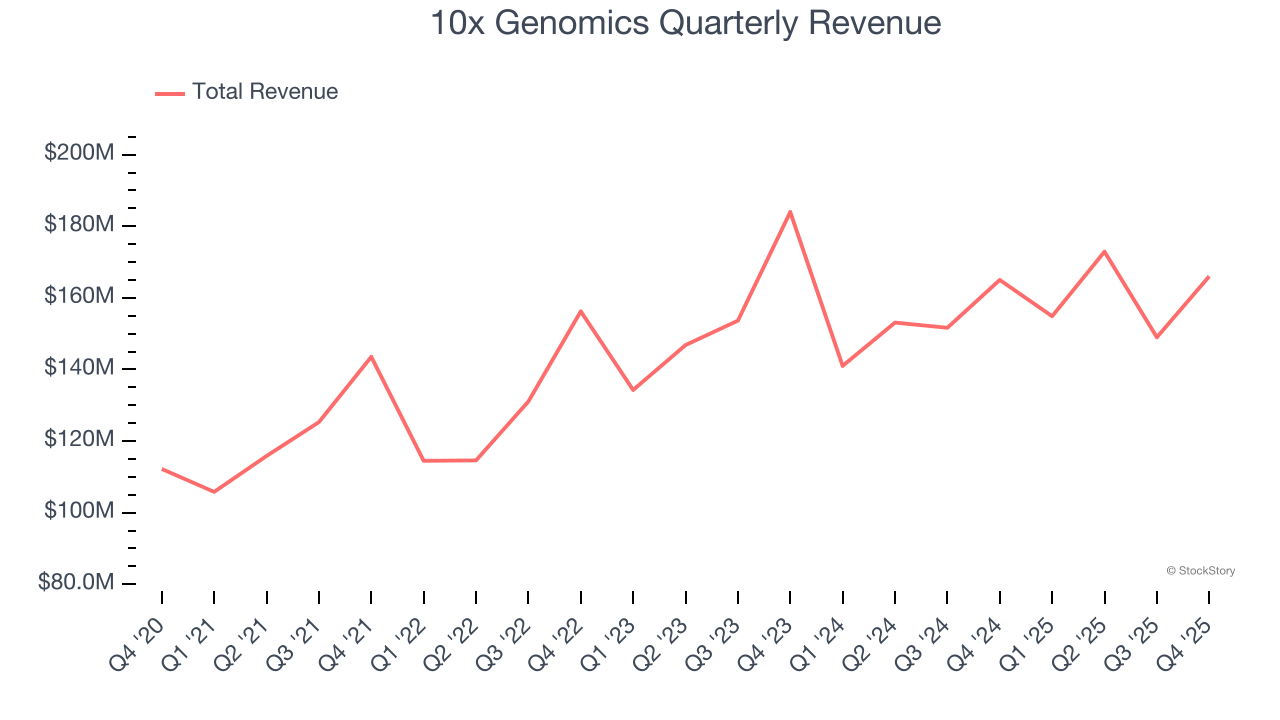

Biotech company 10x Genomics (NASDAQ: TXG) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, but sales were flat year on year at $166 million. The company expects the full year’s revenue to be around $612.5 million, close to analysts’ estimates. Its GAAP loss of $0.13 per share was 37.5% above analysts’ consensus estimates.

Is now the time to buy 10x Genomics? Find out by accessing our full research report, it’s free.

10x Genomics (TXG) Q4 CY2025 Highlights:

- Revenue: $166 million vs analyst estimates of $159.2 million (flat year on year, 4.3% beat)

- EPS (GAAP): -$0.13 vs analyst estimates of -$0.21 (37.5% beat)

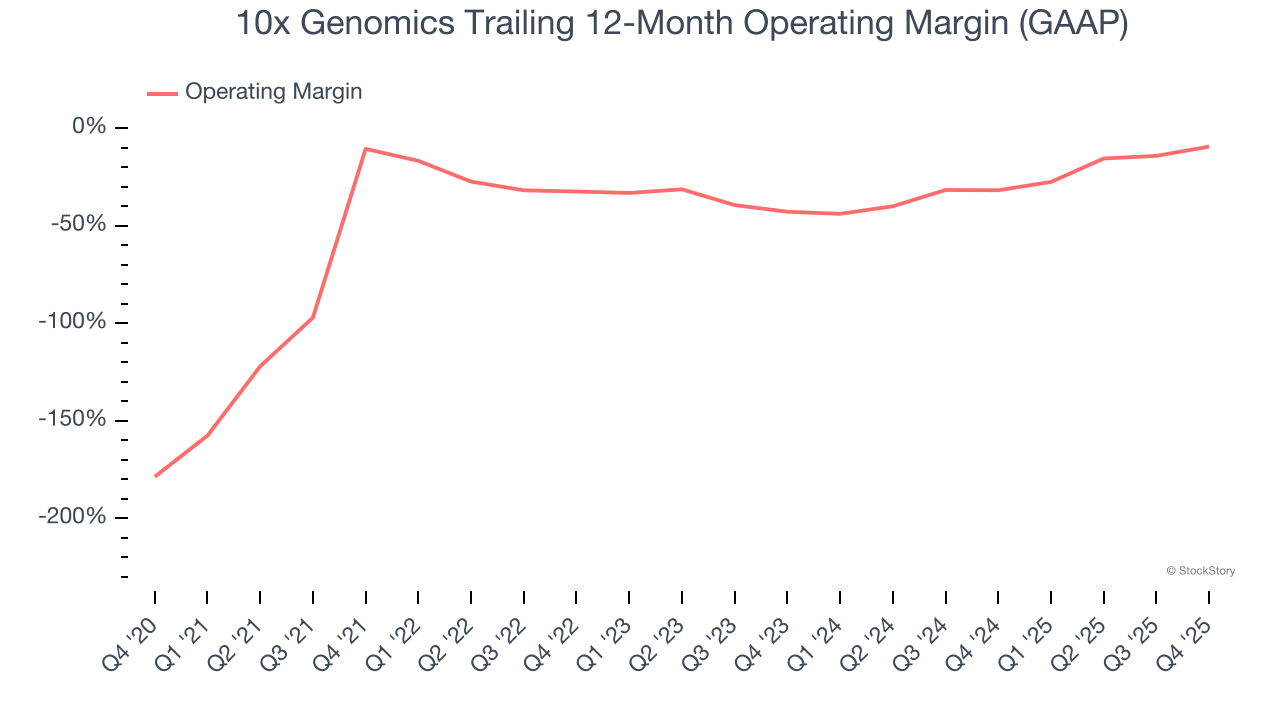

- Operating Margin: -11.8%, up from -30.2% in the same quarter last year

- Market Capitalization: $2.42 billion

"In 2025, our team executed with discipline through a challenging environment while continuing to strengthen the fundamentals of the business," said Serge Saxonov, Co-founder and CEO of 10x Genomics.

Company Overview

Founded in 2012 by scientists seeking to overcome limitations in traditional biological research methods, 10x Genomics (NASDAQ: TXG) develops instruments, consumables, and software that enable researchers to analyze biological systems at single-cell resolution and spatial context.

Revenue Growth

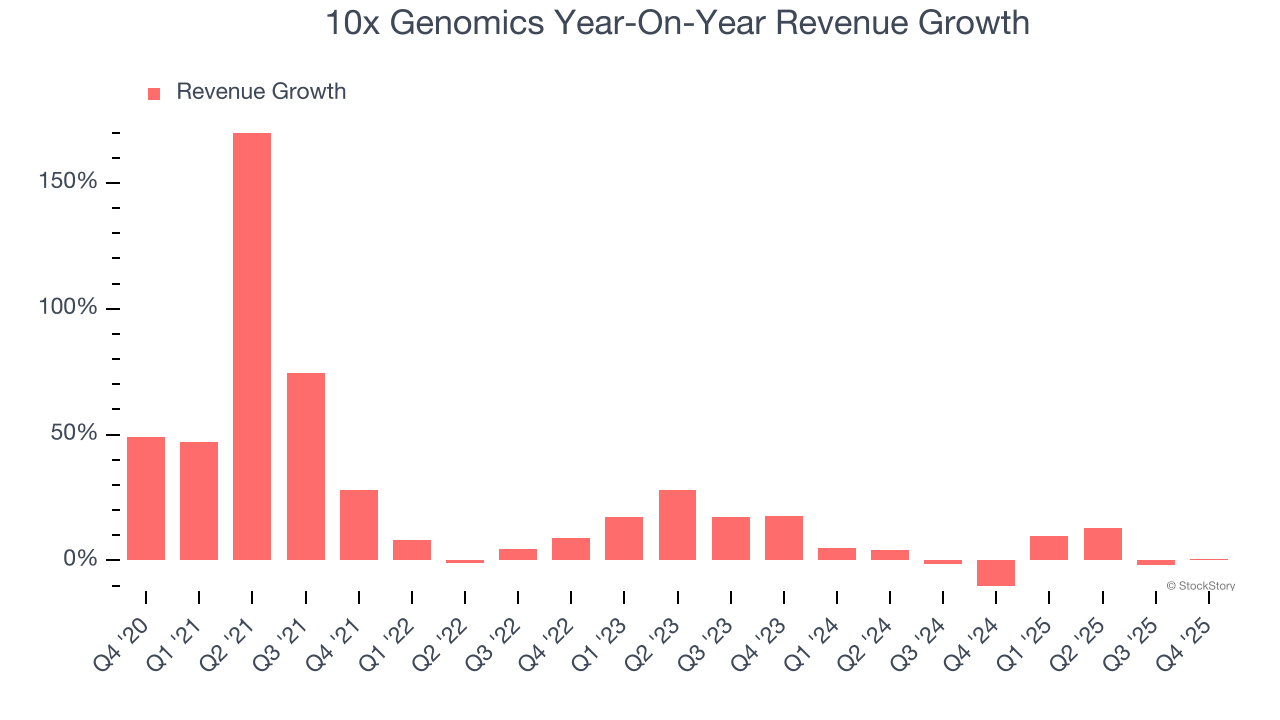

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, 10x Genomics grew its sales at an impressive 16.6% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. 10x Genomics’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 1.9% over the last two years was well below its five-year trend.

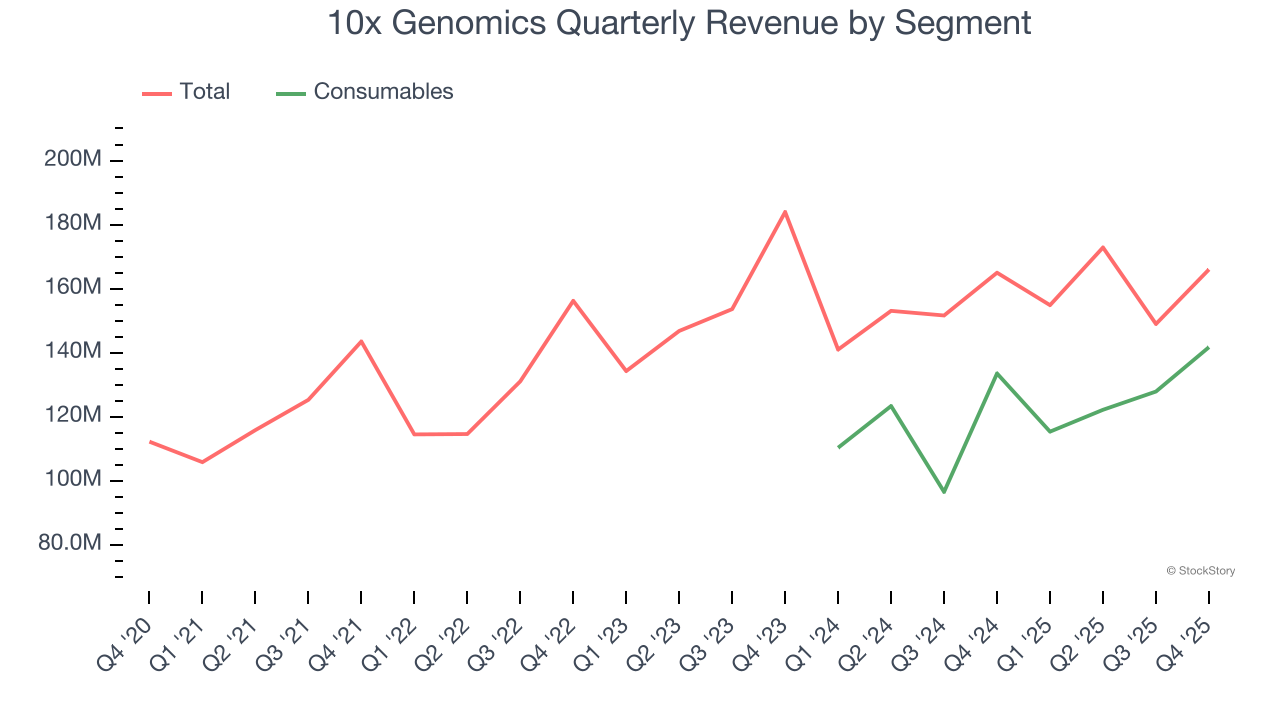

10x Genomics also breaks out the revenue for its most important segment, Consumables. Over the last two years, 10x Genomics’s Consumables revenue (recurring orders) averaged 10.6% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, 10x Genomics’s $166 million of revenue was flat year on year but beat Wall Street’s estimates by 4.3%.

Looking ahead, sell-side analysts expect revenue to decline by 5% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

10x Genomics’s high expenses have contributed to an average operating margin of negative 25.7% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, 10x Genomics’s operating margin rose by 1.2 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its recent improvements as the company’s margin has increased by 33.4 percentage points on a two-year basis.

This quarter, 10x Genomics generated a negative 11.8% operating margin.

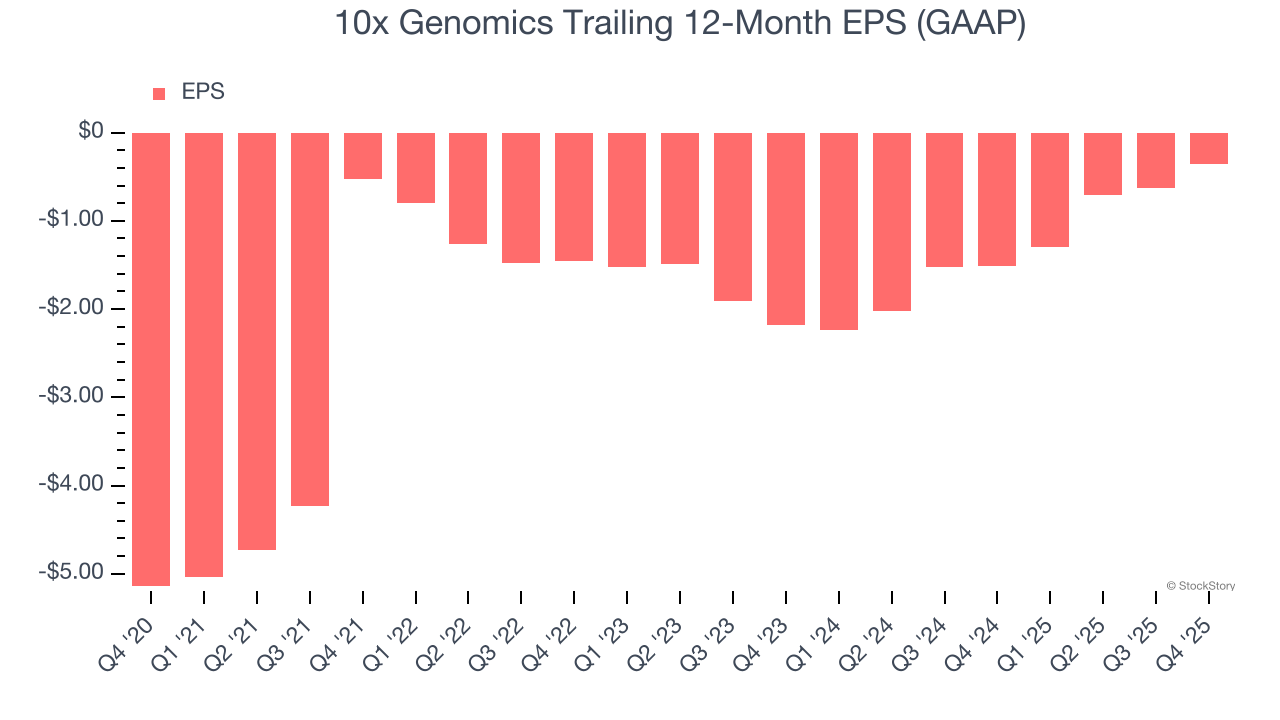

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although 10x Genomics’s full-year earnings are still negative, it reduced its losses and improved its EPS by 41.5% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q4, 10x Genomics reported EPS of negative $0.13, up from negative $0.40 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects 10x Genomics to perform poorly. Analysts forecast its full-year EPS of negative $0.35 will tumble to negative $0.94.

Key Takeaways from 10x Genomics’s Q4 Results

It was good to see 10x Genomics beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $17.44 immediately after reporting.

So do we think 10x Genomics is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).