Over the past 20 years, Costco (COST) has delivered greater than 1,700% returns for investors, far outstripping the 420% returns by the S&P 500 ($SPX). For the past 21 years, Costco has also paid a dividend, raising it each and every year thereafter.

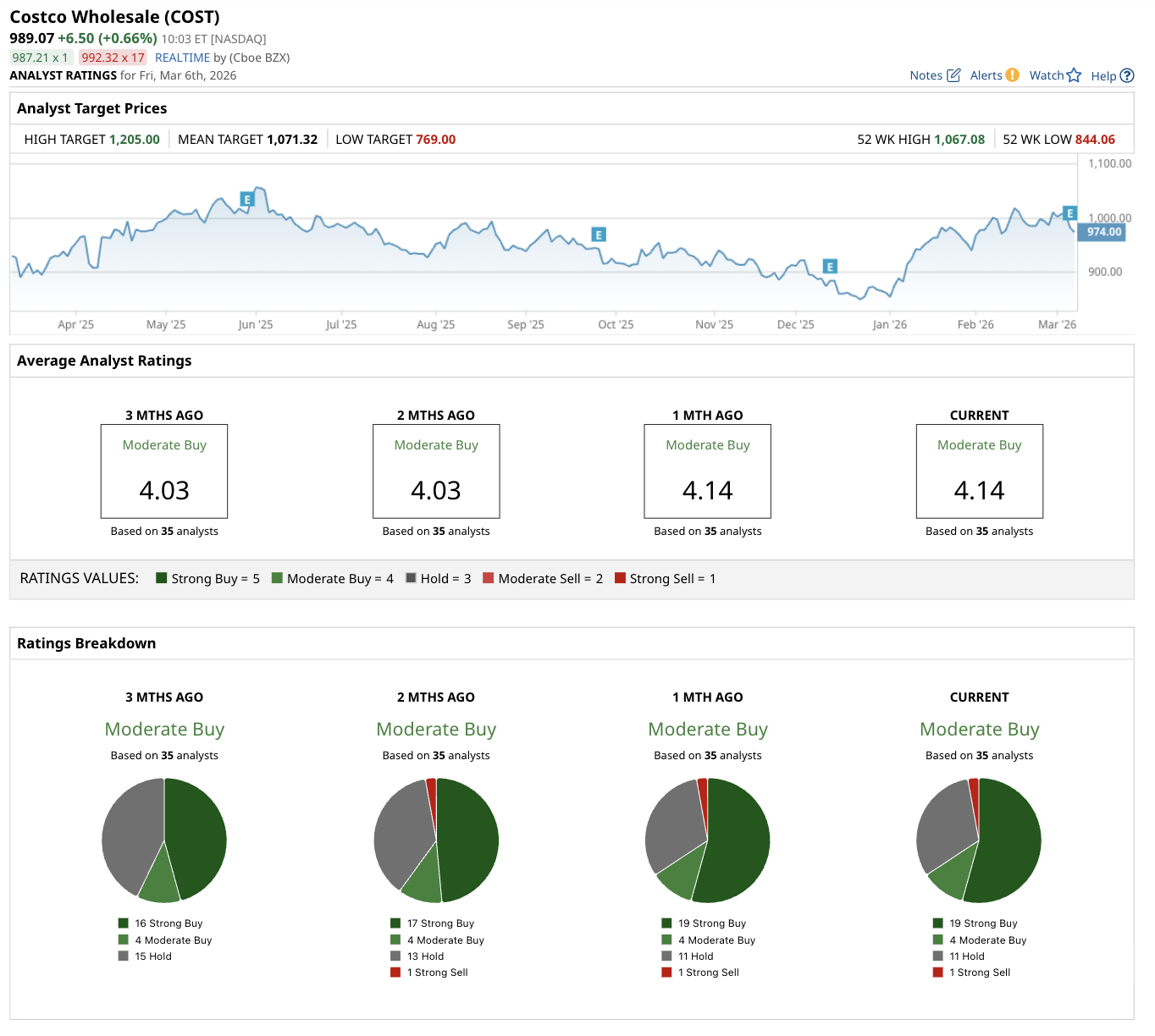

Recently, COST stock crossed above $1,000 per share, but after reporting fiscal second-quarter results, the stock slipped back under the threshold, even though it beat earnings expectations. Is now the time to buy? The company’s journey from regional warehouses to global dominance underscores its ability to reward patient shareholders with both capital appreciation and growing income, making the current moment worth serious consideration for investors seeking quality retail exposure.

A Timeless Winner Regardless of Entry Point

Costco has been a good stock to buy at virtually any time, whether shares are up or down. The stock's long, steady upward trajectory means investors are holding profits no matter when they bought, as the business model consistently compounds value through scale, efficiency, and member loyalty.

Short-term volatility rarely derails the bigger picture because Costco’s focus on delivering unbeatable value keeps customers returning and revenue flowing. Shares of Costco briefly fell below $1,000 this month — opening at $996.50 on March 5 — but have already risen back above the $1,000 mark as of this writing. Market timers often overthink entry points, but history proves that holding through ups and downs has delivered market-beating results for decades.

The best recent buying opportunity for COST stock arrived this past December, when shares dipped to their lowest level in two years, offering a rare discount on a perennial winner. Those who seized that moment have still locked in even gains, yet anyone who purchased earlier sits on substantial unrealized profits today as well.

This resilience stems from Costco’s disciplined approach to expansion, cost control, and relentless innovation in the member experience, turning what could be cyclical retail risk into predictable long-term reward.

Strong Q2 Results Highlight Costco's Core Strengths

Costco released its fiscal Q2 earnings on March 5, and the results painted a picture of underlying strength despite some headline noise. Costco comfortably beat earnings expectations, reflecting tight expense management and healthy operational leverage even amid broader economic caution. Revenue came in slightly below consensus forecasts, a minor shortfall some observers linked to softer discretionary spending patterns.

What truly shone for the retailer, however, was the strong growth in membership revenue, which accelerated nicely and highlighted the enduring appeal of the Costco proposition. This fee income not only provides a high-margin cushion but also signals that members continue to see outsized value in the warehouse shopping format.

A Rock-Solid Foundation

At the core of Costco’s durability sits its membership-based model, which delivers remarkable stability and drives a steady revenue stream that offers excellent visibility. Enjoying renewal rates near 90%, the company benefits from exceptional customer retention that minimizes churn and marketing costs while creating a self-reinforcing flywheel. Happy members renew, new members join, and fees compound reliably.

This recurring revenue base acts as a ballast during periods when general merchandise sales fluctuate, giving management a clear line of sight into cash flows for planning expansions or returning capital to shareholders. The model also limits shrinkage due to theft at rates far below those of competitors like Walmart (WMT) and Target (TGT) . The no-frills warehouse layout, limited product selection, and rapid inventory turnover deter opportunists and keep losses minimal, preserving margins that can then be passed back to members in the form of lower prices.

Combined with prudent balance-sheet management — low leverage, strong free cash flow (FCF) generation, and conservative capital allocation — Costco maintains a rock-solid financial foundation that supports sustained growth without undue risk.

Investors drawn to dividend powerhouses especially appreciate how the annual payout increases have transformed a modest initial yield into meaningful income growth over time. Even at today’s elevated share price, the forward yield paired with consistent raises offers inflation protection and compounding potential that few peers can match.

Key Takeaways on COST Stock

There is never a bad time to buy COST stock, but every once in a while there are some very good times. While the current dip isn’t near the December lows — and investors should scoop up shares with both hands when such instances emerge — buying Costco stock near $1,000 is just as good a time as any.

The company’s proven ability to deliver superior long-term returns, paired with its reliable dividend growth, makes it a foundational holding for portfolios built to last.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart