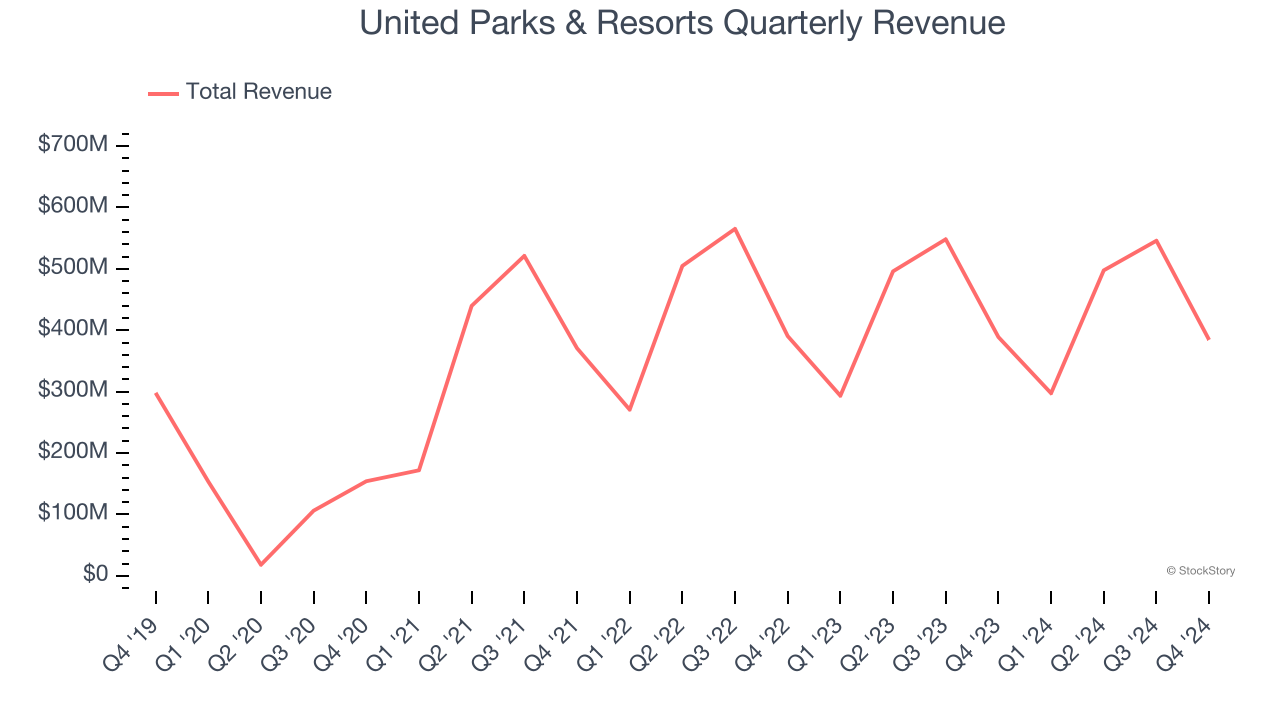

Theme park operator United Parks & Resorts (NYSE: PRKS) beat Wall Street’s revenue expectations in Q4 CY2024, but sales fell by 1.2% year on year to $384.4 million. Its GAAP profit of $0.50 per share was 21% below analysts’ consensus estimates.

Is now the time to buy United Parks & Resorts? Find out by accessing our full research report, it’s free.

United Parks & Resorts (PRKS) Q4 CY2024 Highlights:

- Revenue: $384.4 million vs analyst estimates of $380.4 million (1.2% year-on-year decline, 1% beat)

- EPS (GAAP): $0.50 vs analyst expectations of $0.63 (21% miss)

- Adjusted EBITDA: $144.5 million vs analyst estimates of $138.6 million (37.6% margin, 4.2% beat)

- Operating Margin: 19.7%, down from 23% in the same quarter last year

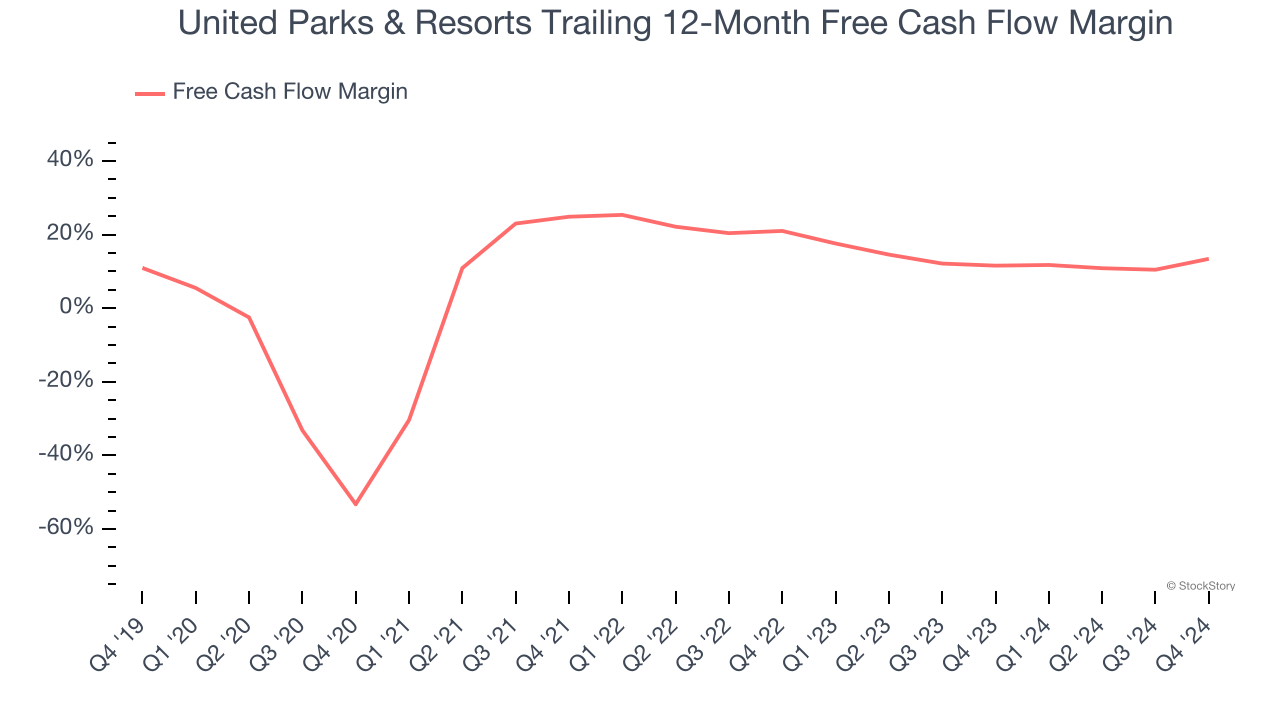

- Free Cash Flow Margin: 22.4%, up from 9.2% in the same quarter last year

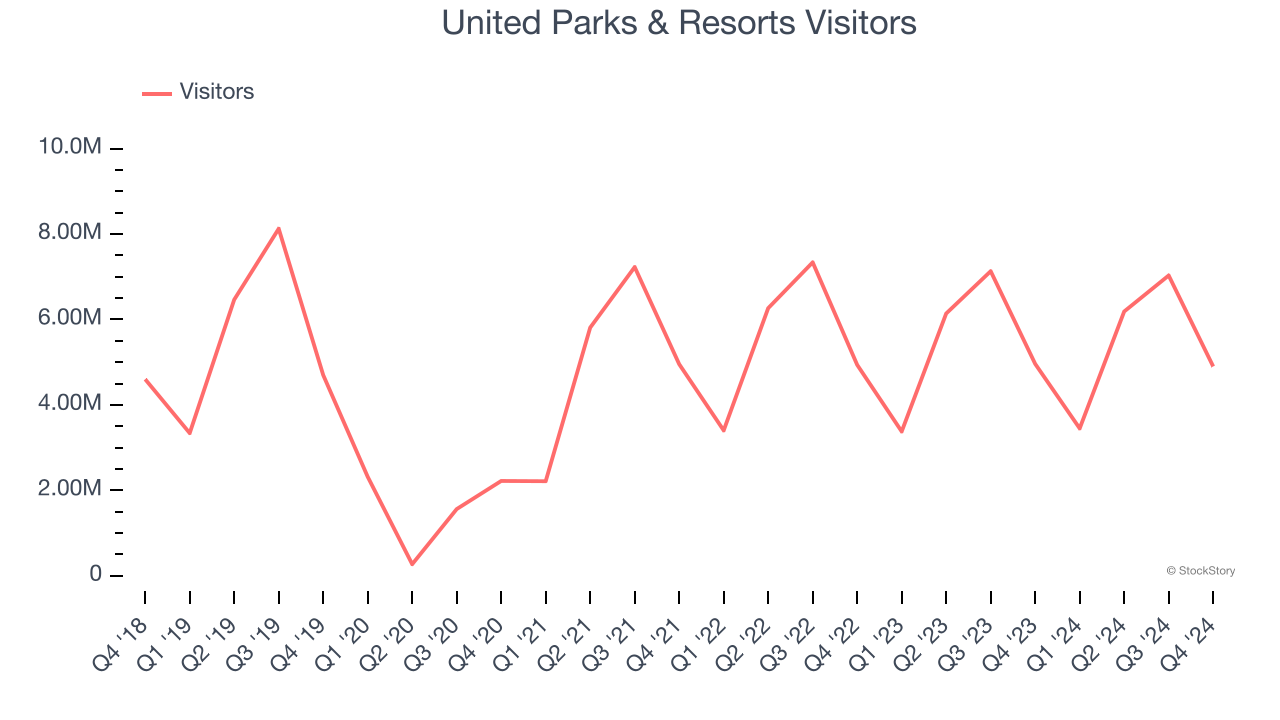

- Visitors: 4.9 million, down 60,000 year on year

- Market Capitalization: $3.00 billion

"We are pleased to report another quarter and fiscal year of strong financial results," said Marc Swanson, Chief Executive Officer of United Parks & Resorts,

Company Overview

Parent company of SeaWorld and home of the world-famous Shamu, United Parks & Resorts (NYSE: PRKS) is a theme park chain featuring marine life, live entertainment, roller coasters, and waterparks.

Leisure Facilities

Leisure facilities companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted their spending from "things" to "experiences". Leisure facilities seek to benefit but must innovate to do so because of the industry's high competition and capital intensity.

Sales Growth

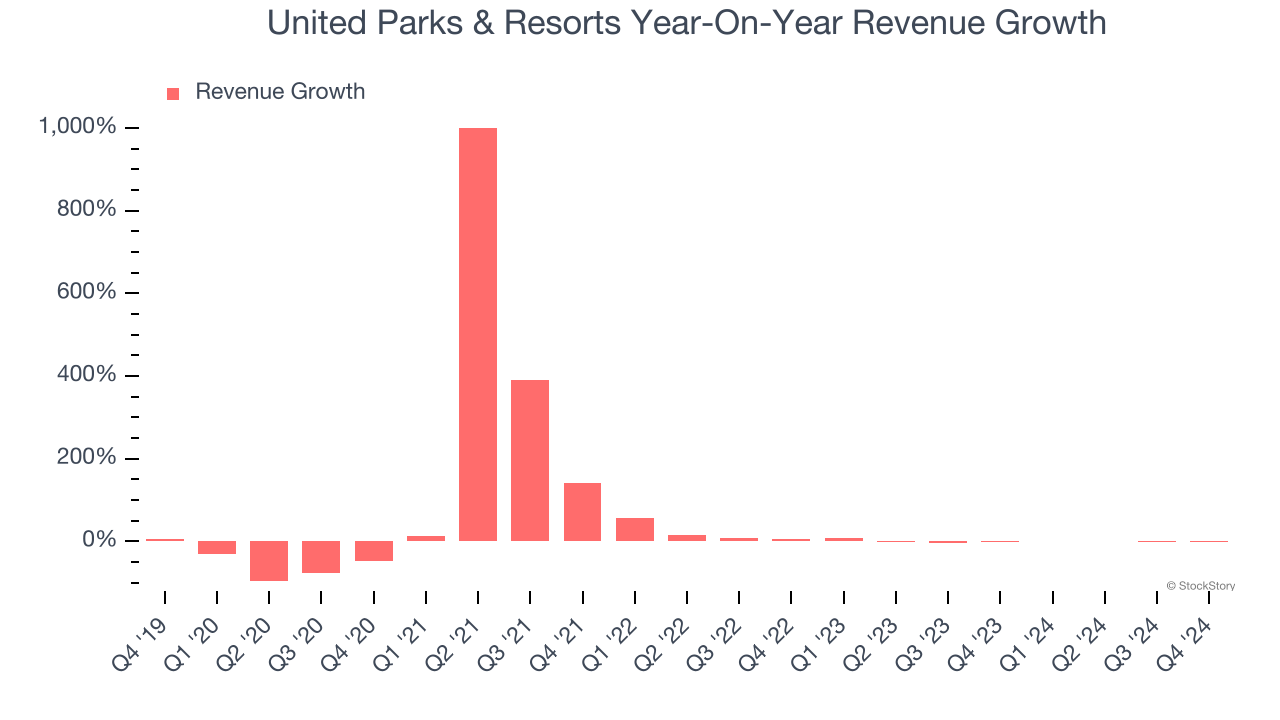

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, United Parks & Resorts grew its sales at a sluggish 4.3% compounded annual growth rate. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. United Parks & Resorts’s recent history shows its demand slowed as its revenue was flat over the last two years. Note that COVID hurt United Parks & Resorts’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

We can dig further into the company’s revenue dynamics by analyzing its number of visitors, which reached 4.9 million in the latest quarter. Over the last two years, United Parks & Resorts’s visitors were flat. Because this number aligns with its revenue growth during the same period, we can see the company’s monetization was fairly consistent.

This quarter, United Parks & Resorts’s revenue fell by 1.2% year on year to $384.4 million but beat Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 1.3% over the next 12 months, similar to its two-year rate. While this projection suggests its newer products and services will spur better top-line performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

United Parks & Resorts has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 12.5% over the last two years, slightly better than the broader consumer discretionary sector.

United Parks & Resorts’s free cash flow clocked in at $86.25 million in Q4, equivalent to a 22.4% margin. This result was good as its margin was 13.2 percentage points higher than in the same quarter last year. Its cash profitability was also above its two-year level, and we hope the company can build on this trend.

Key Takeaways from United Parks & Resorts’s Q4 Results

It was encouraging to see United Parks & Resorts beat analysts’ EBITDA expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its EPS missed significantly. Overall, this quarter was mixed. The stock remained flat at $55.03 immediately after reporting.

Big picture, is United Parks & Resorts a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.