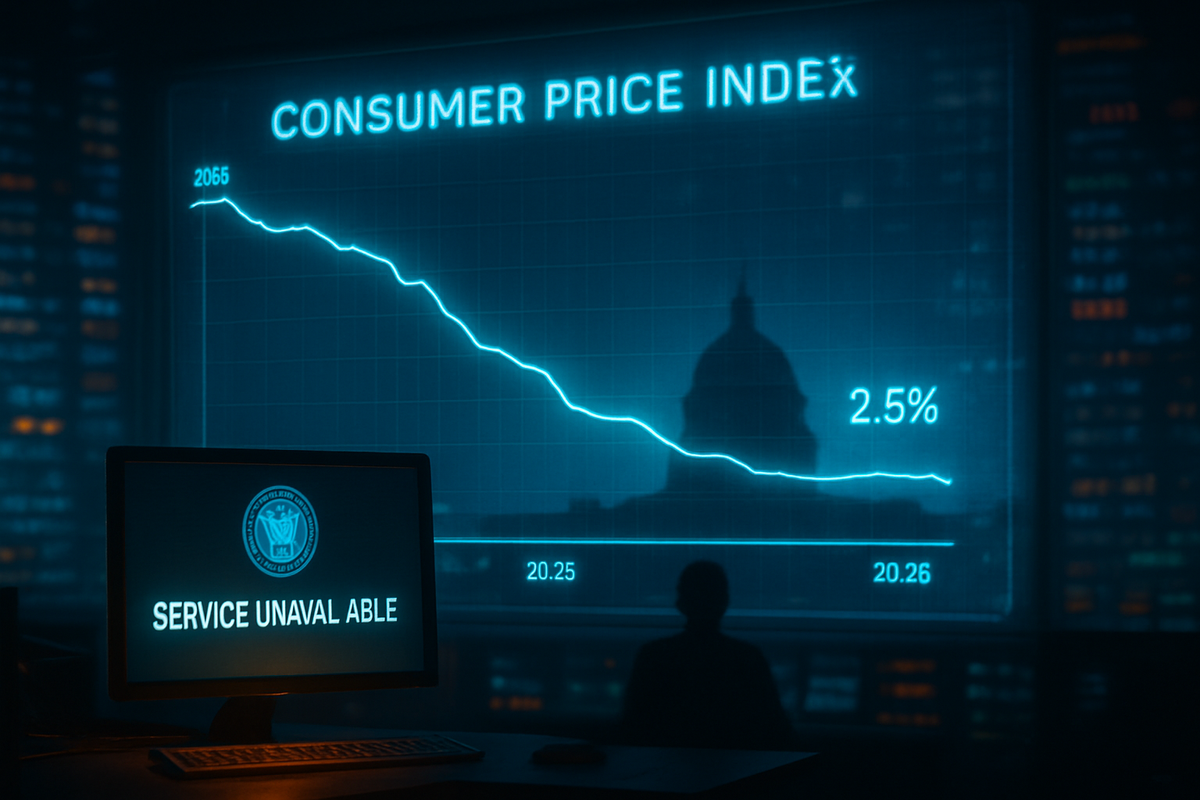

As the calendar turns to mid-February 2026, the American economy stands at a critical juncture. Investors and policymakers are fixated on the upcoming release of the January Consumer Price Index (CPI) report, which is widely anticipated to show a year-over-year inflation rate of 2.5%. This follows a cooling trend from 2025, where inflation hovered around the 2.7% mark. While the headline figure suggests a slow return toward the Federal Reserve’s 2% target, the journey has been anything but smooth, characterized by structural "stickiness" in service costs and a series of disruptive data blackouts.

The anticipation is palpable on Wall Street, as the SPDR S&P 500 ETF Trust (NYSEArca: SPY) remains sensitive to any signals that the Federal Reserve might finally pivot from its "higher-for-longer" interest rate stance. However, the path forward is obscured by the lingering effects of a significant government shutdown in late 2025 and a more recent budgetary impasse in January. These disruptions have turned a standard data release into a high-stakes guessing game for the Federal Reserve and major financial institutions.

A Timeline of Turbulence: The Road to 2.5%

The road to the current 2.5% inflation expectation was paved with administrative and economic obstacles. Throughout much of 2025, inflation proved more resilient than many economists had predicted, ending the year at a stubborn 2.7% in December. This persistence was largely driven by a 43-day government shutdown in October and November 2025, which paralyzed the Bureau of Labor Statistics (BLS). During this period, official price collection was halted, forcing the agency to use "carry-forward imputation"—essentially a statistical best-guess—for its year-end reports.

The resulting "noisy data" created a fog for the Federal Open Market Committee (FOMC). Just as the BLS began to regain its footing, a second, shorter shutdown occurred in late January 2026. Sparked by a budget impasse over Department of Homeland Security funding, this four-day lapse pushed the reporting of the January Jobs Report to February 11 and the CPI report to February 13. While the underlying data for January is believed to be intact, the administrative delays have heightened market anxiety, leaving the Federal Reserve, led by Jerome Powell, with limited clarity on whether the cooling trend is genuine or a statistical artifact.

Market stakeholders have reacted with a mix of caution and skepticism. The CME FedWatch Tool currently indicates a 94.1% probability that the Fed will maintain the federal funds rate in the 3.50%–3.75% range at its upcoming March meeting. Despite the headline cooling to 2.5%, the labor market remains tight with an unemployment rate of 4.3%, suggesting that wage-push inflation could still ignite if the central bank acts too aggressively on rate cuts.

Winners and Losers in the Wait-and-See Economy

The current environment of elevated rates and "stalled descent" inflation has created a bifurcated market. Large-cap financial institutions like JPMorgan Chase & Co. (NYSE: JPM) have emerged as relative winners. These banks continue to benefit from high net interest margins, as they earn more on loans than they pay out in interest to depositors. As long as the Fed maintains its "hawkish pause," the banking sector remains a primary beneficiary of the prolonged high-rate environment.

Similarly, cash-rich technology giants such as Microsoft Corp. (NASDAQ: MSFT) and Apple Inc. (NASDAQ: AAPL) have shown resilience. These companies carry massive cash reserves that generate significant interest income, shielding them from the higher borrowing costs that plague smaller competitors. Their strong balance sheets allow them to continue investing in R&D and artificial intelligence initiatives even as the broader cost of capital remains restrictive.

Conversely, the real estate and housing sectors continue to struggle. The Vanguard Real Estate ETF (NYSEArca: VNQ) has faced headwinds as high mortgage rates dampen homebuyer demand and increase the cost of carry for commercial property owners. Homebuilders like Lennar Corp. (NYSE: LEN) find themselves in a difficult position; while housing supply remains low, the "higher-for-longer" rate narrative keeps potential buyers on the sidelines, waiting for a rate cut that has been repeatedly pushed into the second half of 2026.

The 2.5% Litmus Test and the Fed’s Next Chapter

The significance of the 2.5% figure extends beyond a simple price measurement; it serves as a litmus test for the Fed's credibility. For much of the past decade, 2% was the untouchable target. In the current era of shifting global trade and potential new tariffs, some economists argue that 2.5% may be the "new neutral." However, the Fed has been hesitant to officially move the goalposts, fearing that doing so would unanchor inflation expectations among the public and the markets.

This period is also defined by a sense of "lame-duck" transition. Chair Jerome Powell’s term is set to expire in May 2026, and the uncertainty surrounding his successor is weighing on policy. Historically, the Fed avoids major policy shifts during leadership transitions to prevent market volatility. This suggests that even if tomorrow’s CPI print is favorable, a formal rate-cutting cycle may not begin until a new chair is seated and confirmed, likely delaying any significant relief for the markets until the third quarter of 2026.

The broader industry trend shows a shift from general inflation to "sector-specific" volatility. While energy prices have provided a disinflationary tailwind in early 2026, the service sector and insurance costs remain elevated. This fragmented inflation landscape makes the Fed's job increasingly complex, as a "one-size-fits-all" interest rate policy may over-tighten some sectors while failing to cool others.

Strategic Pivots: Looking Toward the Second Half of 2026

As we look toward the remainder of 2026, the consensus among major investment banks like Goldman Sachs Group Inc. (NYSE: GS) is that rate cuts are a matter of "when," not "if." Most analysts have adjusted their forecasts to expect only one or two 25-basis-point cuts in the latter half of the year, targeting a terminal rate of 3.00%–3.25% by year-end. This conservative outlook requires a strategic pivot from investors who were previously betting on a more rapid return to easy-money conditions.

Market participants must now navigate a "long plateau." In the short term, the focus will remain on whether the January CPI report confirms the 2.5% forecast or provides a "hawkish surprise" that could send yields higher. In the long term, the challenge will be adapting to a world where inflation remains slightly above the historical norm, and the "Fed Put"—the idea that the central bank will quickly bail out markets—is no longer a guaranteed feature of the financial landscape.

Conclusion: The Inflation Watch Continues

The early 2026 CPI trend represents a fragile victory over the runaway inflation of years past. While a move from 2.7% to 2.5% is a step in the right direction, the combination of administrative data delays and a resilient labor market suggests that the "last mile" of the inflation fight will be the most difficult. For the Federal Reserve, the priority remains ensuring that the downward trend is sustainable before committing to any policy easing.

For investors, the key takeaways are patience and selectivity. The "data blackout" caused by the government shutdowns has made fundamental analysis more difficult, but the resilience of big-cap tech and banks suggests where the current market strength lies. Moving forward, the most important indicators to watch will be core service inflation and the identity of the next Federal Reserve Chair. As we await tomorrow's delayed report, the market is bracing for a result that could either solidify the cooling narrative or force a painful reassessment of the 2026 economic outlook.

This content is intended for informational purposes only and is not financial advice.