It is certainly not a good time to be a software company, even if you respond to the name Okta (OKTA). As the “Sasscopalypse” rages on and software stocks continue to receive a beating, the cloud-native identity security company is all set to report its results for Q4 2025 on Wednesday, after the market closes.

About Okta

Founded in 2009 by two ex-Salesforce (CRM) employees, Okta's core business is identity and access management (IAM) software delivered via the cloud. The company’s platform includes single sign-on (SSO), multi-factor authentication (MFA), API access management, Universal Directory, lifecycle management, identity governance, privileged access management, and other security tools that help organizations authenticate and secure human and non-human identities across hybrid IT environments.

Valued at a market cap of $12.8 billion, OKTA is down 18.6% in 2026 and 19.3% over the past year.

However, a closer look at the company will reveal that such a prolonged downturn is certainly not warranted.

Outstanding Q3 for Okta

Okta's results for Q3 2026 shone like a star, with both revenue and earnings beating estimates and key operational metrics seeing marked growth when compared to the year before.

Total revenues grew by 11.6% from the previous year to $742 million, with the core segment of subscription witnessing a year-over-year (YoY) growth rate of 11.2% to $724 million. Earnings grew by an even sharper 22.4% in the same period to $0.82 per share, outpacing the consensus estimate of $0.76. Impressively, this was the ninth consecutive quarter of not only beating estimates but also yearly growth of earnings from the company.

Remaining performance obligations, a key indicator of demand, shot up by 17% yearly to $4.3 billion, while cRPO, which is the quantum of orders that must be fulfilled within 12 months, increased by 13% from the previous year to $2.3 billion. Thus, wider concerns around software stocks may be prevalent, but the demand for Okta's products and services remains robust.

Coming to cash flows, net cash flow from operating activities rose by 35% from the prior year to $626 million for the nine months ended Oct. 31, 2025. Overall, the company closed the quarter with a cash balance of $645 million, with no short-term debt on its books.

For Q4, Okta expects revenues to be in the range of $748 to $750 million, the midpoint of which would denote an annual rise of 9.8%. Meanwhile, earnings are expected to be in the range of $0.84 to $0.85 per share. At the midpoint, this would indicate a growth of 34.2%, higher than Q3 2025. Lastly, expectations for cRPO are between $2.445 billion and $2.450 billion, whose midpoint would denote a growth of 8.9% on a YoY basis.

However, like others in its industry, Okta trades at reasonable levels when compared to its peers. While its forward P/E and P/CF of 21.07 and 15.39 are actually lower than the sector medians of 22.01 and 16.99, respectively, its forward P/S of 4.42 is just above the sector median of 3.12.

AI Opportunity for Okta

Okta is looking to be a formidable force in the world of AI agents, and its strategic vision for growth has that written all over it.

Okta used its recent “Oktane” conference to lay out a forward-looking view on what it calls “agentic identity security.” The company argues that AI agents and non-human identities (NHI) are rapidly becoming the next major frontier in identity and access management. In essence, every AI application, autonomous agent, or automated workflow that touches a company’s systems needs its own identity, authentication, and tightly controlled permissions, exactly like a human employee or contractor. As organizations roll out more AI assistants, bots, and background processes, managing these non-human actors securely is turning into an urgent priority. Okta sees this as a natural extension of its identity security business.

To address the trend, Okta introduced two new offerings. While Auth0 for AI agents is aimed at developers embedding AI into customer-facing applications, Okta for AI agents targets IT and security teams responsible for internal AI tools and workflows. Both build directly on the company’s existing platform, allowing organizations to register, authenticate, and govern machine identities with the same rigor applied to human users. The move positions Okta to capture demand as AI adoption accelerates and companies look for consistent, scalable ways to control non-human access without creating new silos.

Notably, Okta’s competitive edge is built on its ability to integrate seamlessly across thousands of heterogeneous applications and multi-cloud environments, unlike hyperscalers such as Microsoft (MSFT). This platform-agnostic approach is increasingly valuable as enterprises move away from vendor lock-in. Furthermore, the company has successfully pivoted into the developer space through its Auth0 acquisition, creating a high-barrier-to-entry moat by securing not just the workforce but the customer-facing applications themselves. By offering a unified Identity Cloud, Okta reduces the complexity of managing fragmented digital identities, which typically results in superior customer retention and higher lifetime value compared to more specialized or rigid competitors.

However, the company faces a complex set of headwinds that keep investors cautious. The most immediate challenge is the persistent threat landscape; recent reports of sophisticated "vishing" (voice phishing) campaigns targeting SSO providers remind the market that identity platforms are the ultimate prize for hackers. While Okta’s core infrastructure has remained resilient, any perceived breach can lead to reputational friction and longer sales cycles. Furthermore, the competitive pressure from Microsoft Entra ID remains intense, particularly among cost-conscious enterprises that are already heavily invested in the Microsoft 365 ecosystem.

Analyst Opinion of OKTA Stock

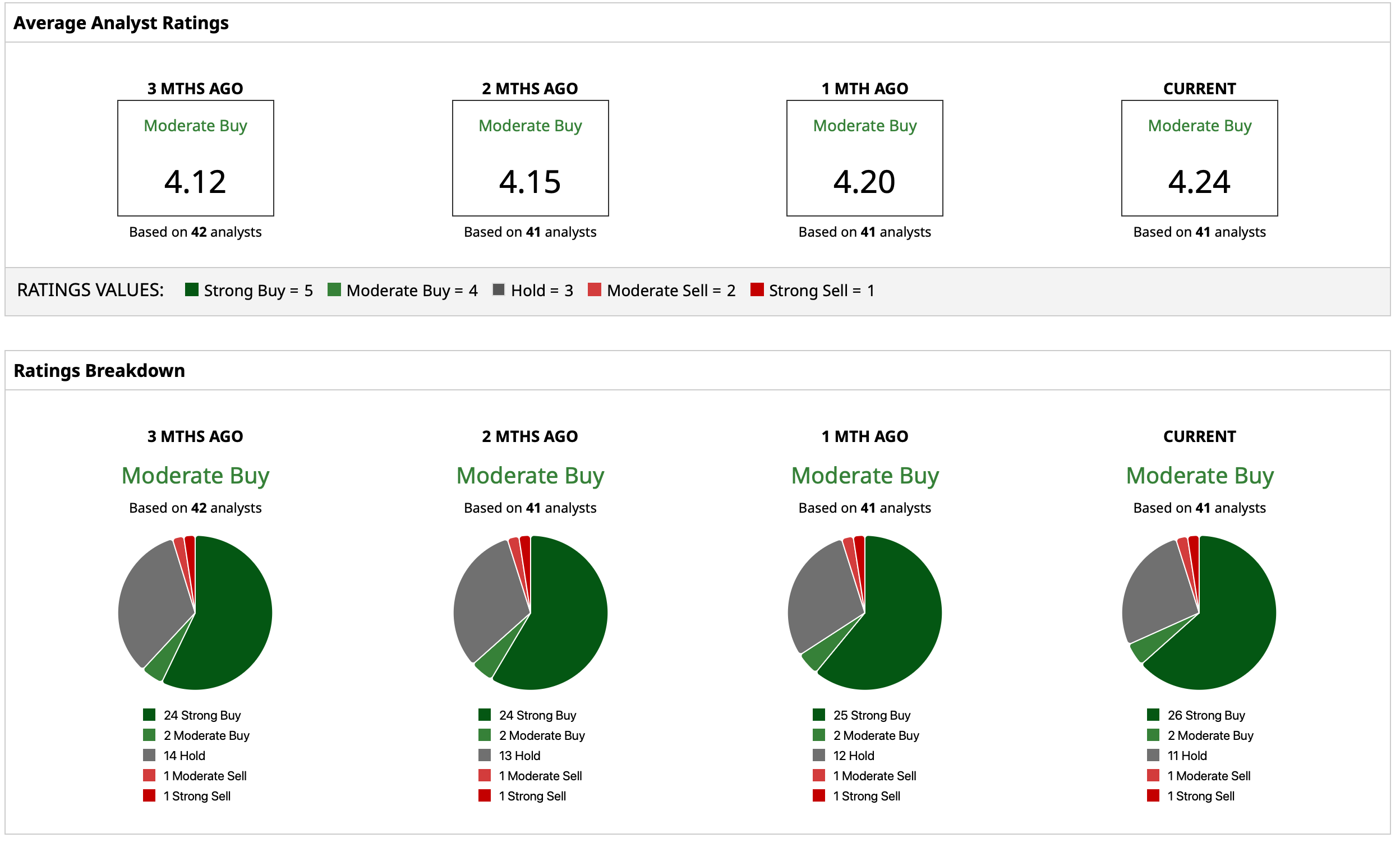

Overall, analysts remain cautiously optimistic about the OKTA stock, earmarking it a consensus rating of “Moderate Buy.” The mean target price of $107.94 indicates an upside potential of about 51% from current levels. Out of 41 analysts covering the stock, 26 have a “Strong Buy” rating, two have a “Moderate Buy” rating, 11 have a “Hold” rating, one has a “Moderate Sell” rating, and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart