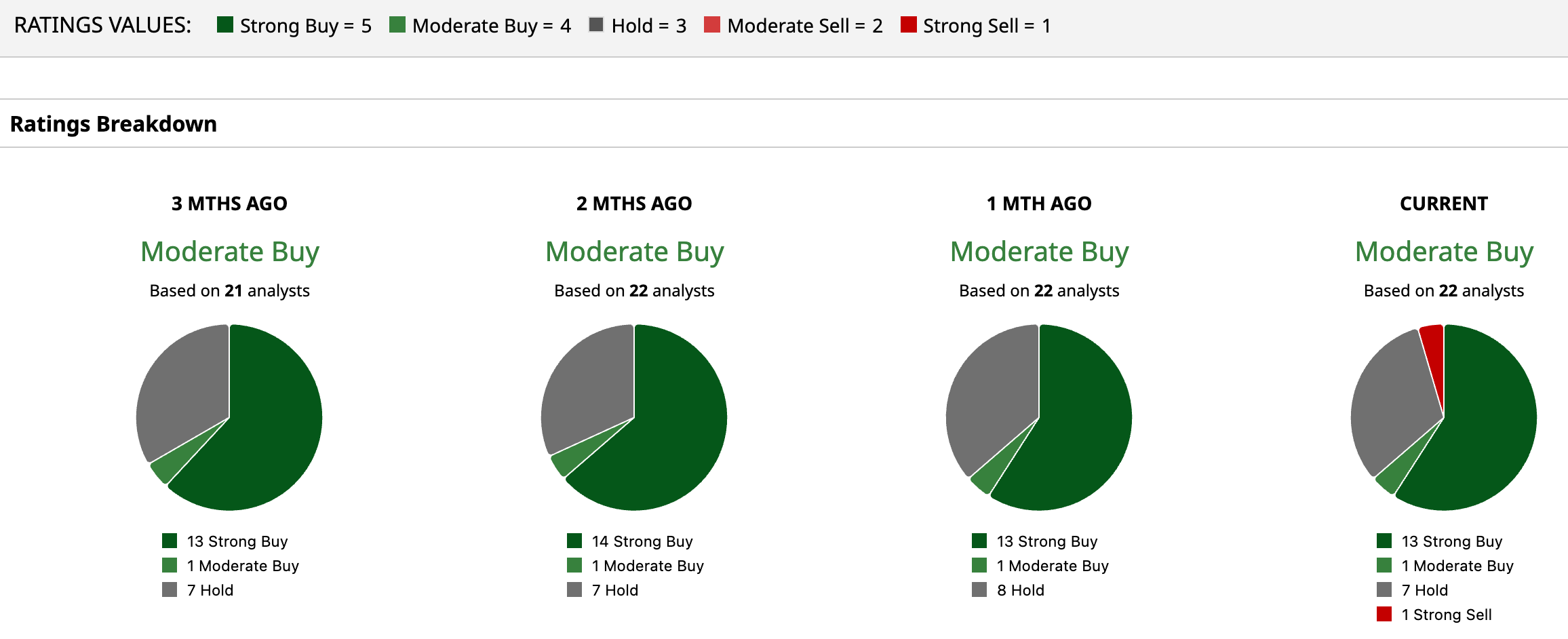

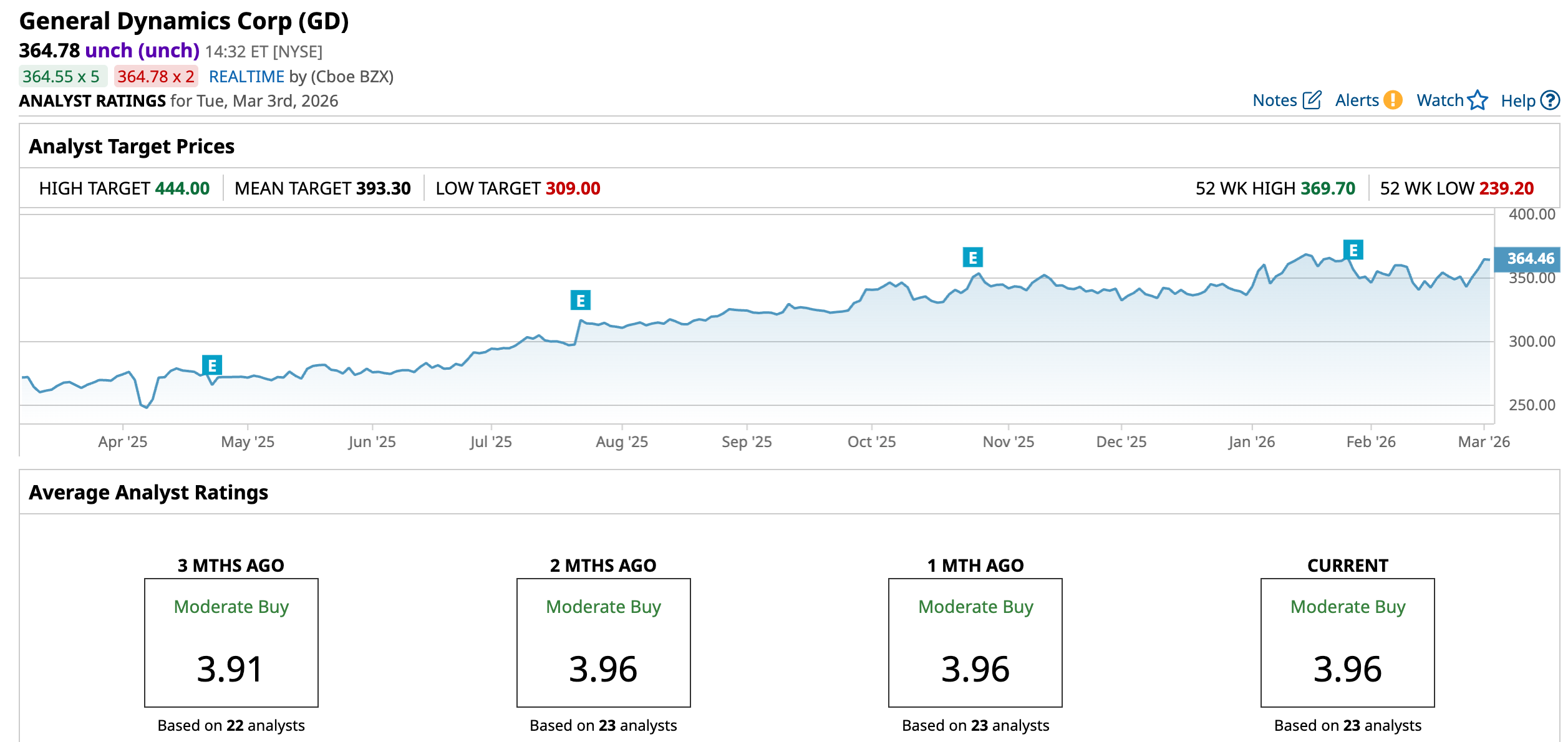

Defense Stock #4: General Dynamics: Marine Systems, Combat Vehicles & Tech Services

Valued at $98.6 billion, General Dynamics (GD) is a broad U.S. aerospace and defense company that builds submarines and other warships, high-end private jets, armored vehicles, and other land combat systems. It also offers secure communications, IT services, and cybersecurity solutions to governments.

General Dynamics reported full-year 2025 revenue of $52.6 billion, an increase of 10% from 2024 and net earnings growth of 11.3% with a large backlog of $118 billion and a book-to-bill ratio of 1.6x. It also generated $3.9 billion in free cash flow. Conflicts and escalation drive up demand for naval and land systems, particularly submarines, surface ships and armored vehicles, where GD has market-leading programs.

Overall, GD stock remains a “Moderate Buy” on Wall Street. Of the 23 analysts that cover the stock, 12 rate it a “Strong Buy,” 10 rate it a “Hold,” and one says it is a “Strong Sell.” GD stock has gained 8.25% so far this year. The average analyst target price of $393.30 suggests the stock can climb by 7.8% from current levels. Plus, the Street-high estimate of $444 implies the stock can rally as much as 21.7% over the next 12 months.

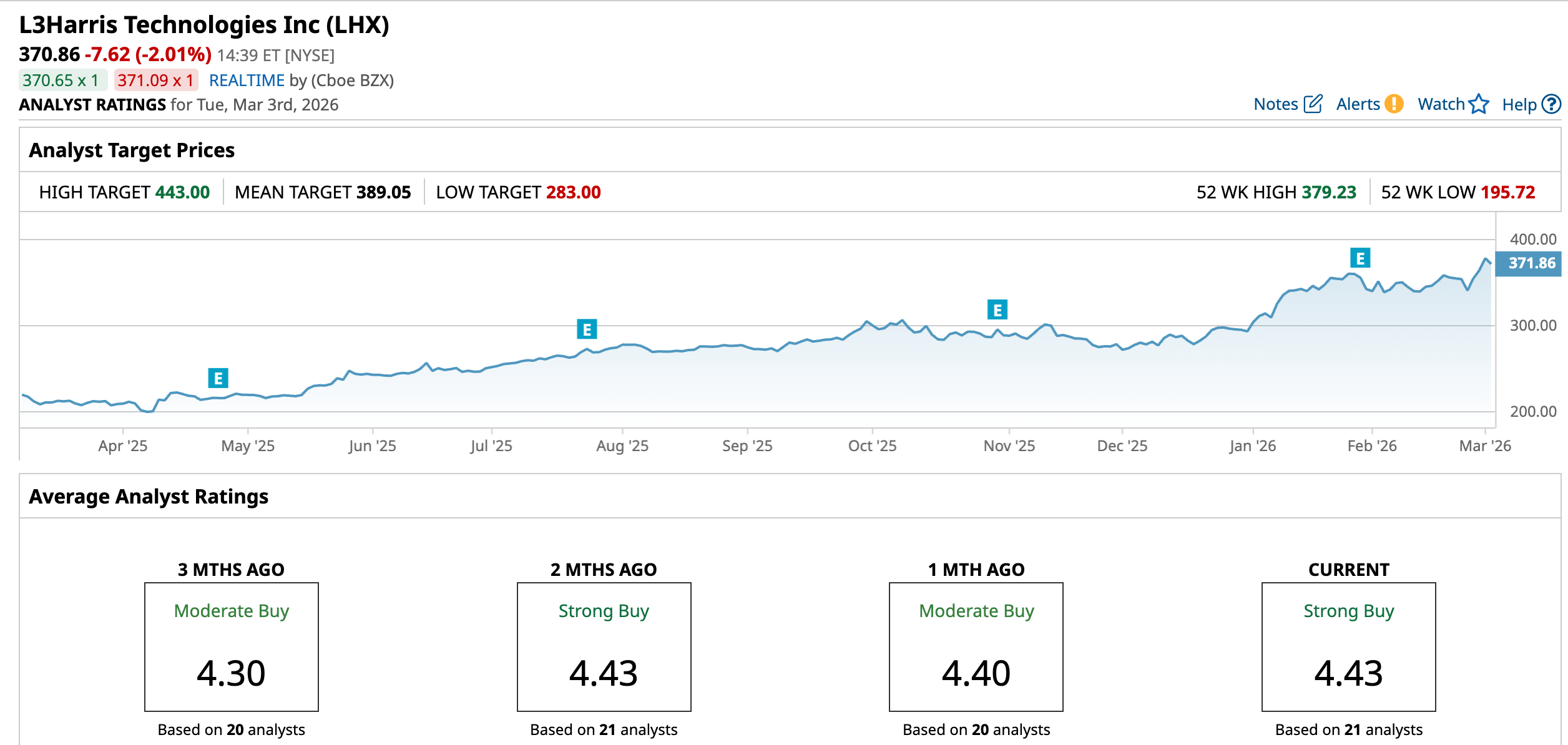

Defense Stock #5: L3Harris Technologies: Electronics, Sensors & ISR Systems

Valued at $70.7 billion, L3Harris Technologies (LHX) is a U.S. defense and aerospace company that offers communications, sensors, avionics, and ISR systems for defense, government, and commercial customers.

In 2025, L3Harris reported 2025 revenue of roughly $21.9 billion, a 5% organic increase YOY. Orders totaled $27.5 billion, with a healthy book-to-bill ratio of 1.3 times. Adjusted earnings increased 11% to $10.73. Improved cash from operations and adjusted free cash flow of $2.8 billion indicate consistent operational strength. Modern conflicts are driving demand for ISR, encrypted communications, and sensor fusion, areas where L3Harris has durable product franchises.

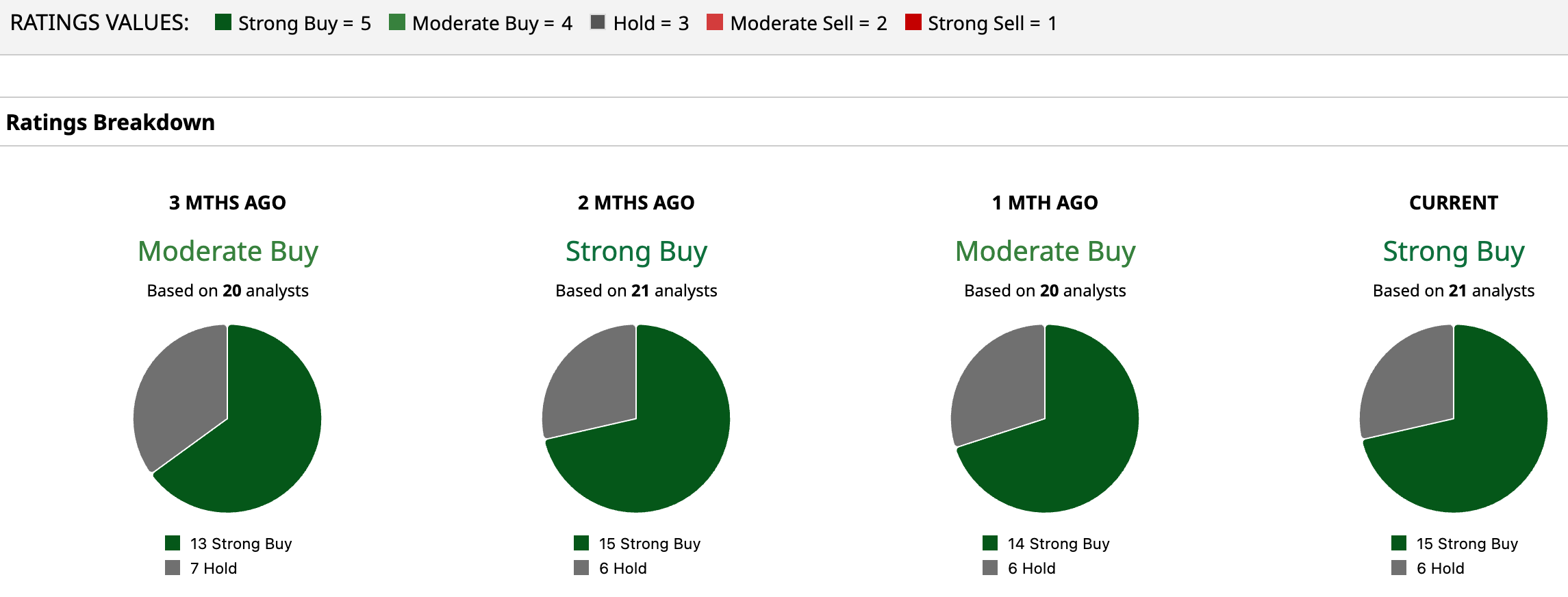

Overall, LHX stock remains a “Strong Buy” on Wall Street. Of the 21 analysts that cover the stock, 15 rate it a “Strong Buy,” and six rate it a “Hold.” LHX stock has soared 26.4% so far this year. The average analyst target price of $389.05 suggests the stock can rebound and climb by 4.9% from current levels. Plus, the Street-high estimate of $443 implies the stock can rally as much 19.45% over the next 12 months.

The Bottom Line

Defense stocks, while an intriguing investment now, also come with concerns such as budget volatility, program cost overruns, and protracted multi-year manufacturing cycles that can compress margins, among others. Hence, investors seeking diversified exposure to these defense stocks may consider the iShares U.S. Aerospace & Defense ETF, which holds many of these major defense contractors in one portfolio.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- MongoDB Stock Just Entered Oversold Territory. Should You Buy the Dip in MDB?

- Most Analysts Are Chasing Memory Stocks, But This 1 Wall Street Expert Thinks You Should Buy Apple Instead

- Dear Rigetti Computing Stock Fans, Mark Your Calendars for March 4

- Down 19% in 2026, Should You Buy the Dip in Qualcomm Stock?