Sandisk (SNDK) has been one of the most explosive momentum names, rising by 145% year-to-date (YTD) and an astonishing 1,050% over the past year. However, the rally is now being put to the test by the high-profile short call by Citron Research. The firm argues the NAND flash cycle can turn quickly, which could reverse the trend.

Citron Research argues the following:

“Memory is cyclical, not structural. While the rise of artificial intelligence and hyperscaler demand has driven pricing and margins higher, the historical record is clear: supply eventually catches up. And with Samsung now signaling its commitment to maintaining premium margins, the risk is that the industry becomes even more competitive than investors expect sooner rather than later.”

About Sandisk Stock

Sandisk Corporation is one of the leading providers of NAND flash memory and storage solutions. The company serves the data center, edge, and consumer markets. It is based in California and was spun out of Western Digital (WDC). The company has a current market capitalization of approximately $93.8 billion.

The stock has traded between $27.89 and $725 over the past year. This demonstrates the extreme volatility of the stock. The current price is approximately $590, which is substantially higher than the broader S&P 500 Index ($SPX).

The stock is trading at high valuations. The current price is 103.31 times earnings and 27.67 times forward earnings. The price/sales ratio is 12.75, and the price/book ratio is 9.18. These valuations are high and demonstrate investors are betting on peak margins. However, the forward earnings multiple is reasonable and demonstrates investors expect earnings to grow rapidly.

The company does not have a dividend.

Sandisk Beats on Earnings

Sandisk reported a spectacular turnaround in its fiscal second quarter, which ended on Jan. 2, 2026. In the latest quarter, the company reported revenue that increased by 61% compared to the same period last year, amounting to $3.025 billion. At the same time, the non-GAAP diluted EPS increased substantially from $1.23 last year to $6.20 this year.

Non-GAAP gross margins also increased substantially, rising to 51.1% compared to 32.5% last year. The company also reported a strong increase in data center revenue, which increased by 64% sequentially and came in at $440 million due to increased demand for infrastructure products. In addition, the edge and consumer segment also reported a strong increase.

Further, the guidance also helped investors become more positive regarding the stock, as the company has projected revenue for the third quarter between $4.4 billion and $4.8 billion, along with non-GAAP EPS between $12 and $14. In addition, the gross margins are also expected to increase further, with the gross margins expected to be between 65% and 67%. This has also been the main point of contention for Citron, which has stated that the NAND shortage can reverse quickly, and with Samsung also re-entering the premium SSD market, the prices could be impacted, which could compress the EPS just as easily as it expanded.

The company has yet to announce the date for the next earnings announcement.

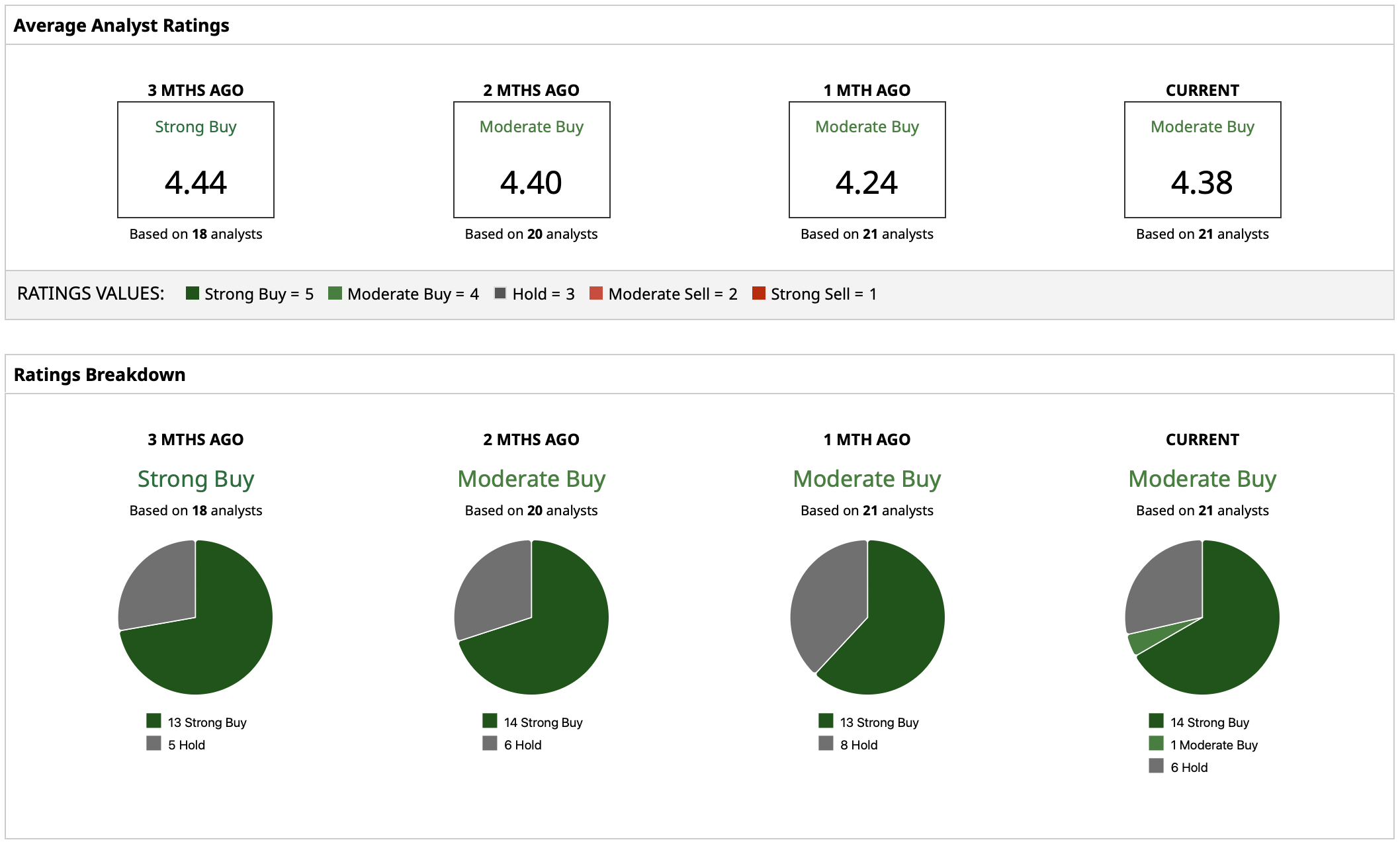

What Do Analysts Expect for SNDK Stock?

Wall Street analysts are positive regarding the stock, with the stock having a “Moderate Buy” rating consensus and a target price of $700.94, with a high target price of $1,000 and a low target price of $235. At current stock prices of around $590, the mean target of $700.94 implies an upside potential of roughly 19%. However, the large range of high and low targets reflects the significant degree of uncertainty regarding normalized earnings.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart