Cybersecurity spending continues to surge despite shifting dynamics in the artificial intelligence (AI) landscape, and Rubrik (RBRK) is emerging as a standout name in the space. Recent channel checks from Wedbush Securities suggest the company is receiving some of the strongest vendor feedback as enterprises deepen investments in cyber resilience and data protection.

Analysts led by Dan Ives highlighted that enterprise IT budgets are expanding meaningfully, supported by rising allocations for AI. Enterprise budgets rose about 20% at the start of the year, with AI spending increasing another 20%, producing roughly a 33% overall rise in technology and AI-related spending across organizations.

Deal dynamics are also shifting across the cybersecurity sector. Around 80% of deals in the current pipelines are being revised upward. Competition and disruption also remain part of the landscape. New cyber-AI tools from Anthropic and innovations such as Claude Cowork are influencing the market.

Notably, sales cycles have stretched to about 109 days as buyers demand more proof-of-concept testing. Yet despite longer negotiations, analysts report no deals being lost, with Rubrik among vendors receiving particularly solid demand signals.

Against this evolving backdrop, let’s delve deeper to better understand what stance investors might consider taking on the stock.

About Rubrik Stock

Based in Palo Alto, California, Rubrik provides data security and cyber-resilience solutions to enterprises worldwide. Its platform safeguards enterprise, cloud, SaaS, and unstructured data while offering threat analytics, security posture management, and cyber-recovery capabilities for organizations across various industries.

Valued at roughly $11 billion, the company operates in a rapidly expanding cybersecurity market but has faced notable stock volatility recently. Over the past 52 weeks, Rubrik’s shares have declined 10.8%. The weakness has intensified in 2026, with the stock down 26.7% year-to-date (YTD) and falling 35% over the past three months.

From a valuation standpoint, the stock still trades at a premium relative to many cybersecurity peers. Shares are currently priced at about 8.57 times sales, reflecting investor expectations tied to the company’s growth potential and expanding role in AI-driven cybersecurity solutions.

A Closer Look at Rubrik’s Q3 Earnings

Rubrik delivered a solid operational update when it unveiled its Q3 fiscal year 2026 results on Dec. 4, 2025, highlighting improving profitability and steady demand for its data-security platform. Total revenue rose 48.3% year-over-year (YOY) to $350.2 million, surpassing analyst expectations by 9.11%.

The company posted non-GAAP net income of $22.9 million, marking a turnaround from a non-GAAP net loss of $37.8 million in the prior-year period. Meanwhile, non-GAAP earnings per share came in at $0.10, a notable improvement from a non-GAAP loss of $0.21 per share reported in the same period last year.

The quarter also reflected strong operational momentum, with subscription annual recurring revenue (ARR) rising 34% YOY and free cash flow exceeding $76 million. Encouraged by the results, management has raised its outlook for fiscal 2026.

For the full fiscal year, Rubrik expects subscription ARR between $1.439 billion and $1.443 billion, with revenue projected in the range of $1.280 billion to $1.282 billion. Additionally, the company anticipates a non-GAAP net loss per share of $0.20 to $0.16 for the year.

For the fiscal fourth quarter of 2026, management forecasts revenue between $341 million and $343 million, alongside a non-GAAP subscription ARR contribution margin of about 9%. The company expects the non-GAAP net loss per share to range from $0.12 to $0.10 for the quarter.

Rubrik is scheduled to report its fiscal Q4 2026 results after the market closes on Thursday, March 12. Analysts expect the quarterly loss per share to narrow 13.1% YOY to $0.53. For the full fiscal year 2026, the company’s loss per share is projected to shrink 75.5% to $1.83, with another 10.4% improvement anticipated in the following fiscal year to $1.64.

What Do Analysts Expect for Rubrik Stock?

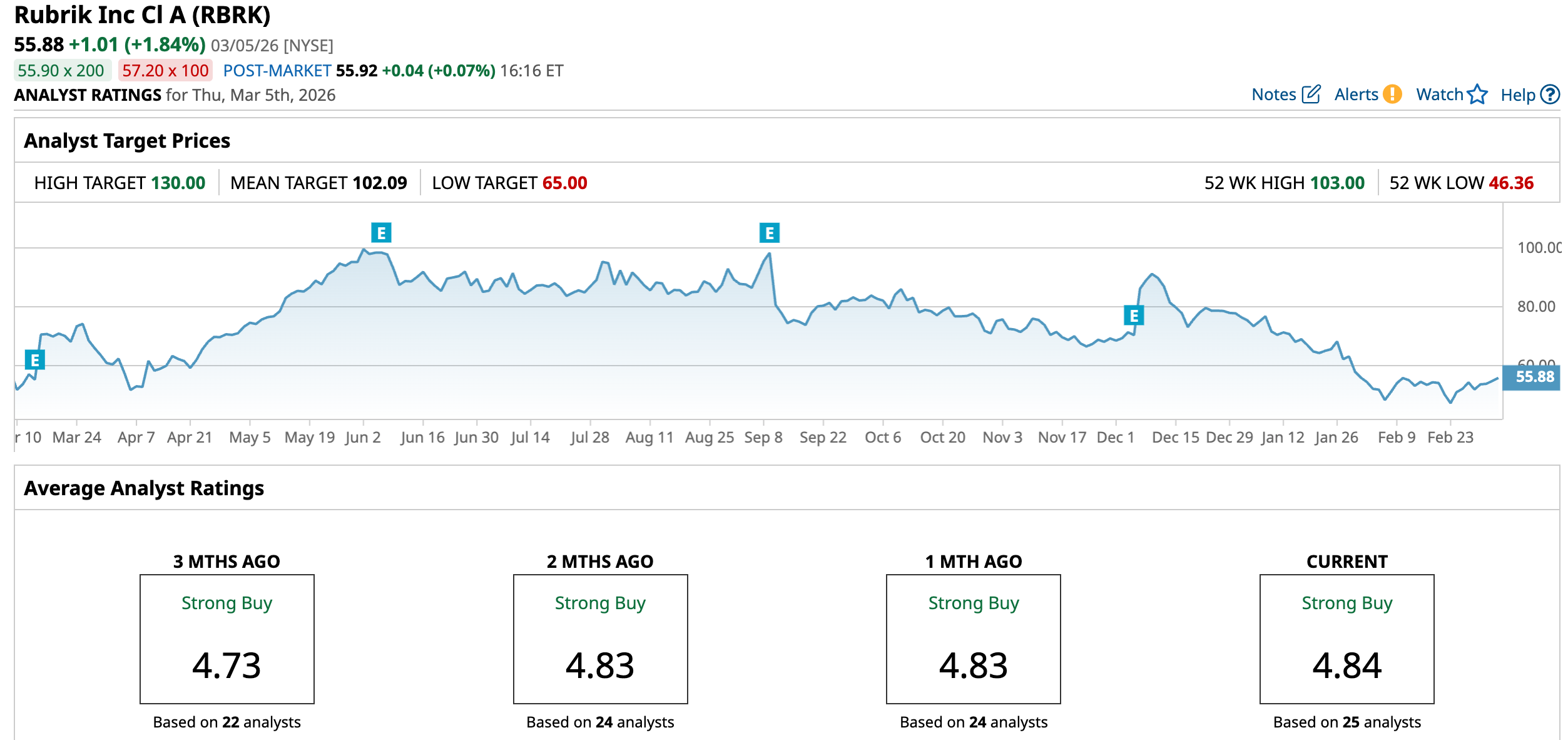

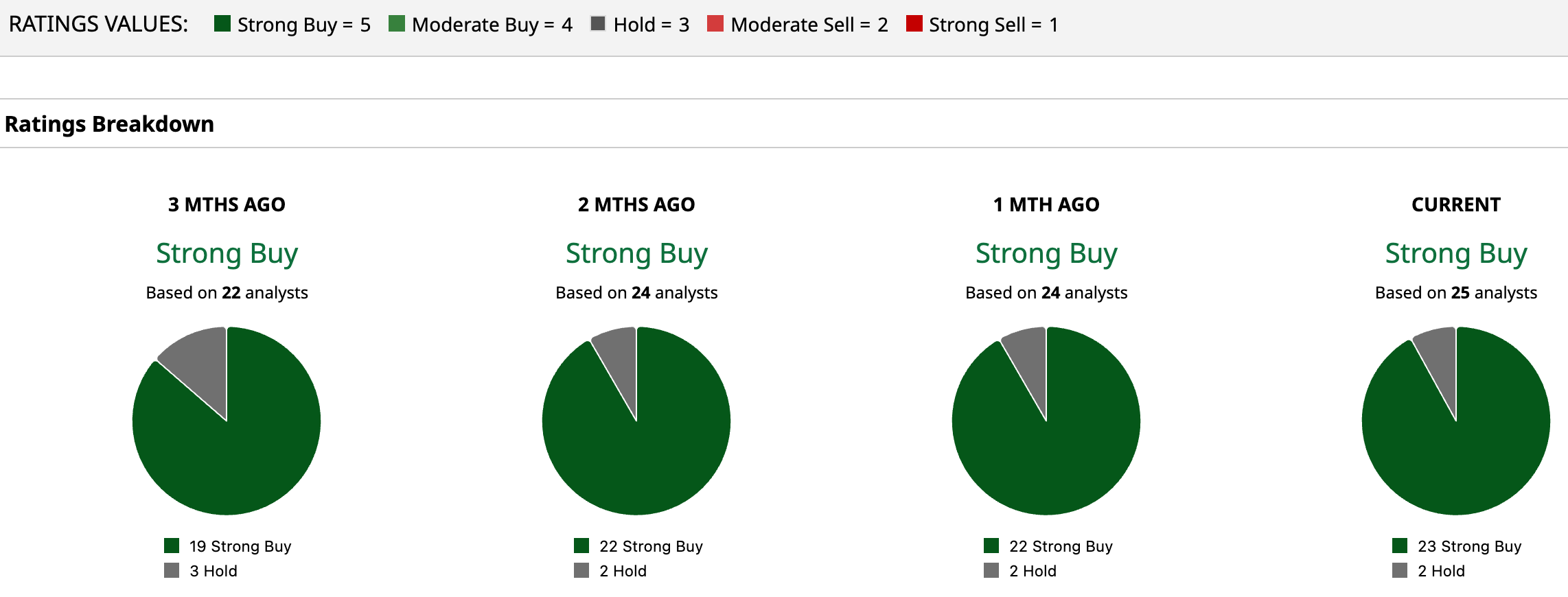

Rubrik currently holds a “Strong Buy” consensus rating on Wall Street, reflecting positive sentiment around the company’s long-term growth prospects. Of the 25 analysts covering the stock, 23 recommend a “Strong Buy,” while two maintain a “Hold.”

Based on current projections, the average price target of $102.09 implies potential upside of 82.7%. Meanwhile, the Street-high target of $130 suggests the shares could rally as much as 132.6% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- SoundHound Is One of the Most Short Stocks Right Now. Should You Bet on a SOUN Squeeze?

- Down 15% in 2026, Should You Buy the Dip in Microsoft Stock?

- 1 ‘Strong Buy’ AI Stock That Wedbush Loves Now: ‘No Lost Deals’ Amid ‘Disruption’

- Okta Is Pushing Higher. Should You Chase the Rally in OKTA Stock After Earnings Here?