While Nvidia (NVDA) gets the lion’s share of investors’ attention for the popularity of its advanced semiconductor chips, it would be a huge mistake to overlook Broadcom (AVGO). The chipmaker is carving out its own space in the market with specialty products that are cheaper than Nvidia’s chips.

With Broadcom’s earnings report coming up on March 4, what should investors expect from the chipmaker?

About Broadcom Stock

Based in San Jose, California, Broadcom is a leading semiconductor company whose products are used in data centers, telecommunication equipment, broadband, and more. The company has a market capitalization of nearly $1.5 trillion, ranking it in the top 10 in the world among publicly traded companies.

Broadcom’s chips are in high demand as high-performance semiconductors are needed to design, train, and run artificial intelligence platforms. Broadcom’s answer to this need is its custom ASIC chips, or application-specific integrated circuits, designed to handle the specific workloads of its clients. That means that the chips are less flexible than Nvidia’s general-purpose graphics processing units. Still, it also makes Broadcom’s chips cheaper—an important consideration as companies are spending billions on AI infrastructure.

Broadcom currently has a $10 billion deal to supply Anthropic with custom chips, and it’s working with Alphabet (GOOG) (GOOGL) to create that company’s Tensor Processing Units (TPUs) that Google is using as an alternative to Nvidia GPUs.

AVGO stock is up 65% in the last 12 months, handily beating the performance of the S&P 500 ($SPX) (up 15%) and Nvidia (up 56%). However, Broadcom's stock comes at somewhat of a premium, with a forward price-to-earnings ratio of 30.4 versus Nvidia’s 21.8. The stock also pays a dividend yield of 0.8%—not huge, but a pleasant bonus for a tech stock.

A Look at Broadcom’s Most Recent Earnings

Broadcom had a solid earnings report for the fourth quarter of fiscal 2025 (ending Nov. 2). Revenue of $18 billion was up 28% from a year ago, and net income of $8.51 billion was up 97%. Broadcom reported adjusted earnings per share of $1.95, which beat analysts’ estimates of $1.86.

"In Q4, record revenue of $18.0 billion grew 28% year-over-year, driven primarily by AI semiconductor revenue increasing 74% year-over-year," CEO Hock Tan said. “We see the momentum continuing in Q1 and expect AI semiconductor revenue to double year-over-year to $8.2 billion, driven by custom AI accelerators and Ethernet AI switches.”

Management issued guidance for revenue to be about $19.1 billion. But analysts will also be looking for more information about additional sales for Broadcom’s custom chips. Broadcom had said in June that it had three customers for its custom AI chips and four prospects. In December, it acknowledged Anthropic as the fourth client and said it signed a deal with a fifth, unknown client.

Any indication from Broadcom when it reports earnings on Wednesday that it’s continuing to sign new deals would potentially have an immediate impact on the stock price. But lack of such news would likely be seen as an indication that Broadcom is falling further behind Nvidia.

The consensus estimate calls for earnings of $1.67 per share, versus $1.40 per share in Q1 2025.

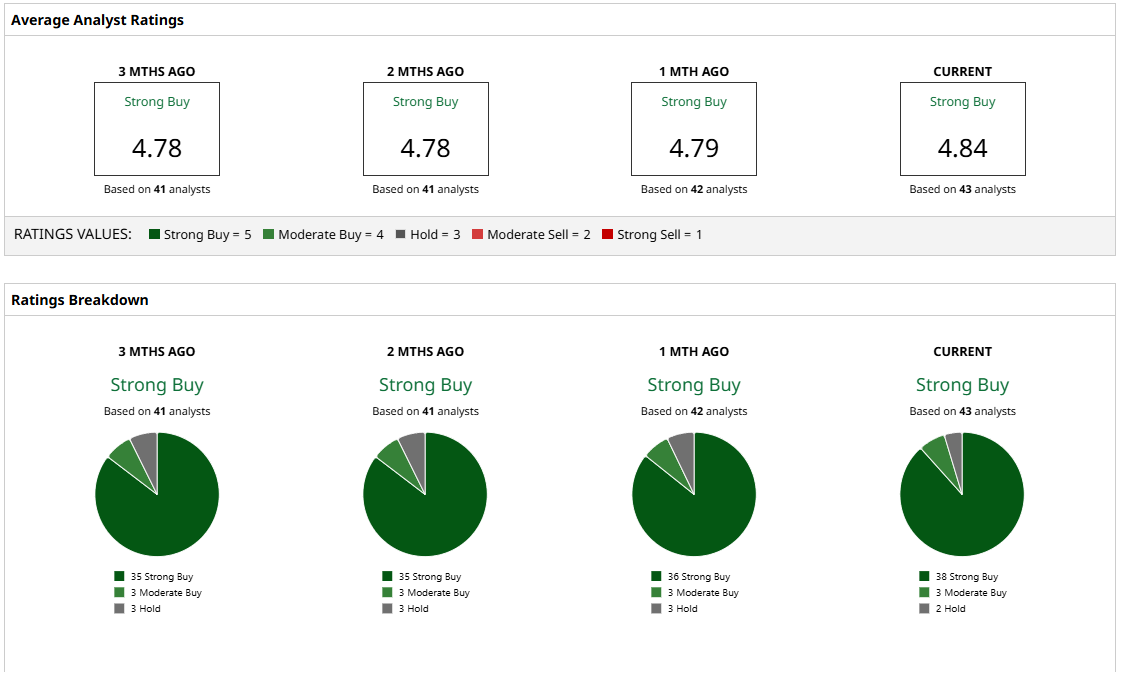

What Do Analysts Expect for AVGO Stock?

A notable thing about Broadcom is that analysts are nearly unanimous in their support for the stock. Of 43 analysts who cover AVGO stock, 41 of them have “Buy” ratings, and the other two have “Hold” ratings. The mean price target of $449 shows that experts project a 44% gain in AVGO stock, with a high target of $535 suggesting a 71% gain. Even the low target of $335 forecasts a modest gain from today’s stock price.

There’s never a sure thing in the stock market, but it’s also difficult to ignore the tailwinds for Nvidia, Broadcom, and other top chipmakers. Amazon (AMZN), Meta Platforms (META), Microsoft (MSFT), and Alphabet are collectively projected to spend as much as $700 billion on AI infrastructure, and a large percentage of that will go to the chips.

I’ll be watching Wednesday’s earnings to see what Broadcom says about its growing client base, but the stock appears to be a strong buy right now.

On the date of publication, Patrick Sanders had a position in: NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Is IonQ Stock the Tesla of Quantum Computing?

- Micron Technology Short-Put Plays Have Huge Yields - Attractive to Value Investors

- Sandisk Stock Hype Could ‘Vanish in a Single Earnings Call’ According to Citron Research. Is It Time to Ditch SNDK Here?

- Up 183% Over the Past Year, Does Teradyne Stock Have More Room to Run?