As the Q3 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the specialty finance industry, including PROG (NYSE: PRG) and its peers.

Specialty finance companies provide targeted lending or financial services for specific industries or needs. They benefit from expertise in particular sectors, often reduced competition in specialized niches, and tailored underwriting that can yield higher margins. Challenges include concentration risk in specific industries, difficulty achieving scale efficiencies, and potential vulnerability during sector-specific downturns affecting their specialized markets.

The 9 specialty finance stocks we track reported a mixed Q3. As a group, revenues missed analysts’ consensus estimates by 3%.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

PROG (NYSE: PRG)

Evolving from its origins as Aaron's, Inc. before rebranding in 2020, PROG Holdings (NYSE: PRG) provides alternative payment solutions including lease-to-own options and second-look credit products for consumers who may not qualify for traditional financing.

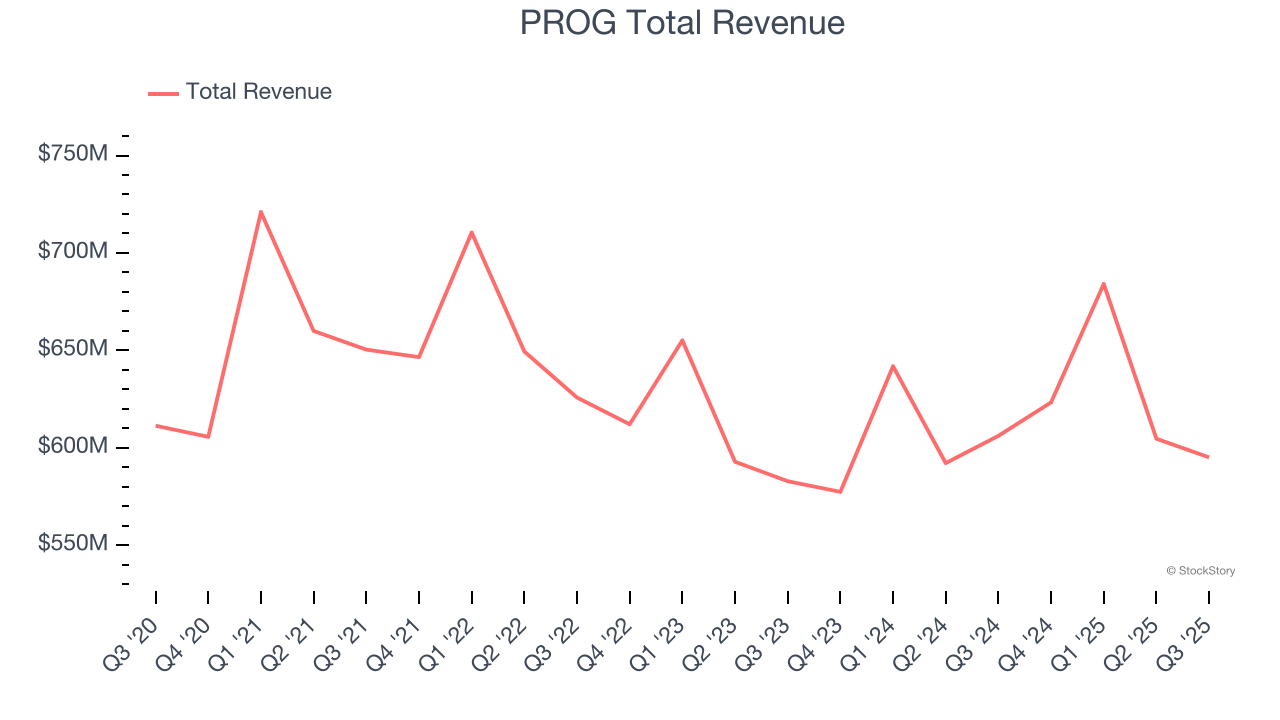

PROG reported revenues of $595.1 million, down 1.8% year on year. This print exceeded analysts’ expectations by 1.5%. Overall, it was a strong quarter for the company with a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

"Our third quarter results once again highlight the strength and consistency of our execution, even as consumers face ongoing economic pressures," said Steve Michaels, President and CEO of PROG Holdings.

Unsurprisingly, the stock is down 16.2% since reporting and currently trades at $27.46.

Is now the time to buy PROG? Access our full analysis of the earnings results here, it’s free for active Edge members.

Best Q3: Encore Capital Group (NASDAQ: ECPG)

Operating in the often misunderstood world of debt collection since 1999, Encore Capital Group (NASDAQ: ECPG) purchases portfolios of defaulted consumer debt at deep discounts and works with individuals to recover these obligations while helping them toward financial recovery.

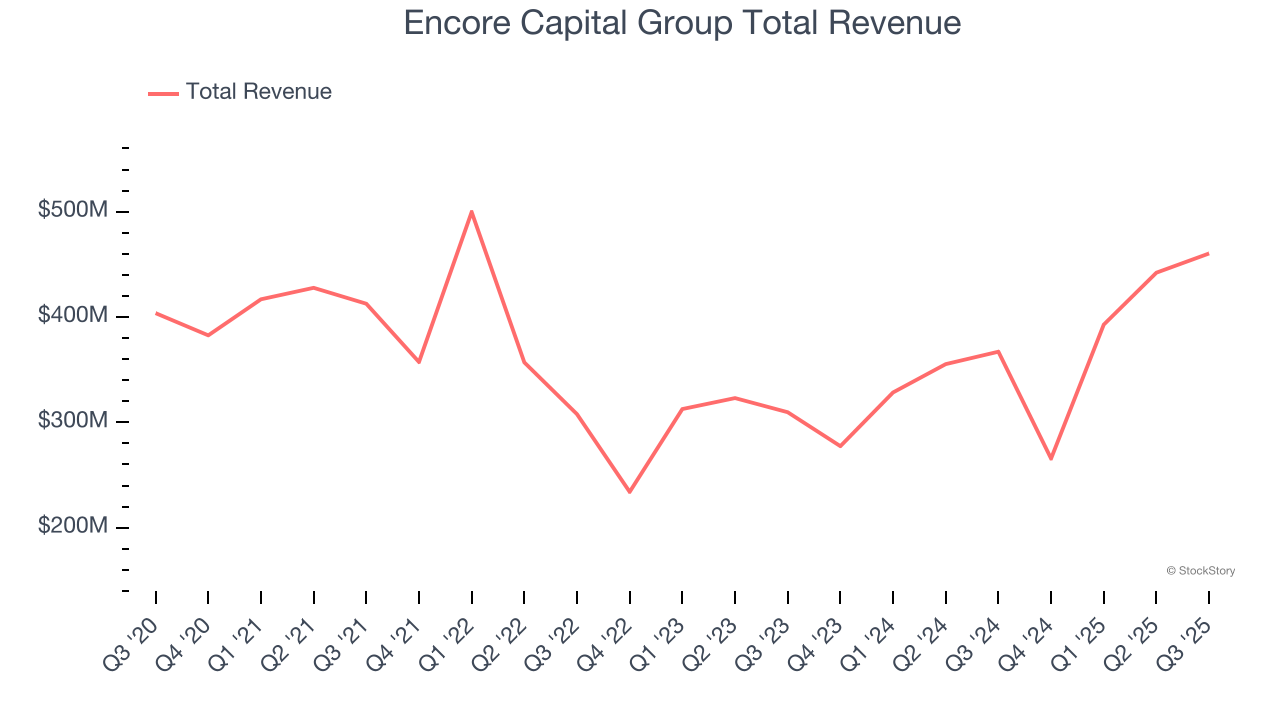

Encore Capital Group reported revenues of $460.4 million, up 25.4% year on year, outperforming analysts’ expectations by 11.9%. The business had an incredible quarter with a beat of analysts’ EPS estimates and an impressive beat of analysts’ revenue estimates.

The market seems happy with the results as the stock is up 9.8% since reporting. It currently trades at $47.

Is now the time to buy Encore Capital Group? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: DigitalBridge (NYSE: DBRG)

Transforming from a traditional real estate investor to a digital-focused powerhouse in 2021, DigitalBridge Group (NYSE: DBRG) is a global digital infrastructure investment firm that manages capital and operates assets across data centers, cell towers, fiber networks, and edge infrastructure.

DigitalBridge reported revenues of $3.82 million, down 95% year on year, falling short of analysts’ expectations by 96.2%. It was a disappointing quarter as it posted a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ revenue estimates.

DigitalBridge delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 16.5% since the results and currently trades at $10.63.

Read our full analysis of DigitalBridge’s results here.

Main Street Capital (NYSE: MAIN)

With a focus on building long-term partnerships rather than quick transactions, Main Street Capital (NYSE: MAIN) is a business development company that provides long-term debt and equity capital to lower middle market and middle market companies.

Main Street Capital reported revenues of $139.8 million, up 2.2% year on year. This result met analysts’ expectations. More broadly, it was a mixed quarter as it recorded EPS in line with analysts’ estimates.

The stock is up 1.2% since reporting and currently trades at $57.88.

Read our full, actionable report on Main Street Capital here, it’s free for active Edge members.

HA Sustainable Infrastructure Capital (NYSE: HASI)

With a proprietary "CarbonCount" metric that quantifies the environmental impact of each dollar invested, HA Sustainable Infrastructure Capital (NYSE: HASI) is an investment firm that finances and develops climate-positive infrastructure projects across renewable energy, energy efficiency, and ecological restoration.

HA Sustainable Infrastructure Capital reported revenues of $139.2 million, up 51.5% year on year. This print beat analysts’ expectations by 58.5%. It was a stunning quarter as it also produced a solid beat of analysts’ revenue estimates and an impressive beat of analysts’ EBITDA estimates.

HA Sustainable Infrastructure Capital delivered the biggest analyst estimates beat and fastest revenue growth among its peers. The stock is up 15.5% since reporting and currently trades at $32.98.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.