VF Corp has had an impressive run over the past six months as its shares have beaten the S&P 500 by 5.4%. The stock now trades at $15.85, marking a 7.7% gain. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy VF Corp, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think VF Corp Will Underperform?

We’re glad investors have benefited from the price increase, but we're swiping left on VF Corp for now. Here are three reasons you should be careful with VFC and a stock we'd rather own.

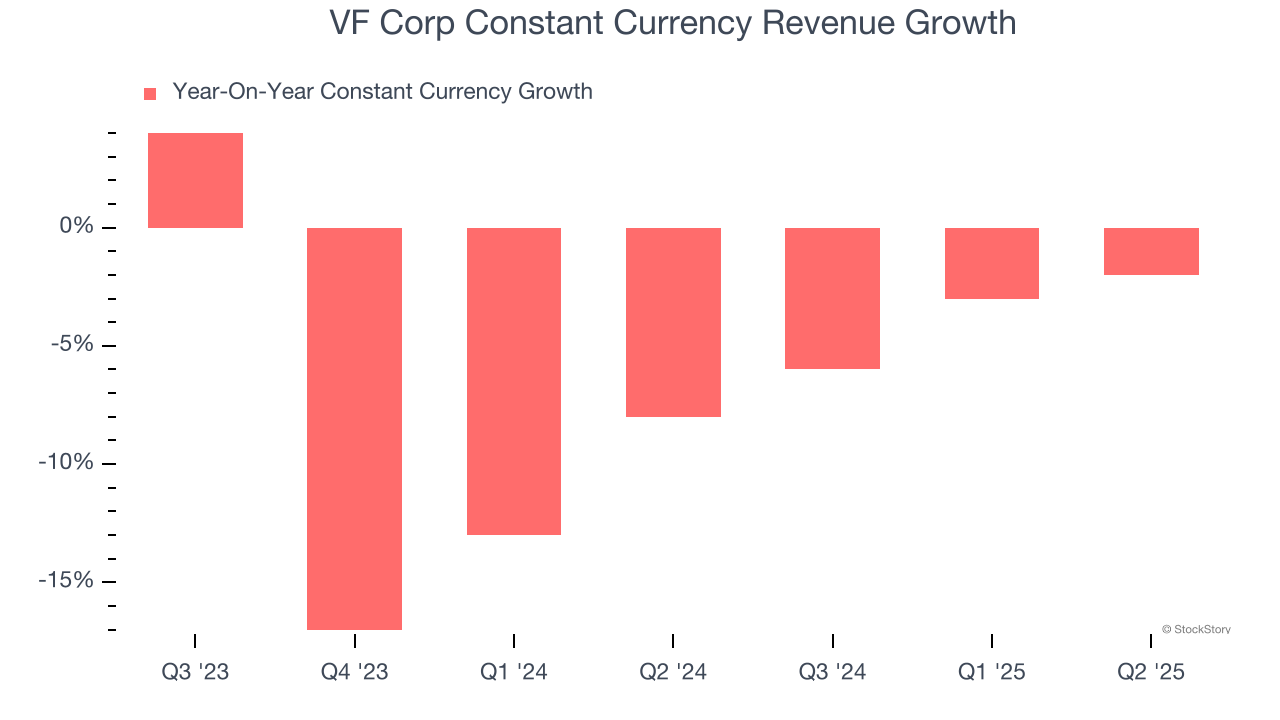

1. Declining Constant Currency Revenue, Demand Takes a Hit

In addition to reported revenue, constant currency revenue is a useful data point for analyzing Consumer Discretionary - Apparel and Accessories companies. This metric excludes currency movements, which are outside of VF Corp’s control and are not indicative of underlying demand.

Over the last two years, VF Corp’s constant currency revenue averaged 6.4% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests VF Corp might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

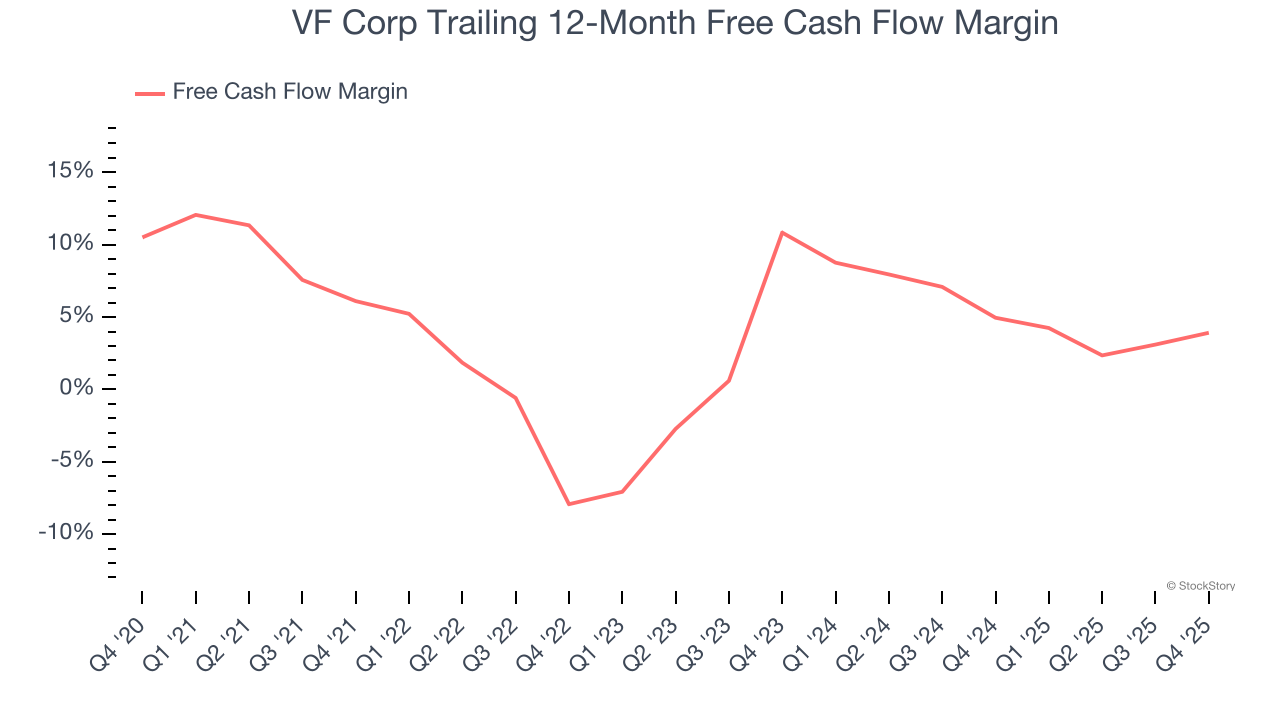

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

VF Corp has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 4.4%, below what we’d expect for a consumer discretionary business.

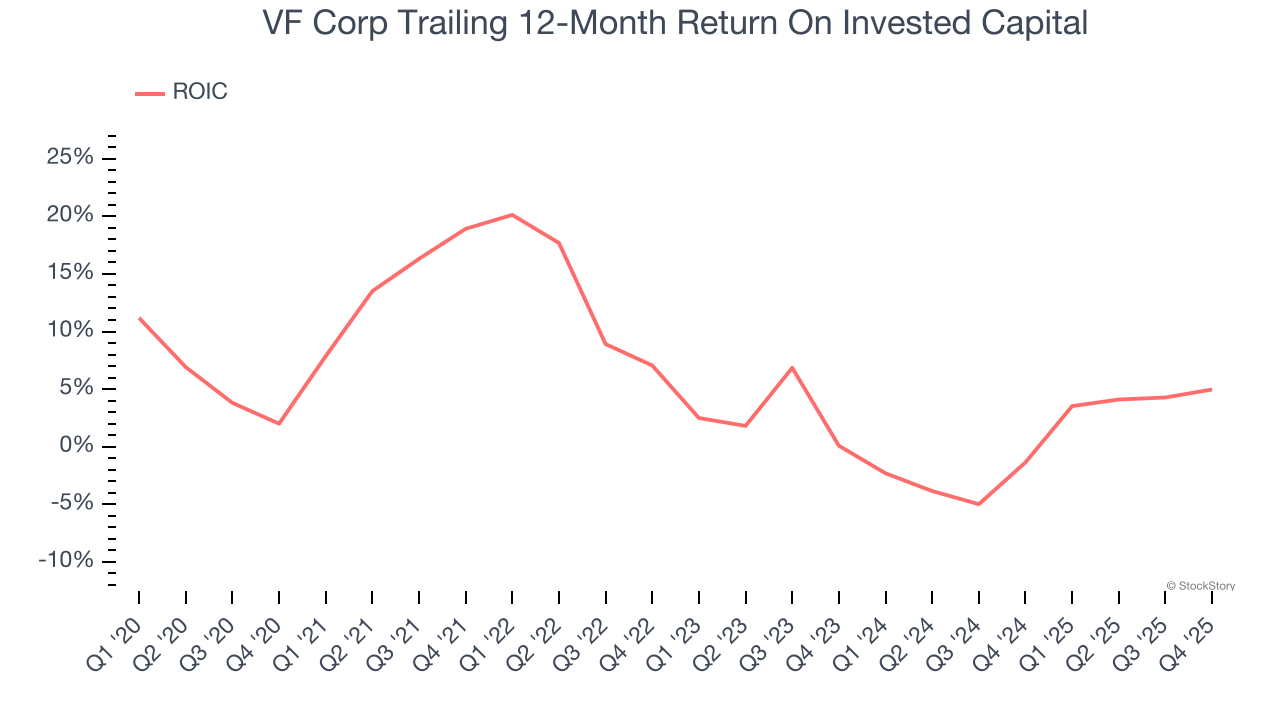

3. New Investments Fail to Bear Fruit as ROIC Declines

We like to invest in businesses with high returns, but the trend in a company’s ROIC can also be an early indicator of future business quality.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, VF Corp’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of VF Corp, we’ll be cheering from the sidelines. With its shares topping the market in recent months, the stock trades at 16.7× forward P/E (or $15.85 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. We’d suggest looking at a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of VF Corp

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.