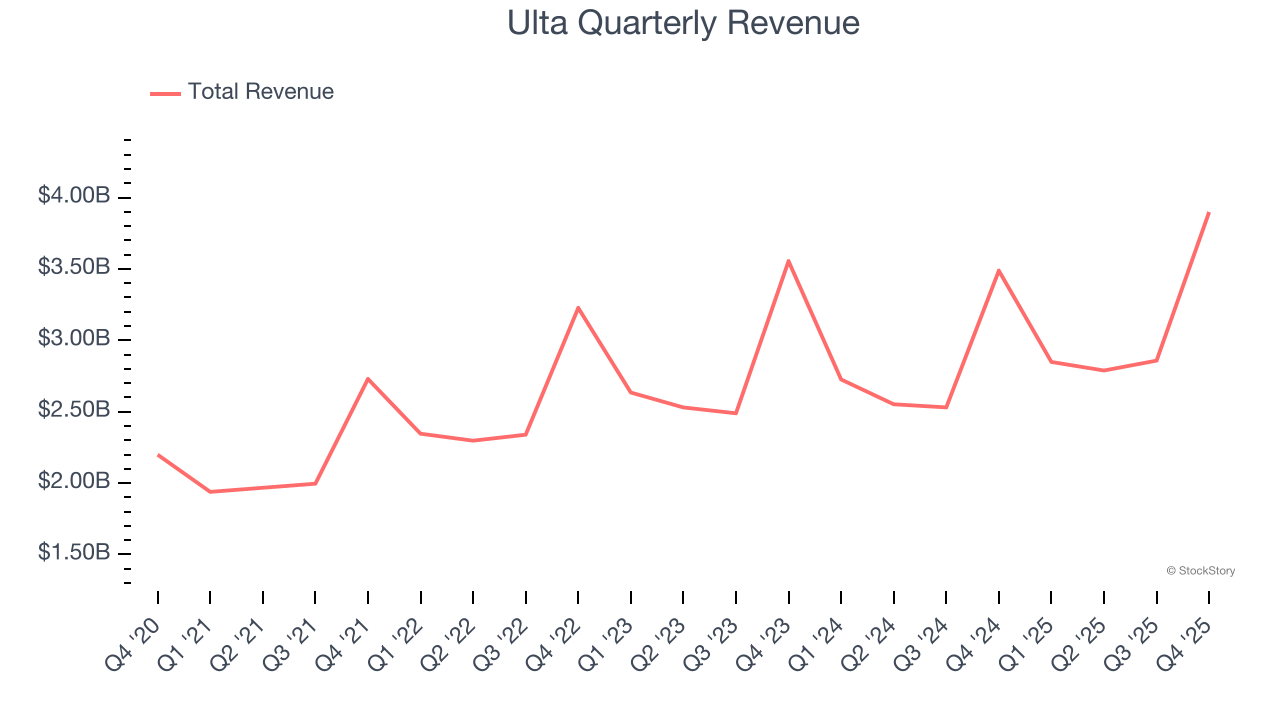

Beauty, cosmetics, and personal care retailer Ulta Beauty (NASDAQ: ULTA) announced better-than-expected revenue in Q4 CY2025, with sales up 11.8% year on year to $3.90 billion. Its GAAP profit of $8.01 per share was in line with analysts’ consensus estimates.

Is now the time to buy Ulta? Find out by accessing our full research report, it’s free.

Ulta (ULTA) Q4 CY2025 Highlights:

- Revenue: $3.90 billion vs analyst estimates of $3.83 billion (11.8% year-on-year growth, 1.9% beat)

- EPS (GAAP): $8.01 vs analyst expectations of $8.03 (in line)

- Adjusted EBITDA: $596.2 million vs analyst estimates of $561.9 million (15.3% margin, 6.1% beat)

- EPS (GAAP) guidance for the upcoming financial year 2026 is $28.30 at the midpoint, missing analyst estimates by 1%

- Operating Margin: 12.2%, down from 14.8% in the same quarter last year

- Free Cash Flow Margin: 25.4%, down from 27.6% in the same quarter last year

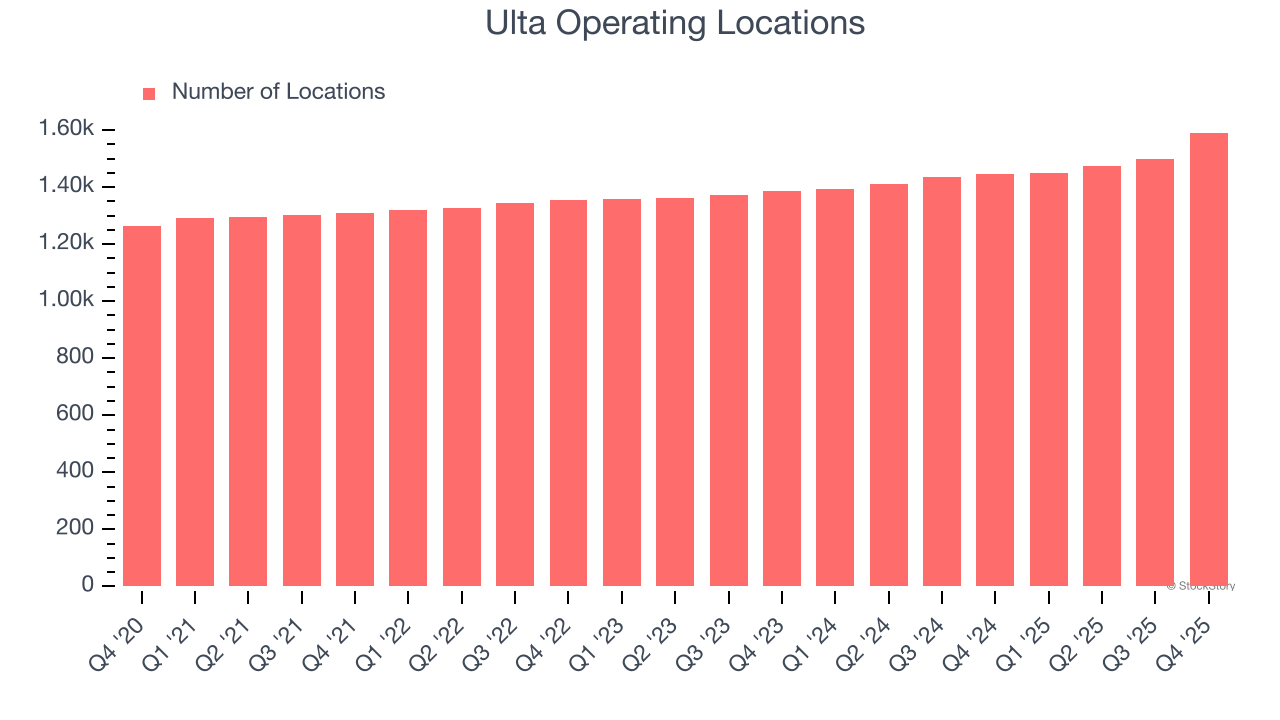

- Locations: 1,591 at quarter end, up from 1,445 in the same quarter last year

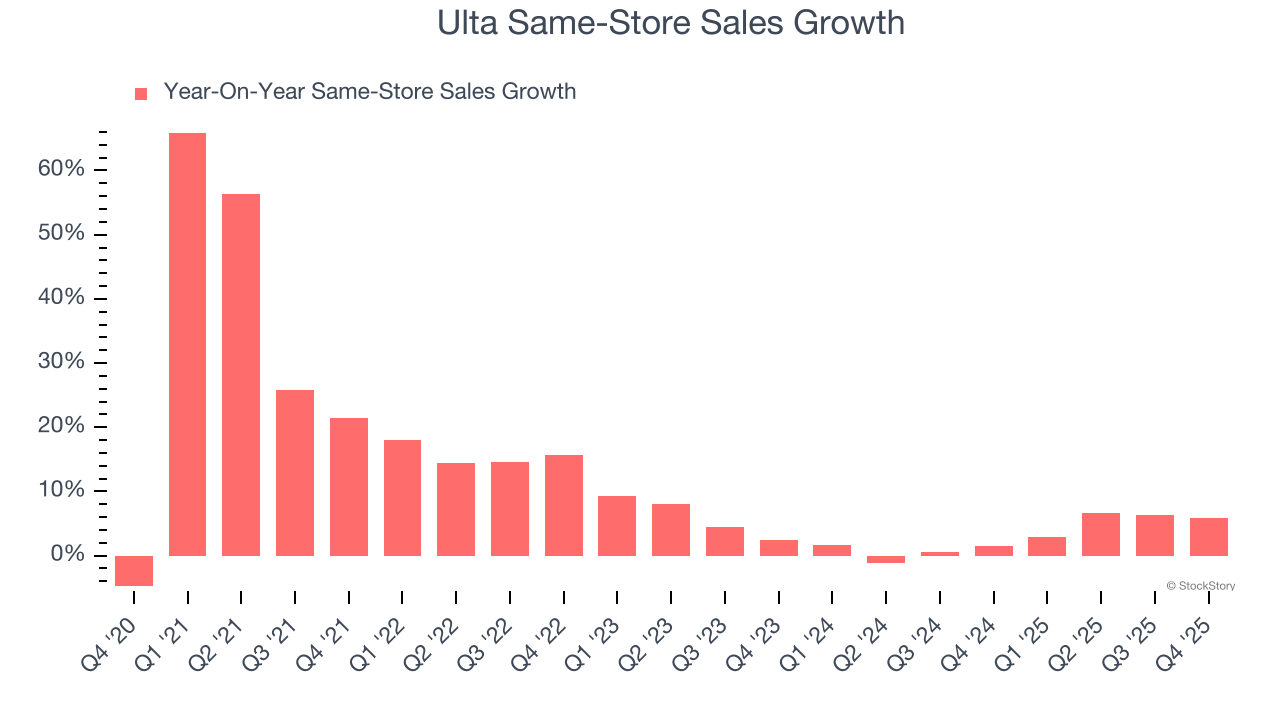

- Same-Store Sales rose 5.8% year on year (1.5% in the same quarter last year)

- Market Capitalization: $28.95 billion

Company Overview

Offering high-end prestige brands as well as lower-priced, mass-market ones, Ulta Beauty (NASDAQ: ULTA) is an American retailer that sells makeup, skincare, haircare, and fragrance products.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $12.39 billion in revenue over the past 12 months, Ulta is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Ulta’s 6.7% annualized revenue growth over the last three years was tepid, but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, Ulta reported year-on-year revenue growth of 11.8%, and its $3.90 billion of revenue exceeded Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to grow 6.1% over the next 12 months, similar to its three-year rate. This projection is particularly healthy for a company of its scale and implies the market is baking in success for its products.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Store Performance

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Ulta operated 1,591 locations in the latest quarter. It has opened new stores at a rapid clip over the last two years, averaging 4.8% annual growth, much faster than the broader consumer retail sector. This gives it a chance to become a large, scaled business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Ulta’s demand has been healthy for a retailer over the last two years. On average, the company has grown its same-store sales by a robust 3% per year. This performance suggests its rollout of new stores could be beneficial for shareholders. When a retailer has demand, more locations should help it reach more customers and boost revenue growth.

In the latest quarter, Ulta’s same-store sales rose 5.8% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

Key Takeaways from Ulta’s Q4 Results

We enjoyed seeing Ulta beat analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance slightly missed. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 9.5% to $570.82 immediately after reporting.

Is Ulta an attractive investment opportunity right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).