I asked where gold was heading in 2026 in a January 6, 2026, Barchart article. I concluded with the following:

Many analysts who did not see gold’s 65.9% 2025 rally are now calling for prices to rise to $5,000 in 2026. Meanwhile, continued uncertainty in the economic and geopolitical landscapes could push prices much higher. I remain bullish on gold’s prospects for the coming year, but buying on pullbacks rather than on rallies has been optimal for over two and a half decades. I expect that trend to continue in 2026.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

Nearby COMEX gold futures traded at $4,456.40 per ounce on January 5, 2026, and the price rose over $1,000 per ounce by the end of January, before gravity brought the parabolic move to a halt.

The tenth consecutive quarterly high and a correction

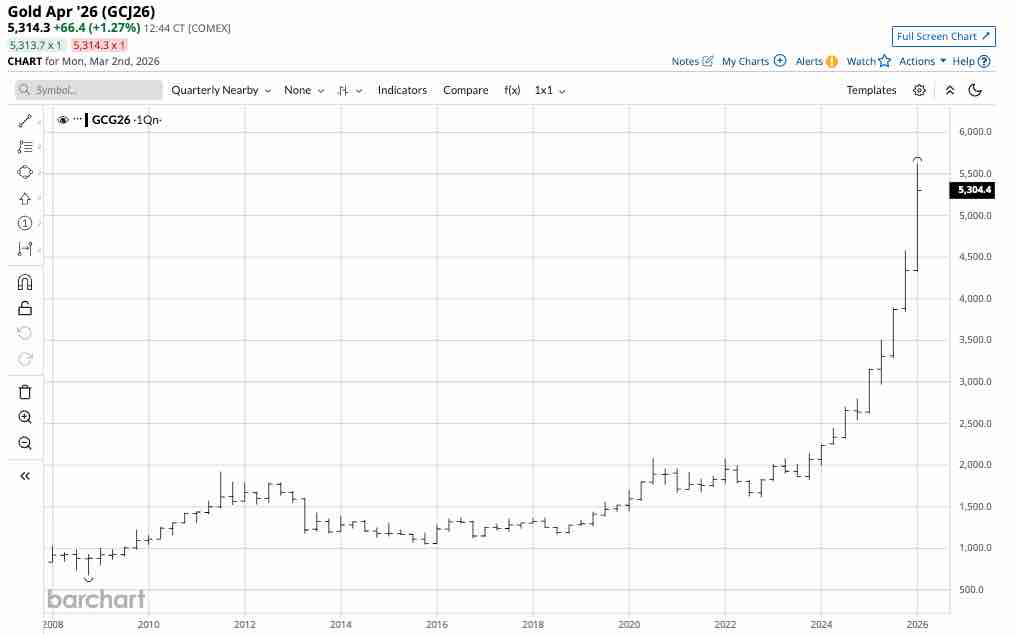

It did not take long for COMEX gold futures to reach their tenth consecutive quarterly record high in Q1 2026.

The quarterly continuous contract chart shows that COMEX gold futures rose 29.6% from the end of 2025, $4,341.10 closing level, to the Q1 high of $5,626.80 per ounce on January 29, 2026.

Gravity hit gold with a sledgehammer in late January and early February, sending the leading precious metal 21.9% lower to $4,423.20 per ounce on February 2. While gold’s price plunged by over 21%, it never reached the 2025 closing level and was back over $5,300 per ounce on March 2.

The case for higher highs

The compelling case for a continuation of gold’s bullish trend includes the following factors:

- Gold’s bullish trend began in 1999 at $252.50 per ounce, and was over 22 times higher at the most recent late January 2026 high.

- Central banks, governments, monetary authorities, and supranational institutions continue to purchase gold, adding to reserves and validating gold’s role in the global financial market.

- The deterioration in the purchasing power of the dollar and other fiat currencies has caused gold to appreciate.

- U.S. sanctions and tariffs support higher gold prices as countries seek to divest from the leading fiat reserve currency, the dollar.

- Falling U.S. interest rates are bullish for gold as they reduce the cost of carrying inventories.

- Geopolitical and economic uncertainty and turmoil are bullish for gold.

A caution about parabolic markets

The case for further downside corrections in gold prices includes:

- Even the most aggressive bull markets rarely move in straight lines. The correction from the high on January 29, 2026, to the low on February 2, 2026, is an example of the periodic corrections that can impact gold prices.

- While central banks have continued to purchase gold, there is no guarantee they will continue to add to their reserves if the price continues to rise.

- Commodity cyclicality suggests that prices can rise to levels that defy rational, reasonable, and logical prices that defy fundamental and technical analysis. However, prices often rise to unsustainable levels, triggering corrections.

Gold is not a typical commodity

Gold is a unique asset. The precious metal has many industrial and ornamental applications, but it is also the oldest form of money and a means of exchange with a history of thousands of years. Over the past year, gold surpassed the euro as the world’s second-leading reserve foreign exchange instrument.

The bottom line is that traditional technical and fundamental analysis may be meaningless for gold, as its value is determined by government and individual investment activity. While governments have increased their gold exposure, individual investors are likely underinvested in the leading precious metal.

Central banks are critical for gold’s price action over the coming months

While central banks steadily purchased gold, adding to their reserves, the official statistics are likely understated. China and Russia are leading gold-producing countries that have likely added their substantial domestic production to reserves to deflect the impact of U.S. sanctions and tariffs. Moreover, the 2022 “no-limits” alliance between Beijing and Moscow undermines the U.S. dollar’s role in the global financial market. Choosing gold over U.S. dollars and U.S. government debt securities as reserve assets reduces the U.S. dominance in the global economy.

Central bank purchases have supported gold’s appreciation. A continuation of higher highs likely depends on continued central bank gold accumulation.

Meanwhile, the trend in any market is always a trader’s or investor’s best friend, and it remains bullish in gold in early March 2026. Time will tell if gold prices eclipse the Q1 2026 high of $5,626.80 on the continuous COMEX futures contract from April through June to establish the eleventh consecutive quarterly record high. Given the powerful demand for gold and central bank buying, the odds favor higher highs over the coming months.

On the date of publication, Andrew Hecht did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart