SanDisk (SNDK) stock is the S&P 500's ($SPX) top-performing stock. Shares are up more than 147% year-to-date (YTD) and have surged by more than 1,000% in just six months. The artificial intelligence (AI) data center expansion has driven demand for memory products used in AI infrastructure, thereby supporting SNDK stock.

The rapid expansion of AI-focused data centers has significantly increased demand for NAND flash memory, a core component of SanDisk’s product portfolio. The company provides high-performance flash storage solutions designed to support AI workloads across hyperscale data centers, edge computing environments, and consumer applications. As enterprises scale AI capabilities, the need for reliable, high-capacity, and energy-efficient storage is rising, positioning SanDisk to benefit from these structural industry trends.

In addition to favorable demand dynamics, SanDisk is benefiting from supply-side constraints within the global memory market. With constrained availability, producers have been able to command higher prices, supporting margin expansion and improved profitability.

Recent financial results show that higher demand and pricing have enabled SanDisk to deliver record revenue and earnings. In the second quarter of fiscal 2026, SanDisk reported a 61% year-over-year (YoY) increase in net revenue. The growth was driven primarily by a 36% rise in average selling prices per gigabyte and a 22% increase in exabytes sold, reflecting stronger demand for the company’s data storage products. The combination of higher pricing and increased shipment volumes has translated into a substantial earnings uplift. It delivered adjusted earnings of $6.20 per share in Q2, up about 408% YoY.

However, after such a steep climb, should investors cash out or hold on to SNDK stock for further gains?

SanDisk’s Growth Unlikely to Slow Down Anytime Soon

While SanDisk has delivered significant growth, the momentum in its business is unlikely to slow down anytime soon. A major catalyst is the planned increase in capital expenditure by hyperscalers, who are investing heavily in AI infrastructure.

As hyperscalers continue expanding AI-focused data center capacity, demand for high-performance storage is rising in tandem. AI workloads, especially inference at scale, require significantly higher NAND density per deployment. That dynamic directly benefits SanDisk’s enterprise solid-state drive (SSD) portfolio, where demand is accelerating across the broader data center ecosystem.

For SanDisk, this shift is not limited to a handful of customers. Adoption is expanding across enterprise data centers, edge infrastructure operators, OEMs, and system integrators building AI-ready systems. This diversification strengthens revenue visibility and reduces concentration risk. Management expects the data center segment to deliver meaningful growth going forward, reflecting structural demand trends.

At the edge, the supply-demand imbalance has been even more pronounced. Replacement cycles in PCs and mobile devices, combined with AI-enabled features requiring higher storage density, are pushing device configurations toward richer, higher-capacity builds. Demand has meaningfully exceeded supply in Q2, allowing SanDisk to benefit from both volume expansion and favorable pricing dynamics. In consumer markets, the mix has shifted toward premium products and higher-value configurations, supporting margin expansion alongside revenue growth.

Looking ahead, SanDisk projects customer demand to remain well above available supply through at least calendar year 2026. Such a sustained imbalance will create favorable pricing conditions and operating leverage for SanDisk, positioning it to deliver substantial revenue and earnings growth in fiscal 2026 and 2027.

For the upcoming third quarter, the company guides revenue between $4.4 billion and $4.8 billion, implying sequential growth of 45% to 58%. That represents a sharp acceleration relative to prior quarters. Profitability expectations are high. Adjusted gross margin is projected in the 65% to 67% range, substantially above both the prior quarter and year-ago levels. Adjusted EPS is projected between $12 and $14, with the midpoint suggesting earnings could more than double on a sequential basis.

Profit expectations for the third quarter support the bullish outlook for SNDK stock. SanDisk forecasts an adjusted gross margin of 65% to 67%, a significant increase from Q2 levels and well above the margin recorded a year ago. Adjusted EPS is projected between $12 and $14, with the midpoint implying that earnings could more than double sequentially.

SNDK Stock: Cash Out or Keep Holding for Gains

A solid demand environment, a broadening customer base, sustained supply tightness, and an accelerating margin profile indicate that SanDisk is well-positioned to deliver significant gains in the coming years.

From a valuation standpoint, SNDK stock does not appear stretched despite its recent rally. SNDK trades at a forward price-to-earnings ratio of 27.7, a multiple that looks reasonable given its projected earnings growth. Analysts anticipate an extraordinary surge of 1,189.9% in EPS in fiscal 2026, followed by another year of strong expansion in fiscal 2027. The strong profitability helps justify the current valuation and leaves room for expansion.

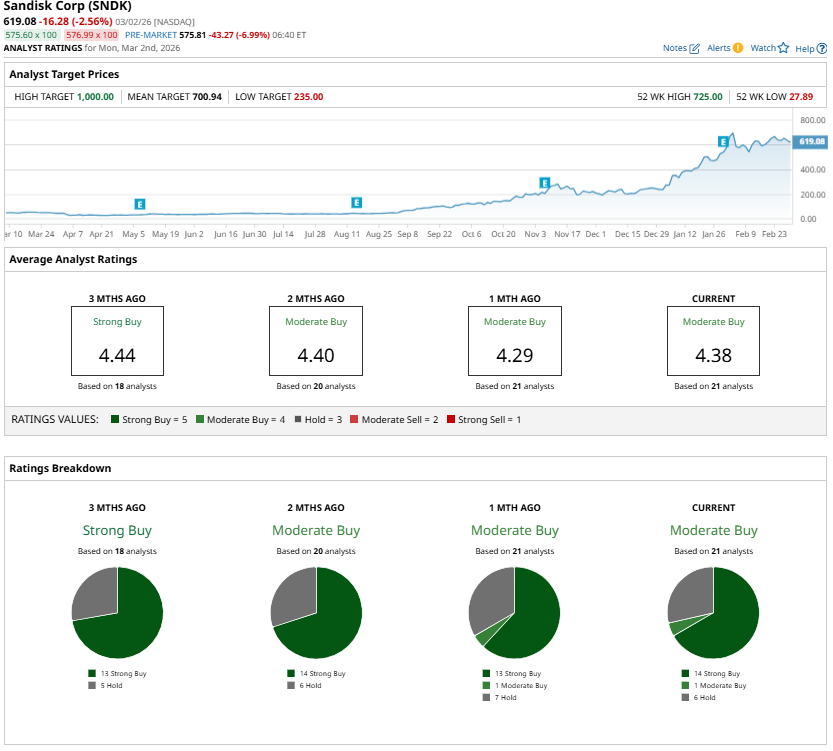

That said, not all analysts are endorsing SNDK stock after a solid rally. The consensus rating is “Moderate Buy,” reflecting some caution around the cyclical nature of the memory market and macro uncertainty.

However, as NAND demand remains strong and pricing momentum continues, SanDisk appears well-positioned to sustain its growth trajectory, suggesting further upside in SNDK stock.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart