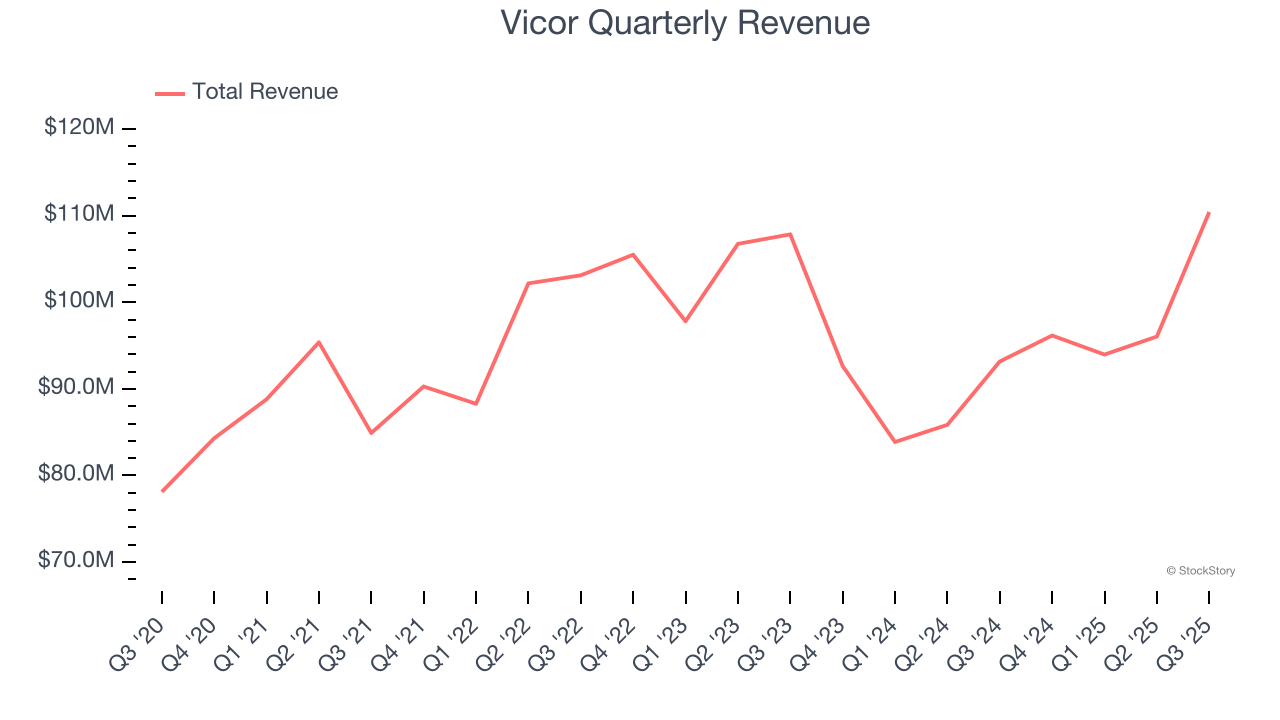

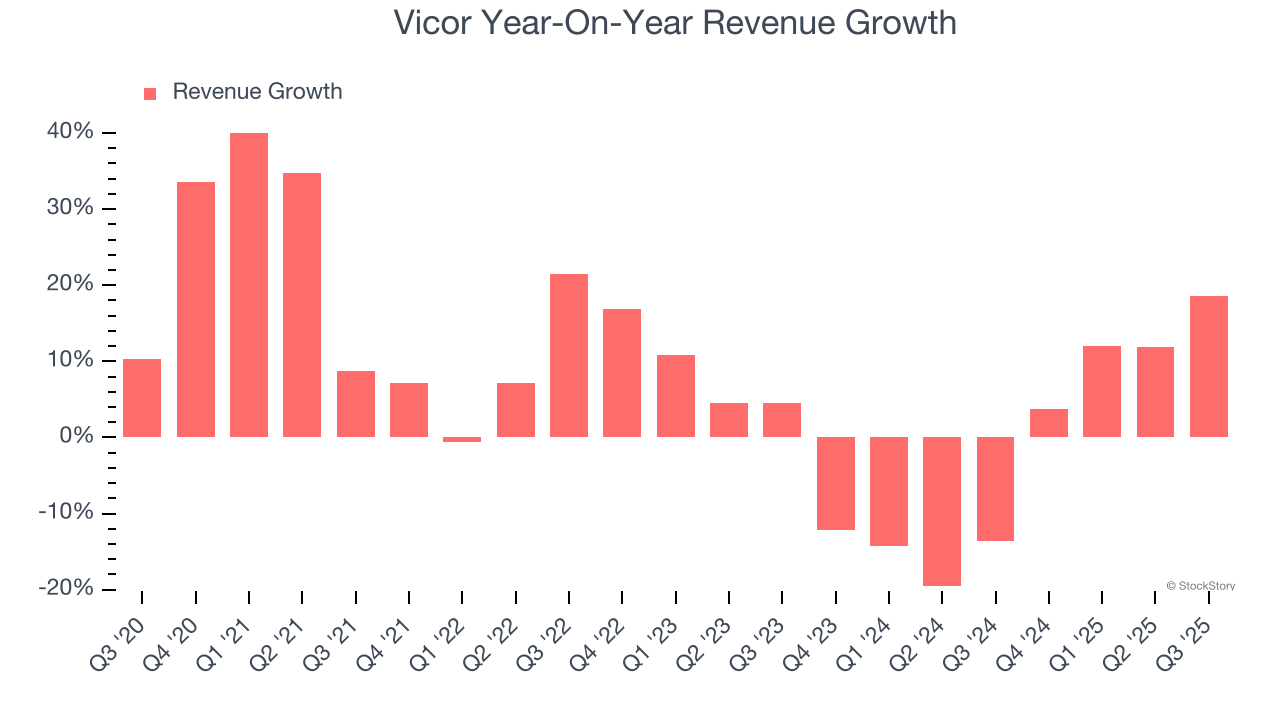

Power conversion and control solutions provider Vicor Corporation (NASDAQ: VICR) reported Q3 CY2025 results exceeding the market’s revenue expectations, with sales up 18.5% year on year to $110.4 million. Its GAAP profit of $0.63 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Vicor? Find out by accessing our full research report, it’s free for active Edge members.

Vicor (VICR) Q3 CY2025 Highlights:

- Revenue: $110.4 million vs analyst estimates of $95.4 million (18.5% year-on-year growth, 15.7% beat)

- EPS (GAAP): $0.63 vs analyst estimates of $0.12 (significant beat)

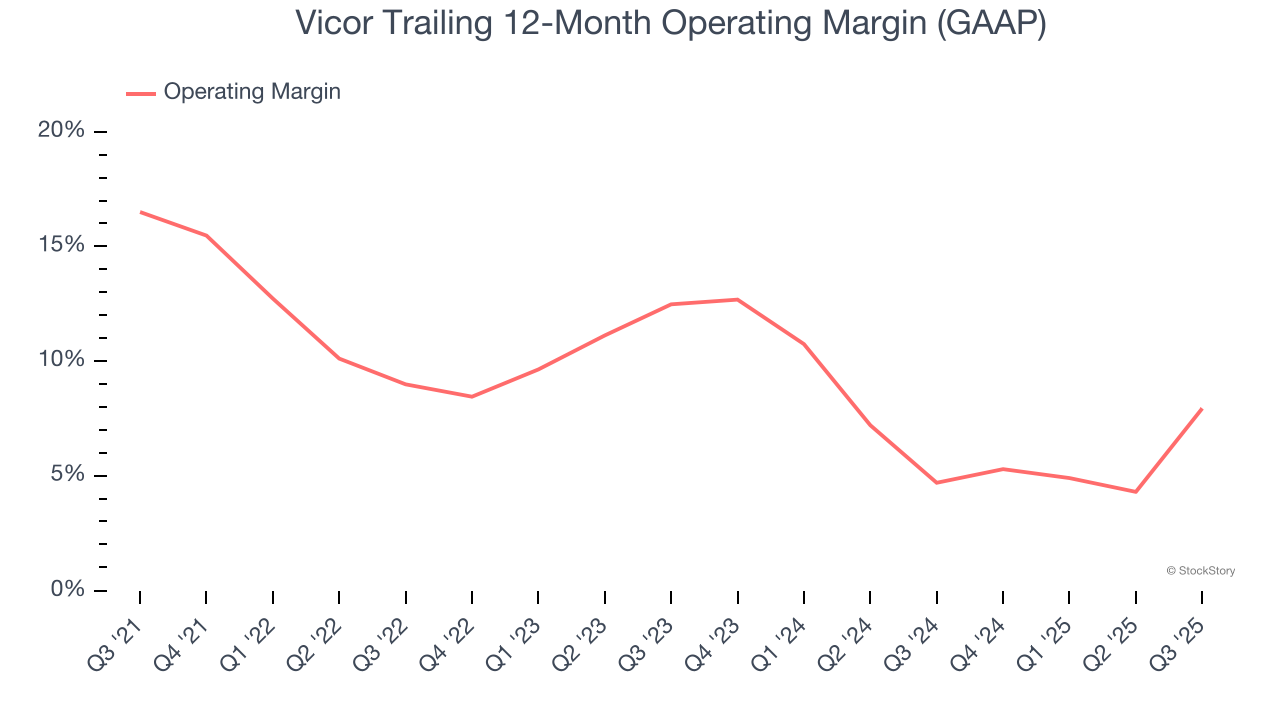

- Operating Margin: 18.9%, up from 6.1% in the same quarter last year

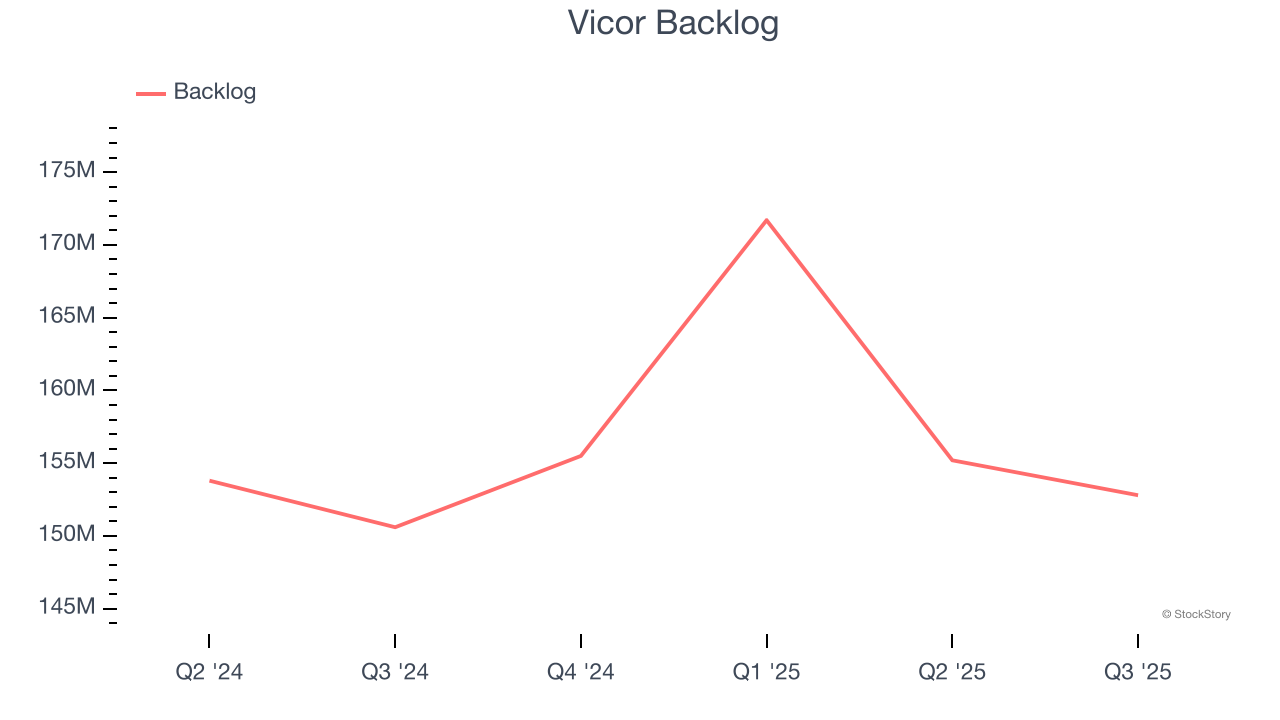

- Backlog: $152.8 million at quarter end, up 1.5% year on year

- Market Capitalization: $2.61 billion

Commenting on third quarter performance, Chief Executive Officer Dr. Patrizio Vinciarelli stated: “Licensing revenue reached a record rate in Q3 following the litigation settlement for prior infringement recorded in Q2. As high density power systems pioneered by Vicor, including NBMs and VPD, are on the critical path of high performance computing, I expect Vicor’s IP licensing practice to grow substantially. OEMs and hyper-scalers need a license, or need to renew their license or expand its scope. Vicor is pursuing additional actions to curtail access to infringing computing systems sourced from infringing contract manufacturers relying on infringing power module makers.”

Company Overview

Founded by a researcher at the Massachusetts Institute of Technology, Vicor (NASDAQ: VICR) provides electrical power conversion and delivery products for a range of industries.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Vicor’s sales grew at a decent 7.6% compounded annual growth rate over the last five years. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Vicor’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 2.6% over the last two years. Vicor isn’t alone in its struggles as the Electronic Components industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

Vicor also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Vicor’s backlog reached $152.8 million in the latest quarter and averaged 1.2% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Vicor’s products and services but raises concerns about capacity constraints.

This quarter, Vicor reported year-on-year revenue growth of 18.5%, and its $110.4 million of revenue exceeded Wall Street’s estimates by 15.7%.

Looking ahead, sell-side analysts expect revenue to grow 6.9% over the next 12 months. Although this projection suggests its newer products and services will catalyze better top-line performance, it is still below average for the sector.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Vicor has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10.1%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Vicor’s operating margin decreased by 8.6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q3, Vicor generated an operating margin profit margin of 18.9%, up 12.8 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

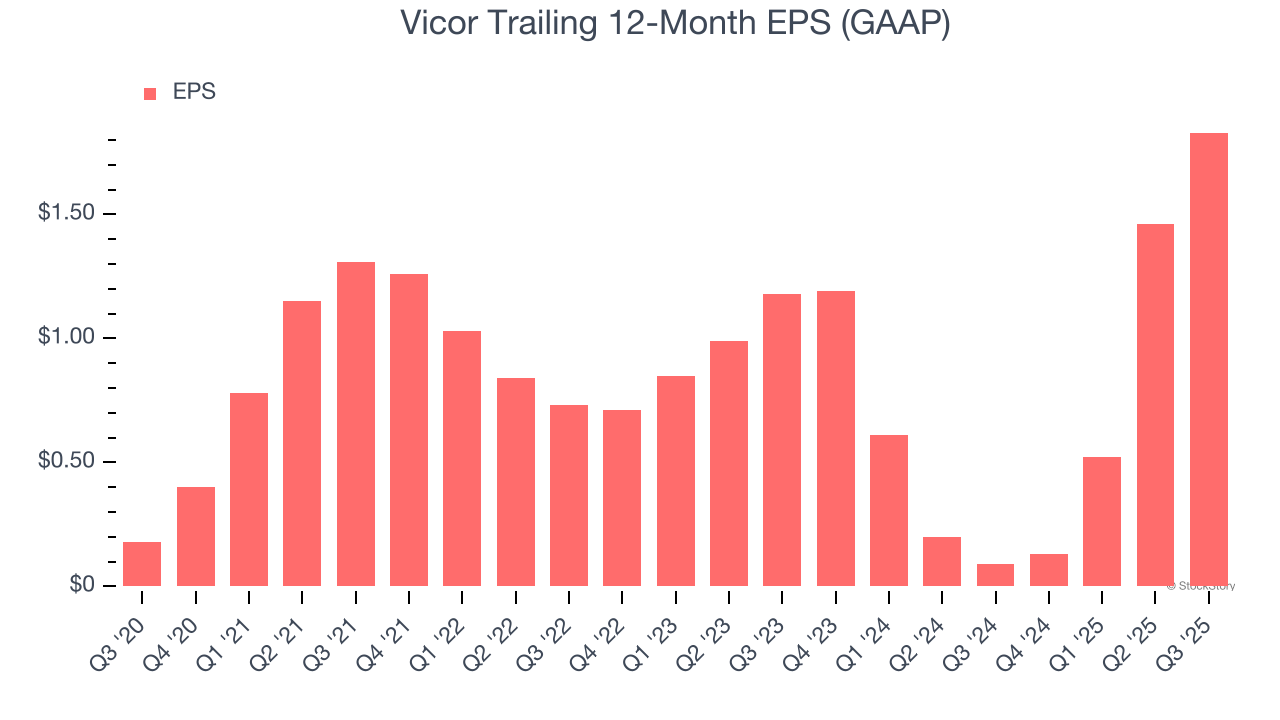

Vicor’s EPS grew at an astounding 59% compounded annual growth rate over the last five years, higher than its 7.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Vicor, its two-year annual EPS growth of 24.5% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q3, Vicor reported EPS of $0.63, up from $0.26 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Vicor’s full-year EPS of $1.83 to shrink by 41.5%.

Key Takeaways from Vicor’s Q3 Results

It was good to see Vicor beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock remained flat at $66.19 immediately after reporting.

Sure, Vicor had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.