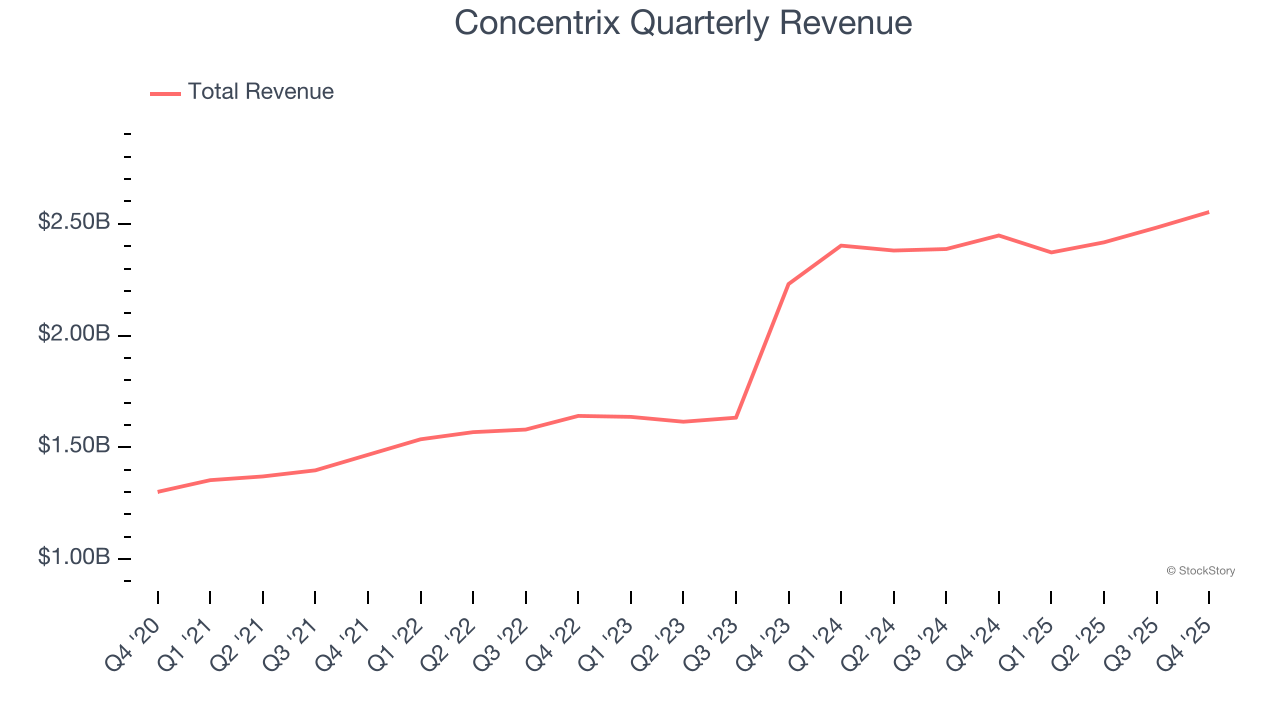

Customer experience solutions provider Concentrix (NASDAQ: CNXC) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 4.3% year on year to $2.55 billion. The company expects next quarter’s revenue to be around $2.49 billion, close to analysts’ estimates. Its non-GAAP profit of $2.95 per share was 1.4% above analysts’ consensus estimates.

Is now the time to buy Concentrix? Find out by accessing our full research report, it’s free.

Concentrix (CNXC) Q4 CY2025 Highlights:

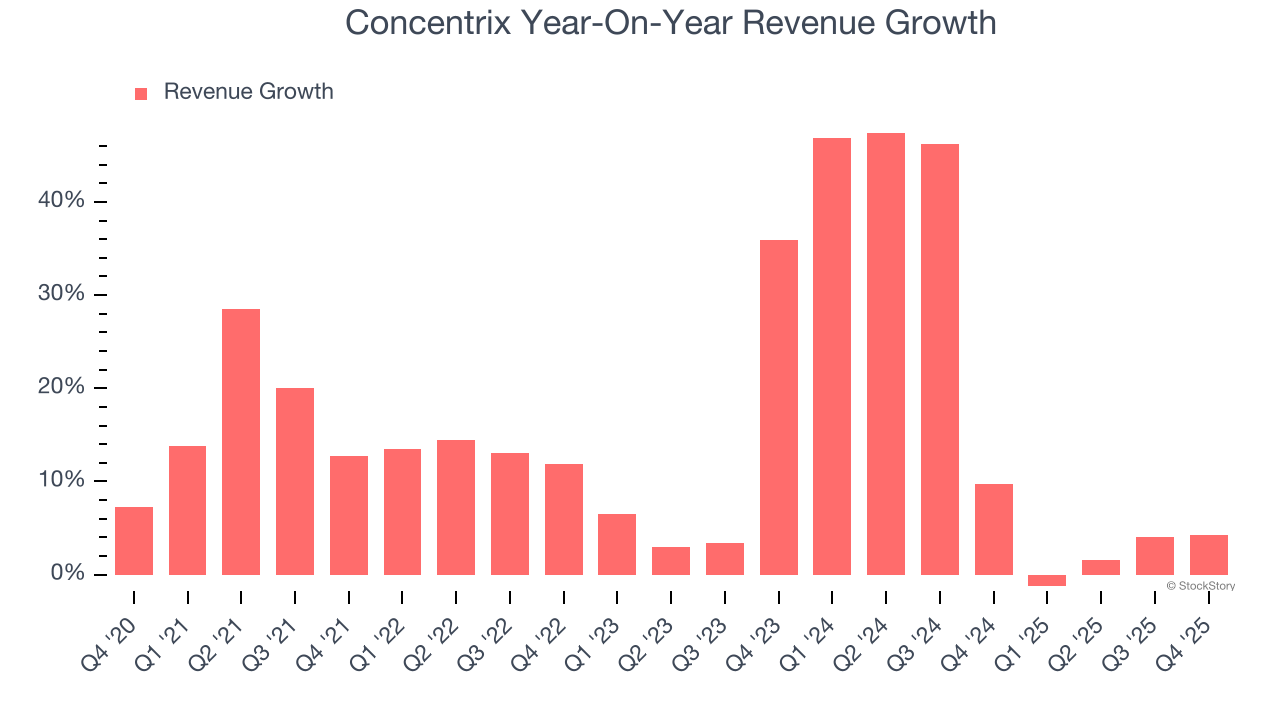

- Revenue: $2.55 billion vs analyst estimates of $2.53 billion (4.3% year-on-year growth, 0.7% beat)

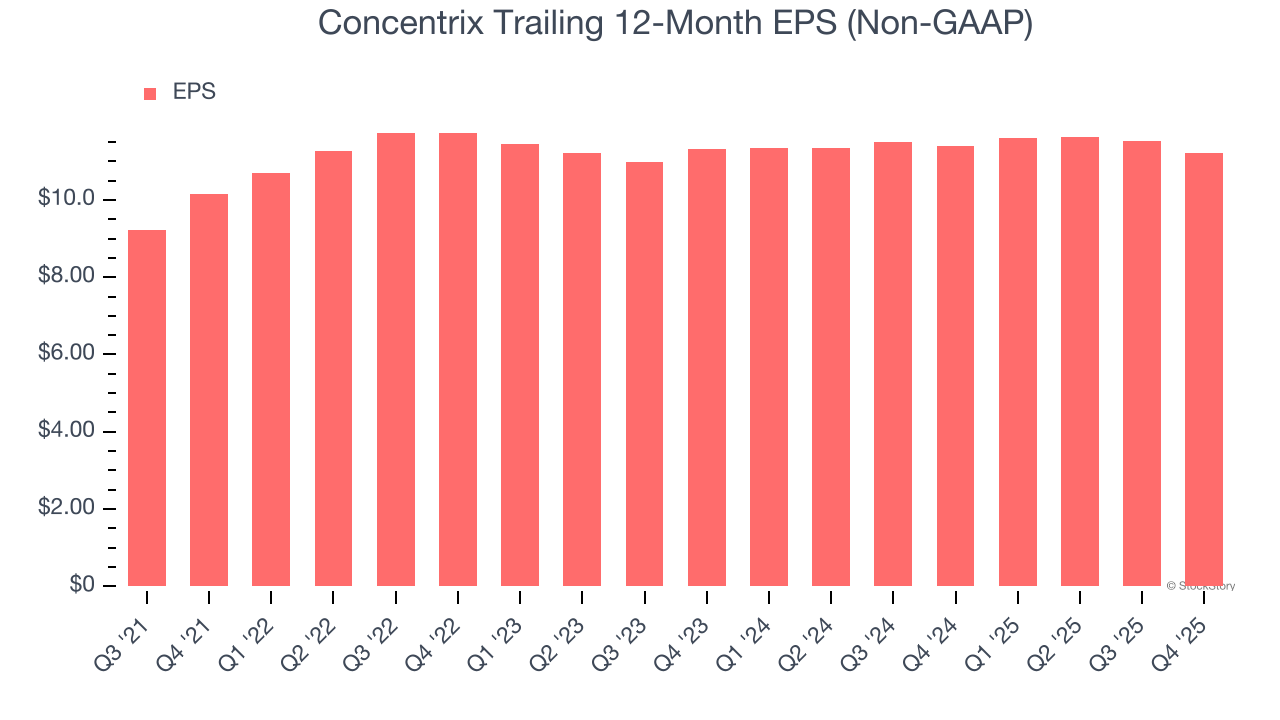

- Adjusted EPS: $2.95 vs analyst estimates of $2.91 (1.4% beat)

- Adjusted EBITDA: $378.6 million vs analyst estimates of $384.9 million (14.8% margin, 1.6% miss)

- Revenue Guidance for Q1 CY2026 is $2.49 billion at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2026 is $11.78 at the midpoint, missing analyst estimates by 3.9%

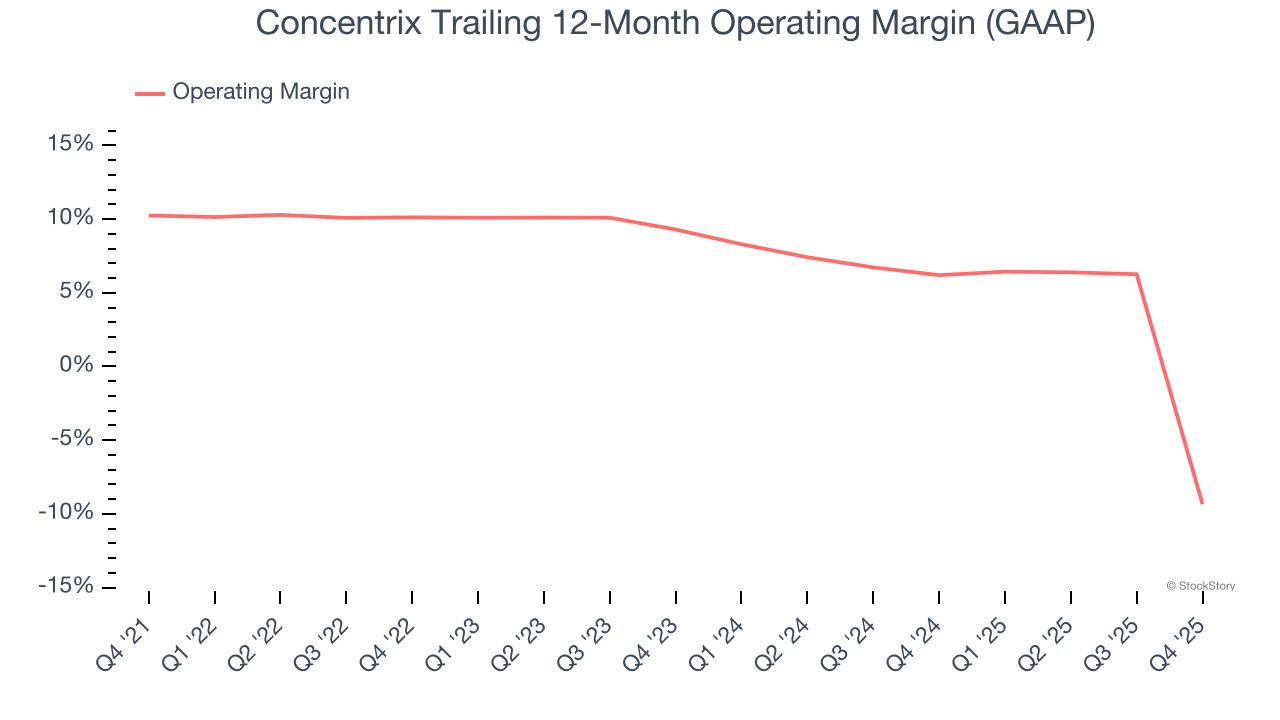

- Operating Margin: -54.1%, down from 5.9% in the same quarter last year due to a non-cash goodwill impairment charge of $1,523.3 million

- Free Cash Flow Margin: 11%, up from 9.2% in the same quarter last year

- Market Capitalization: $2.52 billion

“Our positive fourth quarter and fiscal year results reflect our steadfast commitment to advance our business to meet evolving client demand while delivering value to shareholders,” said Chris Caldwell, Concentrix President and CEO.

Company Overview

With a team of approximately 450,000 employees across 75 countries, Concentrix (NASDAQ: CNXC) designs and delivers customer experience solutions that help global brands manage their customer interactions across digital channels and contact centers.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $9.83 billion in revenue over the past 12 months, Concentrix is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

As you can see below, Concentrix’s sales grew at an incredible 15.8% compounded annual growth rate over the last five years. This is an encouraging starting point for our analysis because it shows Concentrix’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Concentrix’s annualized revenue growth of 17.5% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Concentrix reported modest year-on-year revenue growth of 4.3% but beat Wall Street’s estimates by 0.7%. Company management is currently guiding for a 4.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Concentrix was profitable over the last five years but held back by its large cost base. Its average operating margin of 4% was weak for a business services business.

Analyzing the trend in its profitability, Concentrix’s operating margin decreased by 19.6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Concentrix’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Concentrix generated an operating margin profit margin of negative 54.1%, down 60.1 percentage points year on year. This quarter was impacted by a non-cash goodwill impairment charge of $1,523.3 million.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Concentrix’s full-year EPS grew at a weak 2.6% compounded annual growth rate over the last four years, worse than the broader business services sector.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Concentrix’s flat EPS over the last two years was worse than its 17.5% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into Concentrix’s earnings to better understand the drivers of its performance. Concentrix’s operating margin has declined over the last two years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Concentrix reported adjusted EPS of $2.95, down from $3.26 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 1.4%. Over the next 12 months, Wall Street expects Concentrix’s full-year EPS of $11.22 to grow 8%.

Key Takeaways from Concentrix’s Q4 Results

It was good to see Concentrix narrowly top analysts’ revenue expectations this quarter. On the other hand, its full-year EPS guidance missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 4.5% to $38.67 immediately following the results.

Concentrix may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).