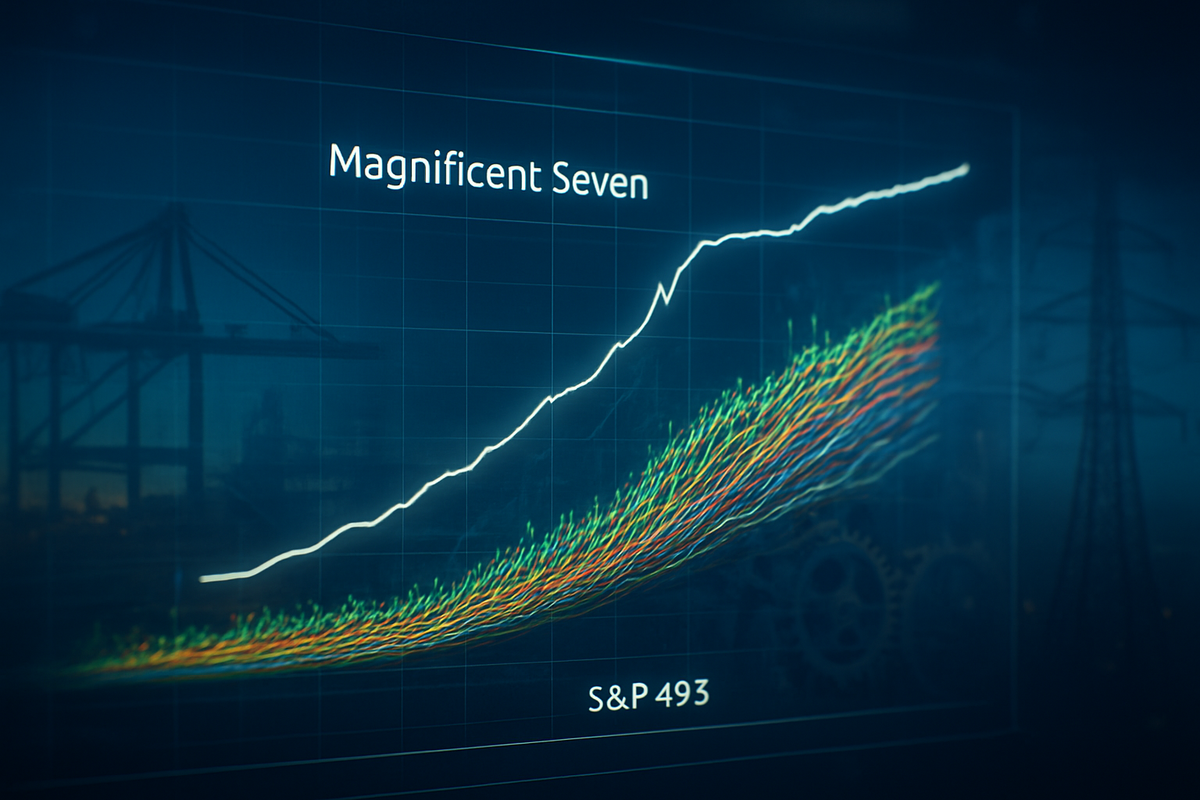

As of February 10, 2026, the long-standing "two-speed" economy that defined the post-pandemic era has finally reached a historic turning point. For years, a handful of mega-cap technology titans—the "Magnificent Seven"—carried the weight of the entire U.S. stock market on their shoulders, while the remaining 493 companies in the S&P 500 largely languished in their shadow. However, recent data confirms that a "Great Convergence" is underway. Capital is aggressively rotating out of overextended tech valuations and into the "S&P 493" and mid-cap sectors, driven by a rare alignment of legislative stimulus, narrowing earnings gaps, and a fundamental shift in investor sentiment toward the "real economy."

The immediate implications of this shift are profound. In the first full week of February 2026, the S&P MidCap 400 (NYSEArca: MDY) staged a massive 4.4% breakout, marking its strongest relative performance against large-caps in nearly two decades. While the technology-heavy Nasdaq 100 remained virtually flat, the broader market has surged to record highs, suggesting that the bull market is no longer a fragile, top-heavy structure but a broad-based rally with deep participation across industrials, materials, and financial sectors.

The 4.4% Breakout and the Legislative Spark

The definitive signal of this market evolution occurred during the opening sessions of February 2026. The mid-cap sector, long considered the "neglected middle child" of the equity world, surged by 4.4% in a single week. This move was not a random fluctuation but the culmination of a technical "bull flag" pattern that had been forming since late 2025. This breakout was catalyzed by the full implementation of the Omnibus Balanced Budget and Business Act (OBBBA), a landmark piece of legislation passed in mid-2025. Often referred to by market participants as the "One Big Beautiful Bill," the OBBBA has fundamentally altered the fiscal landscape for American corporations.

The OBBBA provided two critical pillars of support for the S&P 493 and mid-sized firms. First, it made permanent several corporate tax provisions that were previously set to sunset, providing the long-term fiscal certainty necessary for multi-year capital projects. Second, and perhaps most importantly, it restored the full deductibility of interest expenses under Section 163(j). This change disproportionately benefits mid-cap and industrial companies, which typically carry higher debt-to-equity ratios than the cash-rich technology giants. By effectively lowering the cost of capital, the OBBBA has unlocked a wave of domestic investment in manufacturing and infrastructure that was previously stifled by high interest rates.

The timeline leading to this moment was defined by a steady erosion of the "earnings chasm." In 2024, the Magnificent Seven posted earnings growth that was roughly 30 percentage points higher than the rest of the S&P 500. By the fourth quarter of 2025, that gap had shrunk to just 11 points. As we move deeper into February 2026, projections suggest the gap could narrow to as little as 4 points by the end of the year. Investors are no longer willing to pay a premium for tech growth that is decelerating when they can find accelerating growth in the broader market at a significant discount.

Winners and Losers in the New Market Regime

The clear winners of the Great Convergence are the industrial powerhouses and mid-market innovators that are the primary beneficiaries of the OBBBA. Companies like Caterpillar Inc. (NYSE: CAT) and Deere & Company (NYSE: DE) have seen their order books swell as domestic manufacturing and agricultural modernization projects receive a tax-advantaged green light. Similarly, Eaton Corporation plc (NYSE: ETN), a leader in electrical power management, has become a favorite among institutional investors looking to play the revitalization of the American power grid—a sector that is now growing at a clip once reserved for software-as-a-service (SaaS) firms.

On the other side of the ledger, the Magnificent Seven are facing a "monetization audit." While NVIDIA Corporation (NASDAQ: NVDA), Microsoft Corp. (NASDAQ: MSFT), and Alphabet Inc. (NASDAQ: GOOGL) remain incredibly profitable, the narrative has shifted from the excitement of building Artificial Intelligence (AI) to the grueling task of proving its return on investment (ROI). With capital expenditures for these seven firms projected to hit a staggering $660 billion in 2026, shareholders are beginning to question the sustainability of such spending. Apple Inc. (NASDAQ: AAPL) and Tesla, Inc. (NASDAQ: TSLA) in particular, have struggled to keep pace with the S&P 493, as their mature product cycles and high valuations face increased scrutiny in a world where "Value" is no longer a four-letter word.

Mid-cap players within the S&P MidCap 400 (NYSEArca: MDY) are also finding a second life as AI "diffusion" beneficiaries. Unlike the Mag 7, which provide the AI tools, mid-cap industrial and financial firms are the ones using these tools to achieve massive margin expansion. By automating complex supply chains and back-office operations, these "Old Economy" companies are seeing their first significant productivity leap in decades, leading to the narrowing earnings gap currently captivating Wall Street.

Wider Significance and Historical Precedents

The Great Convergence is more than just a sector rotation; it represents the "de-risking" of the U.S. financial system. For much of 2023 and 2024, the market's extreme concentration was a source of constant anxiety; a single earnings miss from a tech giant could—and often did—drag the entire index into the red. By broadening the base of the rally, the market has become far more resilient to idiosyncratic shocks. This event fits into a broader trend of "reshoring" or "onshoring," where the physical production of goods is prioritized over digital services, a trend accelerated by both the OBBBA and shifting geopolitical priorities.

Historically, this era mirrors the late 1940s and early 1950s, a period when the post-war industrial boom led to a broad-based prosperity that lifted all sectors of the market. It also serves as a sharp contrast to the "Nifty Fifty" era of the 1970s or the Dot-com bubble of 2000, where market concentration eventually led to a painful collapse. In 2026, the convergence suggests a "soft landing" of valuations rather than a crash, as the laggards catch up to the leaders rather than the leaders falling to the level of the laggards.

The regulatory implications of the OBBBA cannot be overstated. By favoring capital-intensive domestic industries through tax policy, the U.S. government has effectively chosen to subsidize the "S&P 493" at the expense of the offshore-heavy, intangible-asset-rich Big Tech firms. This policy pivot marks a definitive end to the era of "unbridled globalization" and the beginning of a fiscal regime that rewards physical presence and domestic job creation.

The Path Ahead: Short-Term Gains and Long-Term Shifts

In the short term, the 4.4% mid-cap breakout is likely to attract further momentum-driven capital. Analysts expect the S&P MidCap 400 to continue its outperformance through at least the first half of 2026, as mutual funds and ETFs rebalance their portfolios to reflect the new earnings reality. We may see a "strategic pivot" from large-cap growth managers who are now forced to hunt for yield and growth in the industrials and materials sectors to meet their performance benchmarks.

However, the long-term challenge will be the sustainability of this domestic boom. As the "AI buildout" phase for tech giants slows, the broader market must prove that its productivity gains are permanent and not merely a one-time result of tax incentives. If inflation re-accelerates due to the massive influx of domestic spending spurred by the OBBBA, the Federal Reserve may be forced to keep interest rates higher for longer, which could eventually put pressure on the very mid-cap firms that are currently leading the charge.

Investors should also watch for potential M&A activity. With the Mag 7 sitting on mountains of cash and their organic growth slowing, we may see a wave of acquisitions as tech giants attempt to buy their way into the industrial and "real world" efficiency gains currently driving the S&P 493. This could lead to a new era of "Industrial Tech" conglomerates, blurring the lines between the sectors once again.

Final Assessment: A Healthier, More Balanced Market

The "Great Convergence" of February 2026 marks the successful transition of the U.S. stock market from a fragile, tech-dependent rally to a robust, diversified bull market. The 4.4% breakout in mid-caps and the outperformance of the S&P 493 are clear indicators that the "earnings chasm" has closed, and the benefits of the digital revolution are finally manifesting in the tangible economy. Driven by the favorable tax climate of the OBBBA, the "real economy" has reclaimed its seat at the head of the table.

For investors, the key takeaway is that the era of "passive tech dominance" is over. Success in 2026 and beyond will require a more nuanced approach, focusing on sectors that benefit from domestic policy tailwinds and productivity-enhancing AI applications. While the Magnificent Seven will remain essential pillars of the economy, they are no longer the only game in town.

As we look toward the coming months, the focus will remain on the sustainability of the mid-cap rally and the ability of the S&P 493 to maintain its newfound earnings momentum. The market has shifted its gaze from the "Cloud" to the "Ground," and so far, the view is remarkably bright.

This content is intended for informational purposes only and is not financial advice.