The U.S. labor market has long been a source of economic resilience, but recent data released in early March 2026 has sent a wave of confusion through Wall Street and the hallowed halls of the Federal Reserve. Investors are currently grappling with two starkly different narratives: a resilient private sector versus a broader contraction in non-farm payrolls. The discrepancy has reignited debates over "stagflation" and placed the Federal Reserve in a precarious position as it prepares for its upcoming policy meeting.

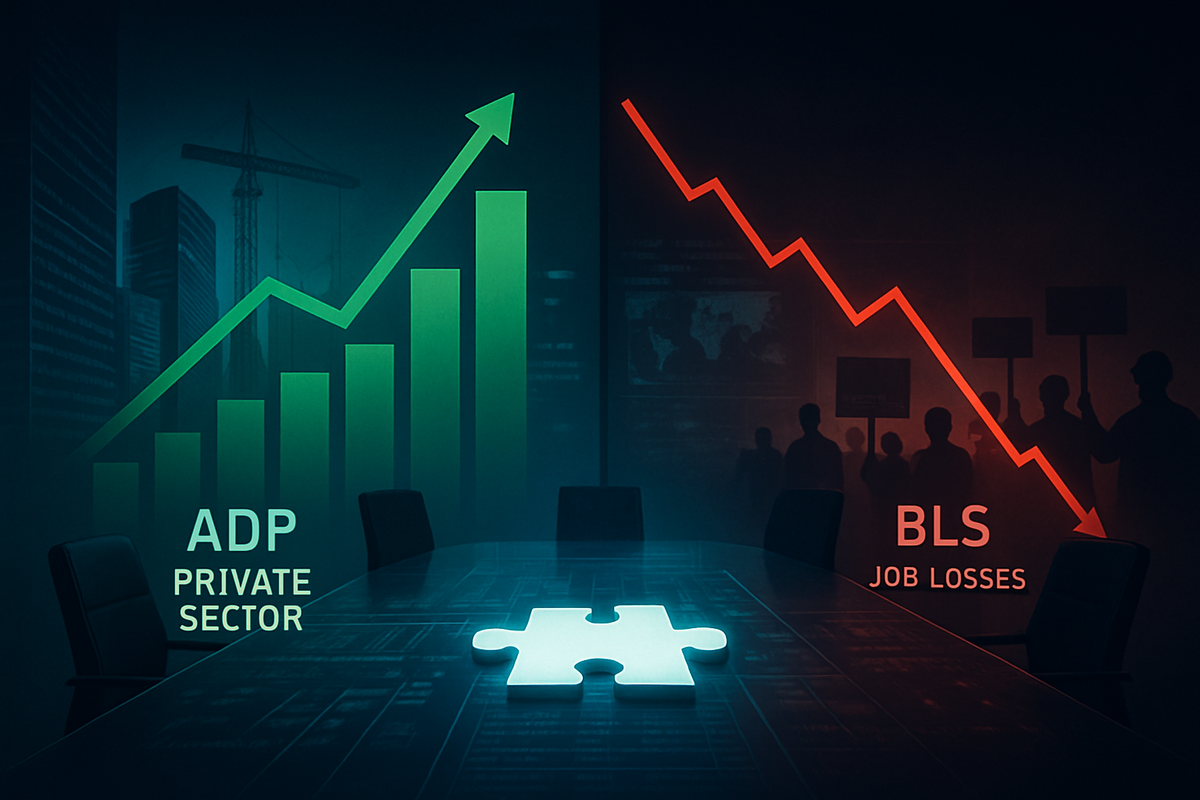

On March 6, 2026, the Bureau of Labor Statistics (BLS) shocked the market by reporting a net loss of 92,000 non-farm payroll jobs for February. This figure stood in sharp contrast to the ADP National Employment Report, published just days earlier by Automatic Data Processing, Inc. (NASDAQ: ADP), which showed a private-sector gain of 63,000 jobs. The divergence of 155,000 positions has left analysts questioning the true health of the American worker and whether the economy is nearing a tipping point.

A Tale of Two Reports: The Statistical Disconnect

The February BLS report was a "shocker" by all accounts, missing the consensus analyst estimate of a 60,000 gain by a massive margin. Beyond the headline loss of 92,000 jobs, the report included downward revisions to previous months, trimming December and January by a cumulative 69,000 positions. The national unemployment rate ticked up to 4.4%, a level that historically signals a cooling trend. However, the ADP report painted a different picture, beating its own estimate of 50,000 gains and suggesting that private-sector hiring remained positive, if modest.

Economists have identified several "one-off" factors to explain this chasm. A major strike at Kaiser Permanente during the BLS survey reference week sidelined over 30,000 workers. Because the BLS "Establishment Survey" only counts individuals as employed if they receive pay during that specific week, these strikers were recorded as job losses. Additionally, federal downsizing efforts removed roughly 15,000 government jobs from the non-farm total—a drag that the private-only ADP report ignores. Severe winter weather in the Northeast also impacted construction and leisure sectors, creating "noise" that the BLS captures more acutely than ADP’s broader payroll processing data.

The initial market reaction on March 6 was swift and severe. The Dow Jones Industrial Average dropped nearly 450 points, or 0.95%, while the tech-heavy Nasdaq-100 fell 1.6%. While Treasury yields initially plummeted in a "flight to safety," they rebounded by midday as investors digested a 0.4% rise in average hourly earnings. This "sticky" wage growth, paired with job losses, raised the specter of stagflation—a scenario where the economy slows while inflation remains stubbornly high.

Winners and Losers in a "Low-Hire, Low-Fire" Economy

The staffing industry is feeling the brunt of what analysts call a "hiring recession." Robert Half Inc. (NYSE: RHI) saw its shares hit 52-week lows following the report, as corporations pulled back on permanent placements and contract labor. Surprisingly, ManpowerGroup Inc. (NYSE: MAN) managed a slight 1.39% gain on the day of the release, as some investors bet the company was oversold, though analysts at Barclays quickly countered this optimism with a downgrade and a slashed price target.

Financial giants also faced headwinds. JPMorgan Chase & Co. (NYSE: JPM) and Goldman Sachs Group, Inc. (NYSE: GS) saw their shares decline as the jobs miss signaled potential credit risk and compressed margins. Goldman Sachs is reportedly preparing for its own defensive shift, planning new rounds of layoffs in middle-office and engineering roles to brace for slower capital market activity. The prospect of lower interest rates, which initially seemed like a boon, was overshadowed by the fear of a broader economic contraction.

In the technology sector, the reaction was bifurcated. High-growth leaders like Nvidia Corp. (NASDAQ: NVDA) and Microsoft Corp. (NASDAQ: MSFT) saw a brief intraday spike as yields dipped, but the rally evaporated as oil prices surged due to geopolitical tensions in the Middle East. Semiconductor players like ASML Holding N.V. (NASDAQ: ASML) and Micron Technology, Inc. (NASDAQ: MU) were hit particularly hard, ending the session down more than 4% as concerns over global demand outweighed any hopes for a "dovish" Fed pivot.

Policy Implications and the Fed’s Next Move

This jobs data presents a "complex puzzle" for the Federal Reserve ahead of its March 17–18 meeting. Fed Governor Stephen Miran has already suggested that the job losses bolster the case for interest rate cuts, arguing that labor market stability should now take precedence over inflation, which remains slightly above the 2% target. Conversely, San Francisco Fed President Mary Daly has urged caution, noting that one month of strike-distorted data should not dictate a long-term policy shift.

The broader significance lies in the transition from a "bad news is good news" market (where weak data leads to rallies on rate-cut hopes) to a "bad news is bad news" reality. With wage growth still rising at 4.5% year-over-year, the Fed faces a dilemma: cutting rates to save the labor market could reignite inflation, while holding rates steady could push the economy into a formal recession. This "stagflationary" signal is a departure from the "Goldilocks" environment investors had hoped for at the start of 2026.

Historically, such wide discrepancies between ADP and BLS data often precede significant revisions or signal a turning point in the business cycle. The 2026 labor market appears to be in a "low-hire, low-fire" equilibrium, where companies are hesitant to add new staff but are paying a premium to retain the talent they already have. This behavior suggests that while the "Great Resignation" is long over, a "Great Stagnation" may be beginning.

What Comes Next: Scenarios for the Second Quarter

In the short term, all eyes will be on the March jobs report (to be released in April) to see if the February losses were truly an anomaly caused by strikes and weather. If the BLS data "catches up" to the ADP's positive trend, markets may recover. However, if the 92,000 loss is confirmed or worsened in subsequent reports, the Federal Reserve may be forced to initiate a series of aggressive rate cuts that were not on the table just two months ago.

For public companies, the strategic pivot is likely to be toward efficiency and "labor hoarding." Rather than broad layoffs, many firms may continue to freeze hiring while utilizing AI to maintain productivity. Residential construction companies like Lennar Corp. (NYSE: LEN), D.R. Horton, Inc. (NYSE: DHI), and PulteGroup, Inc. (NYSE: PHM) are particularly vulnerable; they need the 10-year Treasury yield to stabilize below 4% to keep mortgage rates attractive, but current volatility is making the spring home-buying season increasingly uncertain.

Closing Thoughts for Investors

The conflicting jobs data of February 2026 serves as a reminder that the "headline" numbers often mask a deeper, more complicated reality. While the BLS report was undeniably grim, the underlying private sector strength suggested by ADP and the temporary nature of the Kaiser Permanente strike offer a glimmer of hope that the U.S. economy isn't falling off a cliff just yet.

Moving forward, investors should watch for the Fed's March 18 statement and the subsequent "dot plot" of interest rate expectations. The key takeaway is that labor market stability is no longer a given. For the first time in years, "recession" is a word being whispered more loudly than "inflation." Investors would be wise to monitor the 10-year yield and energy prices, as these will likely be the primary drivers of market sentiment until the labor data achieves some form of reconciliation.

This content is intended for informational purposes only and is not financial advice