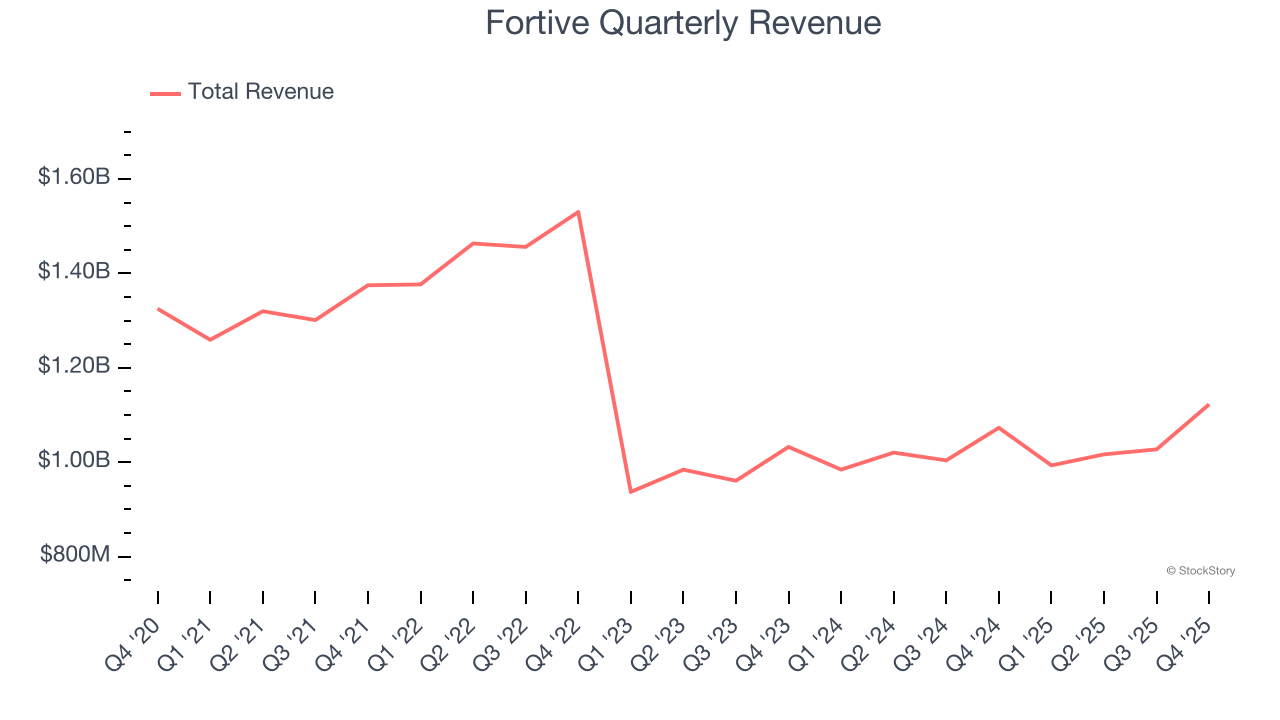

Industrial technology company Fortive (NYSE: FTV) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 4.6% year on year to $1.12 billion. Its non-GAAP profit of $0.90 per share was 7.4% above analysts’ consensus estimates.

Is now the time to buy Fortive? Find out by accessing our full research report, it’s free.

Fortive (FTV) Q4 CY2025 Highlights:

- Revenue: $1.12 billion vs analyst estimates of $1.09 billion (4.6% year-on-year growth, 2.7% beat)

- Adjusted EPS: $0.90 vs analyst estimates of $0.84 (7.4% beat)

- Adjusted EBITDA: $357.9 million vs analyst estimates of $354.8 million (31.9% margin, 0.9% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $2.95 at the midpoint, beating analyst estimates by 3.8%

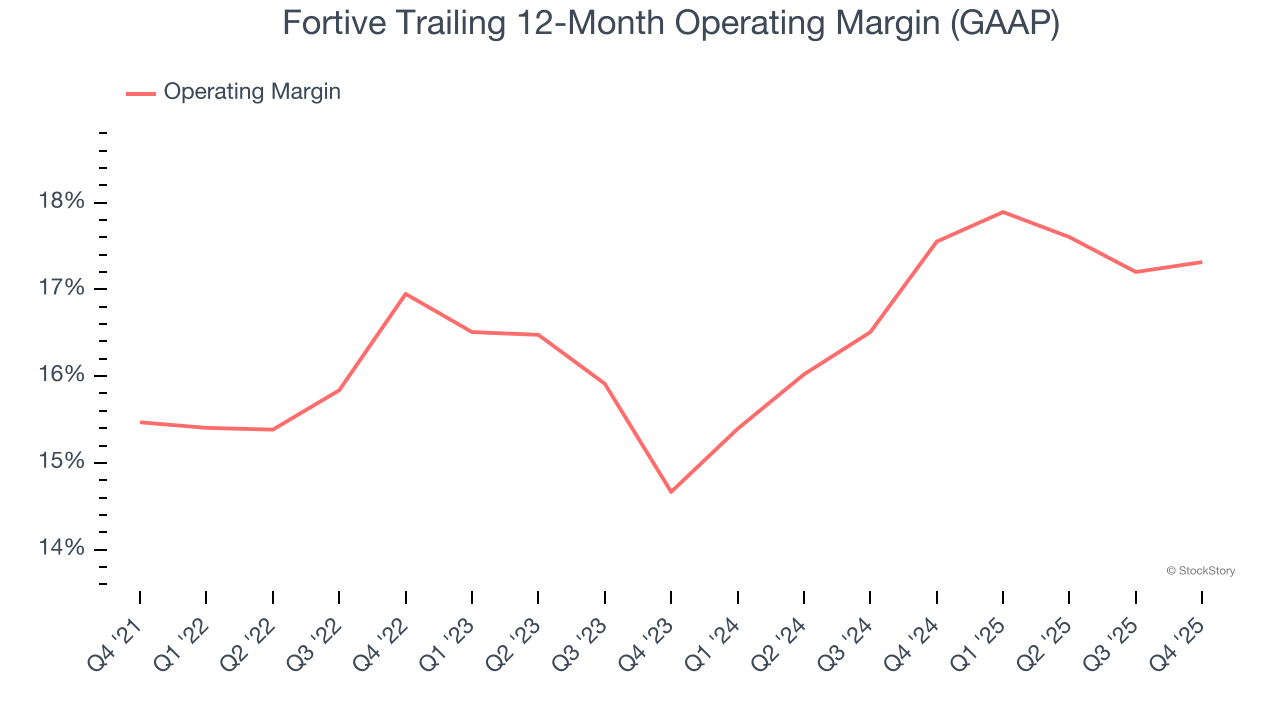

- Operating Margin: 20.1%, in line with the same quarter last year

- Free Cash Flow Margin: 28%, similar to the same quarter last year

- Market Capitalization: $17.26 billion

“Q4 represented another quarter of solid execution by our new Fortive team. With the first two quarters of performance now behind us, and our 2026 strategic and financial plans firmly in place, our strong conviction in the road ahead continues to build. In Q4, our team delivered results ahead of our expectations with ~3% core revenue growth, ~8% Adjusted EBITDA growth, and ~13% Adjusted EPS growth. This strong performance enabled us to exceed the high end of our full year Adjusted EPS guidance range. We also continued to execute our disciplined, returns-focused capital allocation strategy, completing an additional $265 million of share repurchases in the quarter and bringing total second-half buybacks to ~$1.3 billion,” said Olumide Soroye, President and CEO.

Company Overview

Taking its name from the Latin root of "strong", Fortive (NYSE: FTV) manufactures products and develops industrial software for numerous industries.

Revenue Growth

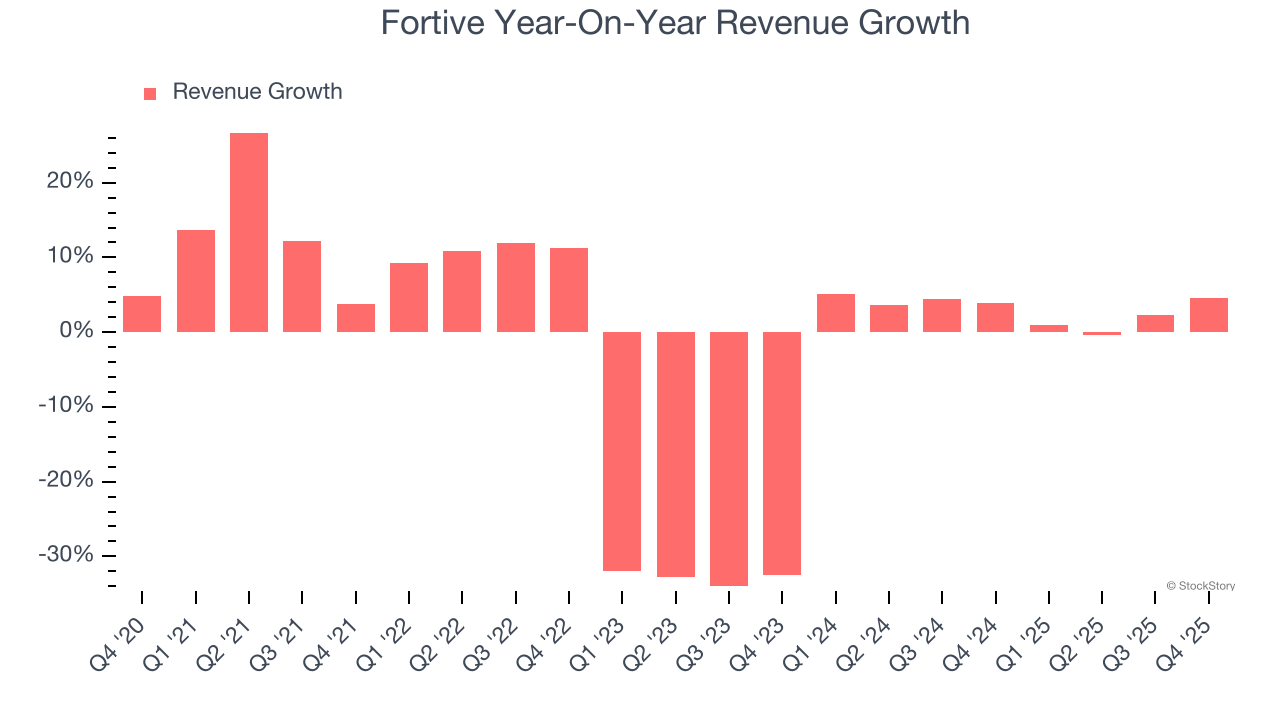

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Fortive’s demand was weak over the last five years as its sales fell at a 2.1% annual rate. This wasn’t a great result and is a sign of poor business quality.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Fortive’s annualized revenue growth of 3.1% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, Fortive reported modest year-on-year revenue growth of 4.6% but beat Wall Street’s estimates by 2.7%.

Looking ahead, sell-side analysts expect revenue to decline by 4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Operating Margin

Fortive has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.4%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Fortive’s operating margin rose by 1.8 percentage points over the last five years, showing its efficiency has improved.

In Q4, Fortive generated an operating margin profit margin of 20.1%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

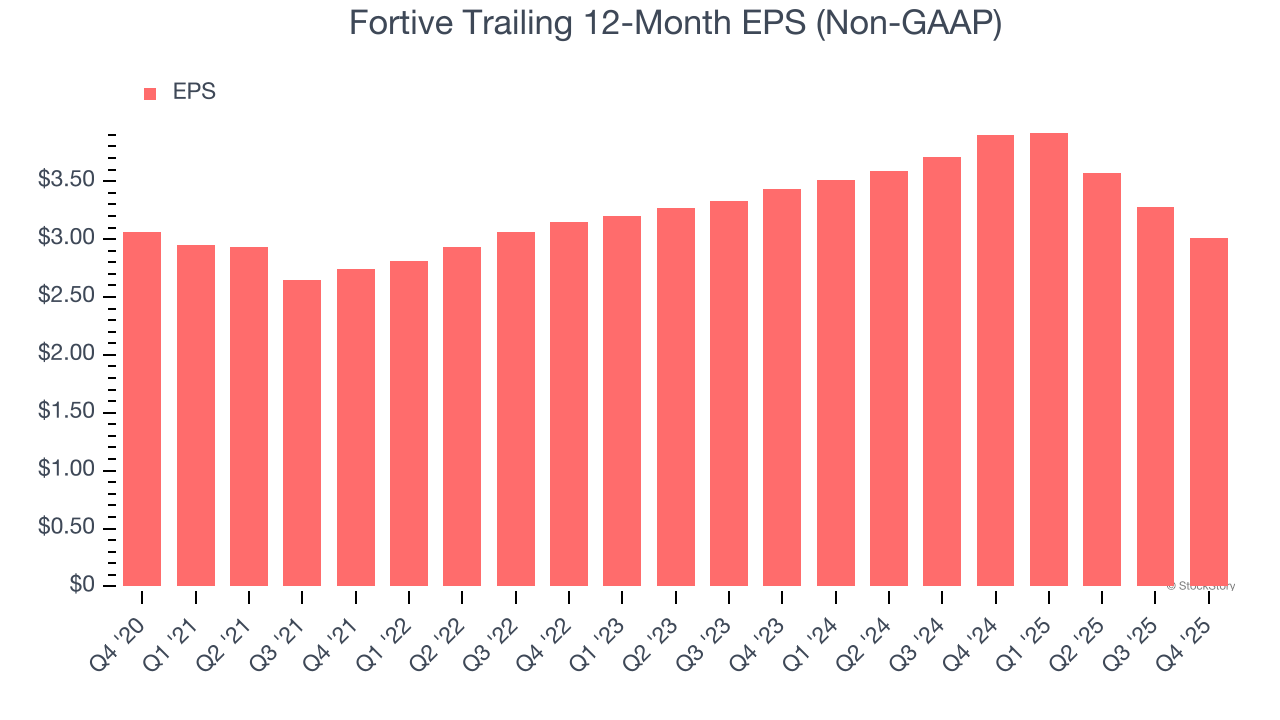

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Fortive’s flat EPS over the last five years was weak but better than its 2.1% annualized revenue declines. This tells us management adapted its cost structure.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Fortive, its two-year annual EPS declines of 6.3% show its recent history was to blame for its underperformance over the last five years. These results were bad no matter how you slice the data.

In Q4, Fortive reported adjusted EPS of $0.90, down from $1.17 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 7.4%. Over the next 12 months, Wall Street expects Fortive’s full-year EPS of $3.01 to shrink by 5.3%.

Key Takeaways from Fortive’s Q4 Results

We were impressed by Fortive’s optimistic full-year EPS guidance, which blew past analysts’ expectations. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 1.7% to $55.30 immediately after reporting.

Fortive may have had a good quarter, but does that mean you should invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).